Exam 2: Accounting for Business Combinations

Exam 1: Introduction to Business Combinations and the Conceptual Framework35 Questions

Exam 2: Accounting for Business Combinations42 Questions

Exam 3: Consolidated Financial Statements-Date of Acquisition37 Questions

Exam 4: Consolidated Financial Statements After Acquisition42 Questions

Exam 5: Allocation and Depreciation of Differences Between Implied and Book Values36 Questions

Exam 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory35 Questions

Exam 7: Elimination of Unrealized Gains or Losses on Intercompany Sales of Property and Equipment33 Questions

Exam 8: Changes in Ownership Interest32 Questions

Exam 9: Intercompany Bond Holdings and Miscellaneous Topicsconsolidated Financial Statements33 Questions

Exam 10: Insolvencyliquidation and Reorganization34 Questions

Exam 11: International Financial Reporting Standards28 Questions

Exam 12: Accounting for Foreign Currency Transactions and Hedging Foreign Exchange Risk35 Questions

Exam 13: Translation of Financial Statements of Foreign Affiliates29 Questions

Exam 14: Reporting for Segments and for Interim Financial Periods44 Questions

Exam 15: Partnerships: Formation, Operation, and Ownership Changes39 Questions

Exam 16: Partnerships: Formation, Operation, and Ownership Changes35 Questions

Exam 17: Introduction to Fund Accounting29 Questions

Exam 18: Introduction to Accounting for State and Local Governmental Units34 Questions

Exam 19: Accounting for Nongovernment Nonbusiness Organizations: Colleges and Universities, Hospitals and Other Health Care Organizations39 Questions

Select questions type

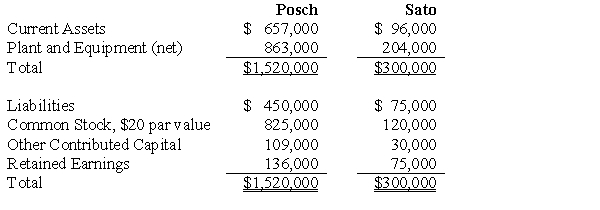

Posch Company issued 12,000 shares of its $20 par value common stock for the net assets of Sato Company in a business combination under which Sato Company will be merged into Posch Company. On the date of the combination, Posch Company common stock had a fair value of $30 per share. Balance sheets for Posch Company and Sato Company immediately prior to the combination were as follows:  If the business combination is treated as an acquisition and Sato Company's net assets have a fair value of $343,200, Posch Company's balance sheet immediately after the combination will include goodwill of:

If the business combination is treated as an acquisition and Sato Company's net assets have a fair value of $343,200, Posch Company's balance sheet immediately after the combination will include goodwill of:

(Multiple Choice)

4.7/5  (33)

(33)

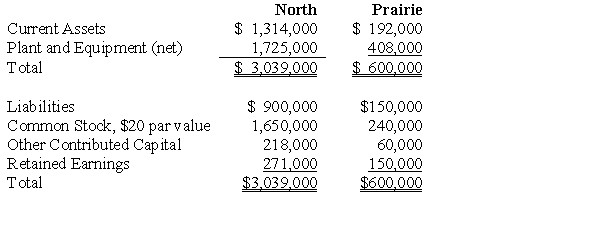

North Company issued 24,000 shares of its $20 par value common stock for the net assets of Prairie Company in business combination under which Prairie Company will be merged into North Company. On the date of the combination, North Company common stock had a fair value of $30 per share. Balance sheets for North Company and Prairie Company immediately prior to the combination were as follows:  If the business combination is treated as an acquisition and the fair value of Prairie Company's current assets is $270,000, its plant and equipment is $726,000, and its liabilities are $168,000, North Company's financial statements immediately after the combination will include:

If the business combination is treated as an acquisition and the fair value of Prairie Company's current assets is $270,000, its plant and equipment is $726,000, and its liabilities are $168,000, North Company's financial statements immediately after the combination will include:

(Multiple Choice)

4.7/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)