Exam 2: Accounting for Business Combinations

Exam 1: Introduction to Business Combinations and the Conceptual Framework35 Questions

Exam 2: Accounting for Business Combinations42 Questions

Exam 3: Consolidated Financial Statements-Date of Acquisition37 Questions

Exam 4: Consolidated Financial Statements After Acquisition42 Questions

Exam 5: Allocation and Depreciation of Differences Between Implied and Book Values36 Questions

Exam 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory35 Questions

Exam 7: Elimination of Unrealized Gains or Losses on Intercompany Sales of Property and Equipment33 Questions

Exam 8: Changes in Ownership Interest32 Questions

Exam 9: Intercompany Bond Holdings and Miscellaneous Topicsconsolidated Financial Statements33 Questions

Exam 10: Insolvencyliquidation and Reorganization34 Questions

Exam 11: International Financial Reporting Standards28 Questions

Exam 12: Accounting for Foreign Currency Transactions and Hedging Foreign Exchange Risk35 Questions

Exam 13: Translation of Financial Statements of Foreign Affiliates29 Questions

Exam 14: Reporting for Segments and for Interim Financial Periods44 Questions

Exam 15: Partnerships: Formation, Operation, and Ownership Changes39 Questions

Exam 16: Partnerships: Formation, Operation, and Ownership Changes35 Questions

Exam 17: Introduction to Fund Accounting29 Questions

Exam 18: Introduction to Accounting for State and Local Governmental Units34 Questions

Exam 19: Accounting for Nongovernment Nonbusiness Organizations: Colleges and Universities, Hospitals and Other Health Care Organizations39 Questions

Select questions type

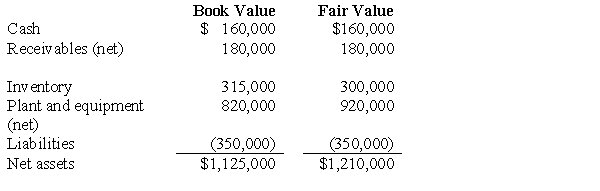

On February 5, Pryor Corporation paid $1,600,000 for all the issued and outstanding common stock of Shaw, Inc., in a transaction properly accounted for as an acquisition. The book values and fair values of Shaw's assets and liabilities on February 5 were as follows:  What is the amount of goodwill resulting from the business combination?

What is the amount of goodwill resulting from the business combination?

Free

(Multiple Choice)

4.9/5  (43)

(43)

Correct Answer: Verified

Verified

D

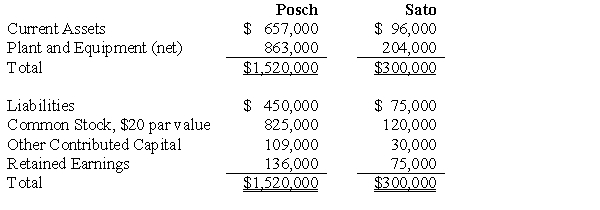

Posch Company issued 12,000 shares of its $20 par value common stock for the net assets of Sato Company in a business combination under which Sato Company will be merged into Posch Company. On the date of the combination, Posch Company common stock had a fair value of $30 per share. Balance sheets for Posch Company and Sato Company immediately prior to the combination were as follows:  If the business combination is treated as an acquisition and the fair value of Sato Company's current assets is $135,000, its plant and equipment is $363,000, and its liabilities are $84,000, Posch Company's financial statements immediately after the combination will include:

If the business combination is treated as an acquisition and the fair value of Sato Company's current assets is $135,000, its plant and equipment is $363,000, and its liabilities are $84,000, Posch Company's financial statements immediately after the combination will include:

Free

(Multiple Choice)

4.7/5 (38)

Correct Answer:Verified

B

The stockholders' equities of Penn Corporation and Simon Corporation were as follows on January 1, 2016:

On January 2, 2016 Penn Corp. issued 100,000 of its shares with a market value of $14 per share in exchange for all of Simon's shares, and Simon Corp. was dissolved. Penn Corp. paid $10,000 to register and issue the new common shares.

Required:

Prepare the stockholders' equity section of Penn Corp. balance sheet after the business combination on January 2, 2016.

On January 2, 2016 Penn Corp. issued 100,000 of its shares with a market value of $14 per share in exchange for all of Simon's shares, and Simon Corp. was dissolved. Penn Corp. paid $10,000 to register and issue the new common shares.

Required:

Prepare the stockholders' equity section of Penn Corp. balance sheet after the business combination on January 2, 2016.

Free

(Essay)

4.8/5 (34)

Correct Answer:Verified

The managers of Savage Company own 10,000 of its 100,000 outstanding common shares. Swann Company is formed by the managers of Savage Company to take over Savage Company in a leveraged buyout. The managers contribute their shares in Savage Company and Swann Company then borrows $675,000 to purchase the remaining 90,000 shares of Savage Company for $600,000; the remaining $75,000 is used for working capital. Savage Company is then merged into Swann Company effective January 1, 2016. Data relevant to Savage Company immediately prior to the leveraged buyout follow:  Required:

A. Prepare journal entries on Swann Company's books to reflect the effects of the leveraged buyout.

B. Determine the balance of each of the following immediately after the merger:

1. Current Assets

2. Plant Assets

3. Note Payable

4. Common Stock

Required:

A. Prepare journal entries on Swann Company's books to reflect the effects of the leveraged buyout.

B. Determine the balance of each of the following immediately after the merger:

1. Current Assets

2. Plant Assets

3. Note Payable

4. Common Stock

(Essay)

4.9/5 (36)

P Co. issued 5,000 shares of its common stock, valued at $200,000, to the former shareholders of S Company two years after S Company was acquired in an all-stock transaction. The additional shares were issued because P Company agreed to issue additional shares of common stock if the average post combination earnings over the next two years exceeded $500,000. P Company will treat the issuance of the additional shares as a (decrease in):

(Multiple Choice)

4.7/5 (33)

Briefly describe the different treatment under SFAS 141 vs. SFAS 141R for the following issues:

-Business definition

-Acquisition costs

-In-process R&D

-Contingent consideration

(Essay)

4.8/5 (30)

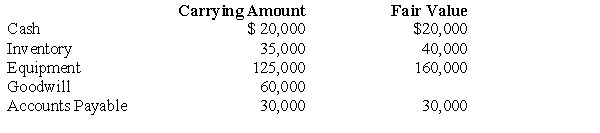

Following its acquisition of the net assets of Burnt Company, Primrose Company assigned goodwill of $60,000 to one of the reporting divisions. Information for this division follows:  Based on the preceding information, what amount of goodwill will be reported for this division if its fair value is determined to be $200,000?

Based on the preceding information, what amount of goodwill will be reported for this division if its fair value is determined to be $200,000?

(Multiple Choice)

4.8/5 (44)

Porpoise Corporation acquired Sims Company through an exchange of common shares. All of Sims' assets and liabilities were immediately transferred to Porpoise. Porpoise Company's common stock was trading at $20 per share at the time of exchange. The following selected information is also available:  What number of shares was issued at the time of the exchange?

What number of shares was issued at the time of the exchange?

(Multiple Choice)

4.8/5 (36)

SFAS 141R requires that the acquirer disclose each of the following for each material business combination EXCEPT the:

(Multiple Choice)

4.8/5 (31)

Parental Company and Sub Company were combined in an acquisition transaction. Parental was able to acquire Sub at a bargain price. The sum of the fair values of identifiable assets acquired less the fair value of liabilities assumed exceeded the cost to Parental. After eliminating previously recorded goodwill, there was still some "negative goodwill." Proper accounting treatment by Parental is to report the amount as:

(Multiple Choice)

4.8/5 (41)

SFAS 141R requires that all business combinations be accounted for using:

(Multiple Choice)

4.9/5 (39)

Under the acquisition method, if the fair values of identifiable net assets exceed the value implied by the purchase price of the acquired company, the excess should be:

(Multiple Choice)

4.9/5 (42)

P Corporation issued 10,000 shares of common stock with a fair value of $25 per share for all the outstanding common stock of S Company in a business combination properly accounted for as an acquisition. The fair value of S Company's net assets on that date was $220,000. P Company also agreed to issue an additional 2,000 shares of common stock with a fair value of $50,000 to the former stockholders of S Company as an earnings contingency. Assuming that the contingency is expected to be met, the $50,000 fair value of the additional shares to be issued should be treated as a(n):

(Multiple Choice)

4.7/5 (35)

In a leveraged buyout, the portion of the net assets of the new corporation provided by the management group is recorded at:

(Multiple Choice)

4.8/5 (32)

Balance sheet information for Hope Corporation at January 1, 2016, is summarized as follows:

Hope's assets and liabilities are fairly valued except for plant assets that are undervalued by $200,000. On January 2, 2016, Robin Corporation issues 80,000 shares of its $10 par value common stock for all of Hope's net assets and Hope is dissolved. Market quotations for the two stocks on this date are:

Hope's assets and liabilities are fairly valued except for plant assets that are undervalued by $200,000. On January 2, 2016, Robin Corporation issues 80,000 shares of its $10 par value common stock for all of Hope's net assets and Hope is dissolved. Market quotations for the two stocks on this date are:  Robin pays the following fees and costs in connection with the combination:

Robin pays the following fees and costs in connection with the combination:  Required:

A. Calculate Robin's investment cost of Hope Corporation.

B. Calculate any goodwill from the business combination.

Required:

A. Calculate Robin's investment cost of Hope Corporation.

B. Calculate any goodwill from the business combination.

(Essay)

4.9/5 (31)

SFAS No. 142 requires that goodwill impairment be tested annually for each reporting unit. Discuss the necessary steps of the goodwill impairment test.

(Essay)

4.9/5 (43)

When the acquisition price of an acquired firm is less than the fair value of the identifiable net assets, all of the following are recorded at fair value EXCEPT:

(Multiple Choice)

4.8/5 (31)

Edina Company acquired the assets (except cash) and assumed the liabilities of Burns Company on January 1, 2016, paying $2,600,000 cash. Immediately prior to the acquisition, Burns Company's balance sheet was as follows:  Edina Company agreed to pay Burns Company's former stockholders $200,000 cash in 2017 if post- combination earnings of the combined company reached $1,000,000 during 2016.

Required:

A. Prepare the journal entry necessary for Edina Company to record the acquisition on January 1, 2016. It is expected that the earnings target is likely to be met.

B. Prepare the journal entry necessary for Edina Company in 2017 assuming the earnings contingency was not met.

Edina Company agreed to pay Burns Company's former stockholders $200,000 cash in 2017 if post- combination earnings of the combined company reached $1,000,000 during 2016.

Required:

A. Prepare the journal entry necessary for Edina Company to record the acquisition on January 1, 2016. It is expected that the earnings target is likely to be met.

B. Prepare the journal entry necessary for Edina Company in 2017 assuming the earnings contingency was not met.

(Essay)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)