Exam 2: Accounting for Business Combinations

Exam 1: Introduction to Business Combinations and the Conceptual Framework35 Questions

Exam 2: Accounting for Business Combinations42 Questions

Exam 3: Consolidated Financial Statements-Date of Acquisition37 Questions

Exam 4: Consolidated Financial Statements After Acquisition42 Questions

Exam 5: Allocation and Depreciation of Differences Between Implied and Book Values36 Questions

Exam 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory35 Questions

Exam 7: Elimination of Unrealized Gains or Losses on Intercompany Sales of Property and Equipment33 Questions

Exam 8: Changes in Ownership Interest32 Questions

Exam 9: Intercompany Bond Holdings and Miscellaneous Topicsconsolidated Financial Statements33 Questions

Exam 10: Insolvencyliquidation and Reorganization34 Questions

Exam 11: International Financial Reporting Standards28 Questions

Exam 12: Accounting for Foreign Currency Transactions and Hedging Foreign Exchange Risk35 Questions

Exam 13: Translation of Financial Statements of Foreign Affiliates29 Questions

Exam 14: Reporting for Segments and for Interim Financial Periods44 Questions

Exam 15: Partnerships: Formation, Operation, and Ownership Changes39 Questions

Exam 16: Partnerships: Formation, Operation, and Ownership Changes35 Questions

Exam 17: Introduction to Fund Accounting29 Questions

Exam 18: Introduction to Accounting for State and Local Governmental Units34 Questions

Exam 19: Accounting for Nongovernment Nonbusiness Organizations: Colleges and Universities, Hospitals and Other Health Care Organizations39 Questions

Select questions type

Under SFAS 141R, what value of the assets and liabilities is reflected in the financial statements on the acquisition date of a business combination?

(Multiple Choice)

4.9/5  (34)

(34)

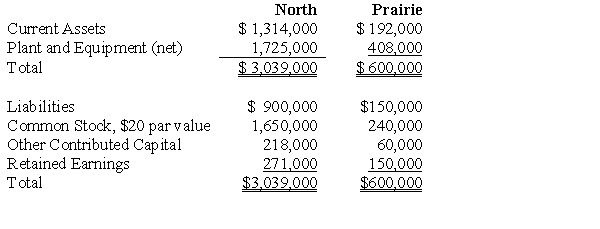

North Company issued 24,000 shares of its $20 par value common stock for the net assets of Prairie Company in business combination under which Prairie Company will be merged into North Company. On the date of the combination, North Company common stock had a fair value of $30 per share. Balance sheets for North Company and Prairie Company immediately prior to the combination were as follows:  If the business combination is treated as an acquisition and Prairie Company's net assets have a fair value of $686,400, North Company's balance sheet immediately after the combination will include goodwill of:

If the business combination is treated as an acquisition and Prairie Company's net assets have a fair value of $686,400, North Company's balance sheet immediately after the combination will include goodwill of:

(Multiple Choice)

4.8/5 (35)

P Company acquires all of the voting stock of S Company for $930,000 cash. The book values of S Company's assets are $800,000, but the fair values are $840,000 because land has a fair value above its book value. Goodwill from the combination is computed as:

(Multiple Choice)

4.9/5 (35)

In a business combination, which of the following costs are assigned to the valuation of the security?

(Multiple Choice)

4.9/5 (43)

If an impairment loss is recorded on previously recognized goodwill due to the transitional goodwill impairment test, the loss should be treated as a(n):

(Multiple Choice)

4.7/5 (38)

The fair value of assets and liabilities of the acquired entity is to be reflected in the financial statements of the combined entity. When the acquisition takes place over a period of time rather than all at once, at what time is the fair value of the assets and liabilities of the acquired entity determined under SFAS 141R?

(Multiple Choice)

5.0/5 (41)

In a period in which an impairment loss occurs, SFAS No. 142 requires each of the following note disclosures EXCEPT:

(Multiple Choice)

4.8/5 (35)

The first step in determining goodwill impairment involves comparing the:

(Multiple Choice)

4.7/5 (37)

On May 1, 2016, the Phil Company paid $1,200,000 for 80% of the outstanding common stock of Sage Corporation in a transaction properly accounted for as an acquisition. The recorded assets and liabilities of Sage Corporation on May 1, 2016, follow:  On May 1, 2016, it was determined that the inventory of Sage had a fair value of $220,000 and the property and equipment (net) has a fair value of $1,200,000. What is the amount of goodwill resulting from the business combination?

On May 1, 2016, it was determined that the inventory of Sage had a fair value of $220,000 and the property and equipment (net) has a fair value of $1,200,000. What is the amount of goodwill resulting from the business combination?

(Multiple Choice)

4.9/5 (45)

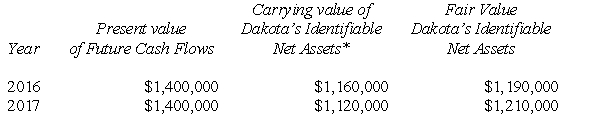

On January 1, 2013, Brighton Company acquired the net assets of Dakota Company for $1,580,000 cash. The fair value of Dakota's identifiable net assets was $1,310,000 on his date. Brighton Company decided to measure goodwill impairment using the present value of future cash flows to estimate the fair value of the reporting unit (Dakota). The information for these subsequent years is as follows:  * Identifiable net assets do not include goodwill.

Required:

A: For each year determine the amount of goodwill impairment, if any.

B: Prepare the journal entries needed each year to record the goodwill impairment (if any) on Brighton's books.

* Identifiable net assets do not include goodwill.

Required:

A: For each year determine the amount of goodwill impairment, if any.

B: Prepare the journal entries needed each year to record the goodwill impairment (if any) on Brighton's books.

(Essay)

4.8/5 (41)

A business combination is accounted for properly as an acquisition. Which of the following expenses related to effecting the business combination should enter into the determination of net income of the combined corporation for the period in which the expenses are incurred?

(Multiple Choice)

4.8/5 (40)

In a business combination accounted for as an acquisition, how should the excess of fair value of net assets acquired over the consideration paid be treated?

(Multiple Choice)

4.8/5 (39)

If the value implied by the purchase price of an acquired company exceeds the fair values of identifiable net assets, the excess should be:

(Multiple Choice)

4.8/5 (31)

Once a reporting unit is determined to have a fair value below its carrying value, the goodwill impairment loss is computed by comparing the:

(Multiple Choice)

4.9/5 (35)

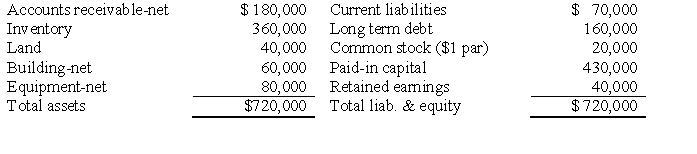

Maplewood Corporation purchased the net assets of West Corporation on January 2, 2016 for $560,000 and also paid $20,000 in direct acquisition costs. West's balance sheet on January

1, 2016 was as follows:  Fair values agree with book values except for inventory, land, and equipment, which have fair values of $400,000, $50,000 and $70,000, respectively. West has patent rights valued at $20,000.

Required:

A. Prepare Maplewood's general journal entry for the cash purchase of West's net assets.

B. Assume Maplewood Corporation purchased the net assets of West Corporation for $500,000 rather than $560,000, prepare the general journal entry.

Fair values agree with book values except for inventory, land, and equipment, which have fair values of $400,000, $50,000 and $70,000, respectively. West has patent rights valued at $20,000.

Required:

A. Prepare Maplewood's general journal entry for the cash purchase of West's net assets.

B. Assume Maplewood Corporation purchased the net assets of West Corporation for $500,000 rather than $560,000, prepare the general journal entry.

(Essay)

4.9/5 (43)

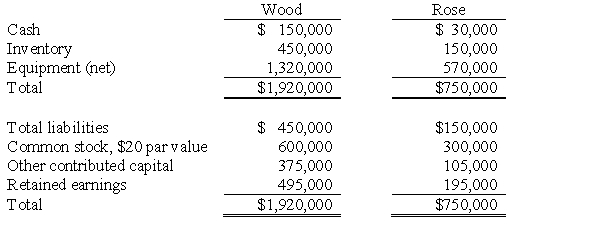

The following balance sheets were reported on January 1, 2016, for Wood Company and Rose Company:  Required:

Appraisals reveal that the inventory has a fair value $180,000, and the equipment has a current value of $615,000. The book value and fair value of liabilities are the same. Assuming that Wood Company wishes to acquire Rose for cash in an asset acquisition, determine the following cutoff amounts:

A. The purchase price above which Wood would record goodwill.

B. The purchase price at which Wood would record a $50,000 gain.

C. The purchase price below which Wood would obtain a "bargain."

D. The purchase price at which Wood would record $75,000 of goodwill.

Required:

Appraisals reveal that the inventory has a fair value $180,000, and the equipment has a current value of $615,000. The book value and fair value of liabilities are the same. Assuming that Wood Company wishes to acquire Rose for cash in an asset acquisition, determine the following cutoff amounts:

A. The purchase price above which Wood would record goodwill.

B. The purchase price at which Wood would record a $50,000 gain.

C. The purchase price below which Wood would obtain a "bargain."

D. The purchase price at which Wood would record $75,000 of goodwill.

(Essay)

4.9/5 (39)

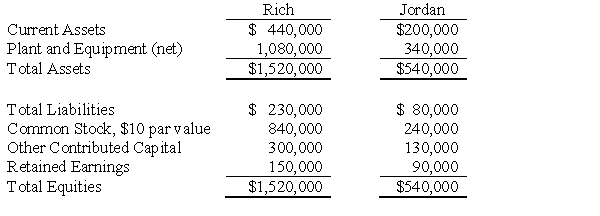

Condensed balance sheets for Rich Company and Jordan Company on January 1, 2016 are as follows:  On January 1, 2016 the stockholders of Rich and Jordan agreed to a consolidation whereby a new corporation, Cannon Company, would be formed to consolidate Rich and Jordan. Cannon Company issued 70,000 shares of its $20 par value common stock for the net assets of Rich and Jordan. On the date of consolidation, the fair values of Rich's and Jordan's current assets and liabilities were equal to their book values. The fair value of plant and equipment for each company was: Rich, $1,270,000; Jordan, $360,000.

An investment banking house estimated that the fair value of Cannon Company's common stock was $35 per share. Rich will incur $45,000 of direct acquisition costs and $15,000 in stock issue costs.

Required:

Prepare the journal entries to record the consolidation on the books of Cannon Company assuming that the consolidation is accounted for as an acquisition.

On January 1, 2016 the stockholders of Rich and Jordan agreed to a consolidation whereby a new corporation, Cannon Company, would be formed to consolidate Rich and Jordan. Cannon Company issued 70,000 shares of its $20 par value common stock for the net assets of Rich and Jordan. On the date of consolidation, the fair values of Rich's and Jordan's current assets and liabilities were equal to their book values. The fair value of plant and equipment for each company was: Rich, $1,270,000; Jordan, $360,000.

An investment banking house estimated that the fair value of Cannon Company's common stock was $35 per share. Rich will incur $45,000 of direct acquisition costs and $15,000 in stock issue costs.

Required:

Prepare the journal entries to record the consolidation on the books of Cannon Company assuming that the consolidation is accounted for as an acquisition.

(Essay)

4.9/5 (36)

P Company purchased the net assets of S Company for $225,000. On the date of P's purchase, S Company had no investments in marketable securities and $30,000 (book and fair value) of liabilities. The fair values of S Company's assets, when acquired, were:  How should the $45,000 difference between the fair value of the net assets acquired ($270,000) and the consideration paid ($225,000) be accounted for by P Company?

How should the $45,000 difference between the fair value of the net assets acquired ($270,000) and the consideration paid ($225,000) be accounted for by P Company?

(Multiple Choice)

4.9/5 (31)

The fair value of net identifiable assets of a reporting unit exclusive of goodwill of Y Company is $270,000. The carrying value of the reporting unit's net assets on Y Company's books is $320,000, including $50,000 goodwill. If the reported goodwill impairment for the unit is $10,000, what would be the fair value of the reporting unit?

(Multiple Choice)

4.8/5 (33)

The fair value of net identifiable assets exclusive of goodwill of a reporting unit of X Company is $300,000. On X Company's books, the carrying value of this reporting unit's net assets is $350,000, including $60,000 goodwill. If the fair value of the reporting unit is $335,000, what amount of goodwill impairment will be recognized for this unit?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)