Exam 14: Firms in Competitive Markets

Exam 1: Ten Principles of Economics220 Questions

Exam 2: Thinking Like an Economist284 Questions

Exam 3: Interdependence and the Gains From Trade192 Questions

Exam 4: The Market Forces of Supply and Demand277 Questions

Exam 5: Elasticity and Its Application222 Questions

Exam 6: Supply, Demand, and Government Policies321 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets218 Questions

Exam 8: Applications: The Costs of Taxation203 Questions

Exam 9: Application: International Trade214 Questions

Exam 10: Externalities204 Questions

Exam 11: Public Goods and Common Resources182 Questions

Exam 12: The Design of the Tax System225 Questions

Exam 13: The Costs of Production261 Questions

Exam 14: Firms in Competitive Markets243 Questions

Exam 15: Monopoly231 Questions

Exam 16: Monopolistic Competition246 Questions

Exam 17: Oligopoly204 Questions

Exam 18: The Markets for the Factors of Production232 Questions

Exam 19: Earnings and Discrimination230 Questions

Exam 20: Income Inequality and Poverty194 Questions

Exam 21: The Theory of Consumer Choice209 Questions

Exam 22: Frontiers in Microeconomics185 Questions

Exam 23: Measuring a Nations Income231 Questions

Exam 24: Measuring the Cost of Living214 Questions

Exam 25: Production and Growth187 Questions

Exam 26: Saving, Investment, and the Financial System225 Questions

Exam 27: Tools of Finance198 Questions

Exam 28: Unemployment and Its Natural Rate361 Questions

Exam 29: The Monetary System210 Questions

Exam 30: Money Growth and Inflation201 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts194 Questions

Exam 32: A Macroeconomic Theory of the Open Economy188 Questions

Exam 33: Aggregate Demand and Aggregate Supply189 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand207 Questions

Exam 35: The Short-Run Tradeoff Between Inflation and Unemployment223 Questions

Exam 36: Six Debates Over Macroeconomic Policy154 Questions

Select questions type

Table 14-5

Suppose that a firm in a competitive market faces the following revenues and costs:

Quantity (Units) Marginal Cost (Dollars) Marginal Revenue (Dollars) 12 5 7 13 6 7 14 7 7 15 8 7 16 9 7 17 10 7

-Refer to Table 14-5. If the firm is maximizing profit, how much profit is it earning?

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

D

For firms operating in a perfectly competitive market, price must always be greater than marginal revenue.

Free

(True/False)

4.8/5 (37)

Correct Answer:Verified

False

A competitive market is in long-run equilibrium. If demand decreases, we can be certain that price will

Free

(Multiple Choice)

4.9/5 (27)

Correct Answer:Verified

C

News reports from the western United States occasionally report incidents of cattle ranchers slaughtering a large number of newborn calves and burying them in mass graves rather than transporting them to markets. Assuming that this is rational behavior by profit-maximizing "firms," explain what economic factors may influence such behavior.

(Essay)

4.9/5 (30)

For any competitive market, the supply curve is closely related to the

(Multiple Choice)

4.9/5 (36)

A golf course in Fargo, North Dakota - where it is very cold in the winter - is closed between November 1 and April 1. If the owner of the golf course is rational, what criterion does he or she use in deciding to close the course for this extended period of time?

(Essay)

4.7/5 (32)

Raiman's Shoe Repair produces custom-made shoes. When Mr. Raiman produces 12 pairs per week, the marginal cost of the 12th pair is $84, and the marginal revenue of the 12th pair is $70. What would you advise Mr. Raiman to do?

(Multiple Choice)

4.9/5 (32)

A dairy farmer must be able to calculate sunk costs in order to determine how much revenue the farm receives for the typical gallon of milk.

(True/False)

5.0/5 (35)

What name do economists have for a cost that has already been committed and cannot be recovered?

(Short Answer)

4.8/5 (41)

"The water that comes out of your faucets at home is not supplied by a competitive firm." Explain why this statement is correct.

(Essay)

4.8/5 (32)

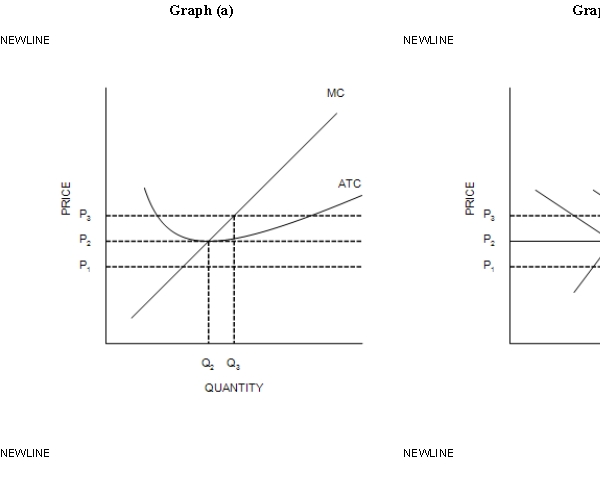

Figure 14-7

-Refer to Figure 14-7. When the market is in long-run equilibrium at point W in graph (b), the firm represented in graph (a) will

-Refer to Figure 14-7. When the market is in long-run equilibrium at point W in graph (b), the firm represented in graph (a) will

(Multiple Choice)

4.7/5 (34)

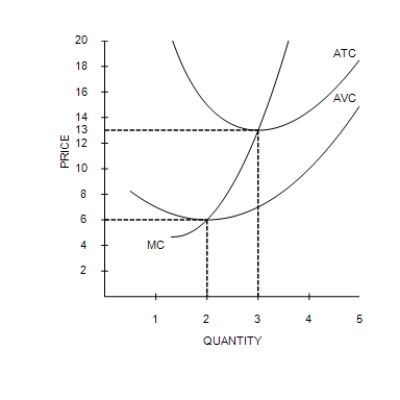

Figure 14-1

Suppose that a firm in a competitive market has the following cost curves:

-Refer to Figure 14-1. If the market price is exactly $13, the firm will earn

-Refer to Figure 14-1. If the market price is exactly $13, the firm will earn

(Multiple Choice)

4.8/5 (35)

In a competitive market, is the long-run supply curve typically more elastic than the short-run supply curve, or is it less elastic than the short-run supply curve?

(Essay)

4.8/5 (33)

Figure 14-1

Suppose that a firm in a competitive market has the following cost curves:

-Refer to Figure 14-1. The firm will earn a negative economic profit but remain in business in the short run if the market price is

(Multiple Choice)

4.8/5 (32)

For a firm operating in a perfectly competitive industry, total revenue, marginal revenue, and average revenue are all equal.

(True/False)

4.8/5 (44)

Because there are many buyers and sellers in a perfectly competitive market, no one seller can influence the market price.

(True/False)

4.8/5 (37)

A firm will shut down in the short run if revenue is not sufficient to cover all of its fixed costs of production.

(True/False)

4.7/5 (38)

Profit-maximizing firms enter a competitive market when existing firms in that market have

(Multiple Choice)

4.8/5 (29)

Table 14-2

The table represents a demand curve faced by a firm in a competitive market.

Price (Dollarsper unit) Quantity Demanded (Units) 5 0 5 1 5 2 5 3 5 4 5 5

-Refer to Table 14-2. For this firm, the marginal revenue from selling the next unit is

(Multiple Choice)

4.8/5 (36)

Because there are many sellers in a competitive market, individual firms are unable to maximize profits.

(True/False)

4.9/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)