Exam 3: Consolidated Financial Statements-Date of Acquisition

Exam 1: Introduction to Business Combinations and the Conceptual Framework35 Questions

Exam 2: Accounting for Business Combinations42 Questions

Exam 3: Consolidated Financial Statements-Date of Acquisition37 Questions

Exam 4: Consolidated Financial Statements After Acquisition42 Questions

Exam 5: Allocation and Depreciation of Differences Between Implied and Book Values36 Questions

Exam 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory35 Questions

Exam 7: Elimination of Unrealized Gains or Losses on Intercompany Sales of Property and Equipment33 Questions

Exam 8: Changes in Ownership Interest32 Questions

Exam 9: Intercompany Bond Holdings and Miscellaneous Topicsconsolidated Financial Statements33 Questions

Exam 10: Insolvencyliquidation and Reorganization34 Questions

Exam 11: International Financial Reporting Standards28 Questions

Exam 12: Accounting for Foreign Currency Transactions and Hedging Foreign Exchange Risk35 Questions

Exam 13: Translation of Financial Statements of Foreign Affiliates29 Questions

Exam 14: Reporting for Segments and for Interim Financial Periods44 Questions

Exam 15: Partnerships: Formation, Operation, and Ownership Changes39 Questions

Exam 16: Partnerships: Formation, Operation, and Ownership Changes35 Questions

Exam 17: Introduction to Fund Accounting29 Questions

Exam 18: Introduction to Accounting for State and Local Governmental Units34 Questions

Exam 19: Accounting for Nongovernment Nonbusiness Organizations: Colleges and Universities, Hospitals and Other Health Care Organizations39 Questions

Select questions type

Majority-owned subsidiaries should be excluded from the consolidated statements when:

(Multiple Choice)

4.9/5  (43)

(43)

A newly acquired subsidiary has pre-existing goodwill on its books. The parent company's consolidated balance sheet will:

(Multiple Choice)

4.8/5 (48)

P Company acquired 54,000 shares of the common stock of S Company on January 1, 2016, for $950,000 cash. The stockholders' equity section of S Company's balance sheet on that date was as follows:

On the date of acquisition, S Company owed P Company $10,000 on open account.

Required:

Present, in general journal form, the elimination entries for the preparation of a consolidated balance sheet workpaper on January 1, 2016. The difference between the value implied by the purchase price of the investment and the book value of the net assets acquired relates to subsidiary land.

On the date of acquisition, S Company owed P Company $10,000 on open account.

Required:

Present, in general journal form, the elimination entries for the preparation of a consolidated balance sheet workpaper on January 1, 2016. The difference between the value implied by the purchase price of the investment and the book value of the net assets acquired relates to subsidiary land.

(Essay)

4.9/5 (30)

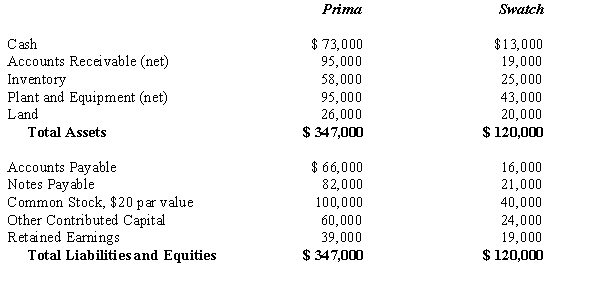

On January 1, 2016, Prima Company issued 1,500 of its $20 par value common shares with a fair value of $50 per share in exchange for 2,000 outstanding common shares of Swatch Company in a purchase transaction. Registration costs amounted to $1,700 paid in cash. Just prior to the acquisition, the balance sheets of the two companies were as follows:  Any differences between the book value of equity and the value implied by the purchase price relates to Land.

Required:

A. Prepare the journal entry on Prima's books to record the exchange of stock.

B. Prepare a Computation and Allocation Schedule for the Difference between book value and value implied by the purchase price.

C. Calculate the consolidated balance for each of the following accounts as of December 31, 2016:

1. Cash

2. Land

3. Common Stock

4. Other Contributed Capital

Any differences between the book value of equity and the value implied by the purchase price relates to Land.

Required:

A. Prepare the journal entry on Prima's books to record the exchange of stock.

B. Prepare a Computation and Allocation Schedule for the Difference between book value and value implied by the purchase price.

C. Calculate the consolidated balance for each of the following accounts as of December 31, 2016:

1. Cash

2. Land

3. Common Stock

4. Other Contributed Capital

(Essay)

4.7/5 (38)

Which of the following is a limitation of consolidated financial statements?

(Multiple Choice)

4.8/5 (36)

In a business combination accounted for as an acquisition, registration costs related to common stock issued by the parent company are:

(Multiple Choice)

4.7/5 (36)

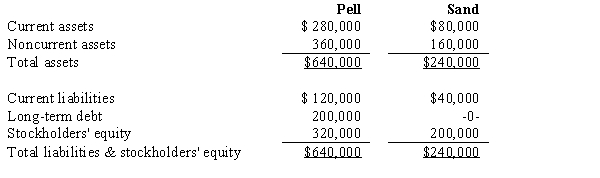

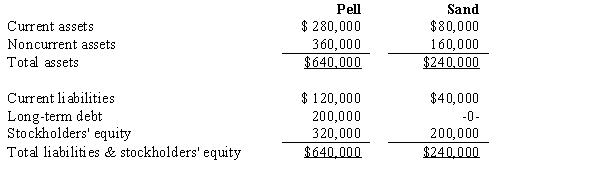

On January 1, 2016, Pell Company and Sand Company had condensed balance sheets as follows:  On January 2, 2016 Pell borrowed $240,000 and used the proceeds to purchase 90% of the outstanding common stock of Sand. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2016. Any difference between book value and the value implied by the purchase price relates to land. On Pell's January 2, 2016 consolidated balance sheet, noncurrent assets should be:

On January 2, 2016 Pell borrowed $240,000 and used the proceeds to purchase 90% of the outstanding common stock of Sand. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2016. Any difference between book value and the value implied by the purchase price relates to land. On Pell's January 2, 2016 consolidated balance sheet, noncurrent assets should be:

(Multiple Choice)

4.9/5 (41)

If an entity is not considered a VIE, the determination of consolidation is based on whether:

(Multiple Choice)

4.9/5 (41)

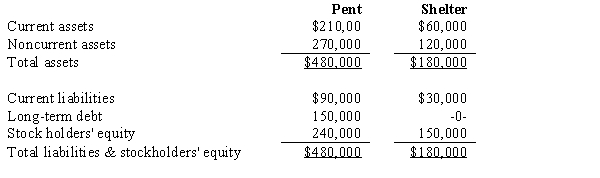

On January 1, 2016, Pent Company and Shelter Company had condensed balance sheets as follows:  On January 2, 2016 Pent borrowed $180,000 and used the proceeds to purchase 90% of the outstanding common stock of Shelter. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2016. Any difference between book value and the value implied by the purchase price relates to land. On Pent's January 2, 2016 consolidated balance sheet, noncurrent liabilities should be:

On January 2, 2016 Pent borrowed $180,000 and used the proceeds to purchase 90% of the outstanding common stock of Shelter. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2016. Any difference between book value and the value implied by the purchase price relates to land. On Pent's January 2, 2016 consolidated balance sheet, noncurrent liabilities should be:

(Multiple Choice)

4.8/5 (39)

Under the economic entity concept, consolidated financial statements are intended primarily for the benefit of the:

(Multiple Choice)

4.8/5 (49)

The primary beneficiary of a variable interest entity (VIE) must consolidate the VIE into its financial statements whenever:

(Multiple Choice)

4.8/5 (33)

On January 1, 2016, Pell Company and Sand Company had condensed balance sheets as follows:  On January 2, 2016 Pell borrowed $240,000 and used the proceeds to purchase 90% of the outstanding common stock of Sand. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2016. Any difference between book value and the value implied by the purchase price relates to land. On Pell's January 2, 2016 consolidated balance sheet, noncurrent liabilities should be:

On January 2, 2016 Pell borrowed $240,000 and used the proceeds to purchase 90% of the outstanding common stock of Sand. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2016. Any difference between book value and the value implied by the purchase price relates to land. On Pell's January 2, 2016 consolidated balance sheet, noncurrent liabilities should be:

(Multiple Choice)

4.8/5 (39)

On December 31, 2016, Priestly Company purchased a controlling interest in Shelter Company for $1,060,000. The consolidated balance sheet on December 31, 2016 reported noncontrolling interest in Shelter Company of $265,000.

On the date of acquisition, the stockholders' equity section of Shelter Company's balance sheet was as follows:  Required:

A.Compute the noncontrolling interest percentage on December 31, 2016.

B. Prepare the investment elimination entry made to prepare a consolidated balance sheet workpaper. Any difference between book value and the value implied by the purchase price relates to subsidiary land.

Required:

A.Compute the noncontrolling interest percentage on December 31, 2016.

B. Prepare the investment elimination entry made to prepare a consolidated balance sheet workpaper. Any difference between book value and the value implied by the purchase price relates to subsidiary land.

(Essay)

4.7/5 (28)

One reason a parent company may pay an amount less than the book value of the subsidiary's stock acquired is:

(Multiple Choice)

4.8/5 (33)

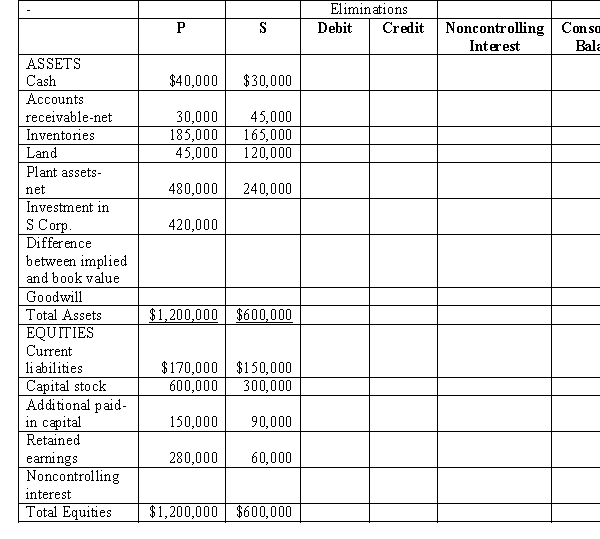

P Corporation paid $420,000 for 70% of S Corporation's $10 par common stock on December 31, 2016, when S Corporation's stockholders' equity was made up of $300,000 of Common Stock, $90,000 of Other Contributed Capital and $60,000 of Retained Earnings. S's identifiable assets and liabilities reflected their fair values on December 31, 2016, except for S's inventory which was undervalued by $60,000 and their land which was undervalued by $25,000. Balance sheets for P and S immediately after the business combination are presented in the partially completed work-paper below.  Required:

Complete the consolidated balance sheet workpaper for P Corporation and Subsidiary.

Required:

Complete the consolidated balance sheet workpaper for P Corporation and Subsidiary.

(Essay)

5.0/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)