Exam 4: The Market Forces of Supply and Demand

Exam 1: Ten Principles of Economics220 Questions

Exam 2: Thinking Like an Economist284 Questions

Exam 3: Interdependence and the Gains From Trade192 Questions

Exam 4: The Market Forces of Supply and Demand277 Questions

Exam 5: Elasticity and Its Application222 Questions

Exam 6: Supply, Demand, and Government Policies321 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets218 Questions

Exam 8: Applications: The Costs of Taxation203 Questions

Exam 9: Application: International Trade214 Questions

Exam 10: Externalities204 Questions

Exam 11: Public Goods and Common Resources182 Questions

Exam 12: The Design of the Tax System225 Questions

Exam 13: The Costs of Production261 Questions

Exam 14: Firms in Competitive Markets243 Questions

Exam 15: Monopoly231 Questions

Exam 16: Monopolistic Competition246 Questions

Exam 17: Oligopoly204 Questions

Exam 18: The Markets for the Factors of Production232 Questions

Exam 19: Earnings and Discrimination230 Questions

Exam 20: Income Inequality and Poverty194 Questions

Exam 21: The Theory of Consumer Choice209 Questions

Exam 22: Frontiers in Microeconomics185 Questions

Exam 23: Measuring a Nations Income231 Questions

Exam 24: Measuring the Cost of Living214 Questions

Exam 25: Production and Growth187 Questions

Exam 26: Saving, Investment, and the Financial System225 Questions

Exam 27: Tools of Finance198 Questions

Exam 28: Unemployment and Its Natural Rate361 Questions

Exam 29: The Monetary System210 Questions

Exam 30: Money Growth and Inflation201 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts194 Questions

Exam 32: A Macroeconomic Theory of the Open Economy188 Questions

Exam 33: Aggregate Demand and Aggregate Supply189 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand207 Questions

Exam 35: The Short-Run Tradeoff Between Inflation and Unemployment223 Questions

Exam 36: Six Debates Over Macroeconomic Policy154 Questions

Select questions type

Which of the following changes would not shift the supply curve for a good or service?

Free

(Multiple Choice)

4.9/5  (35)

(35)

Correct Answer: Verified

Verified

B

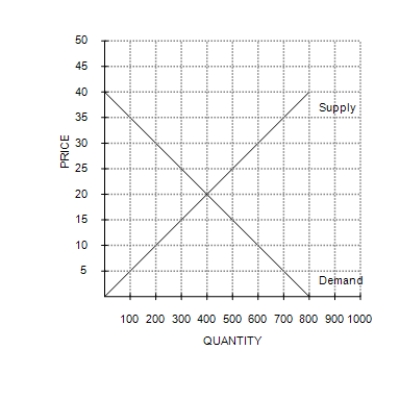

Figure 4-7

-Refer to Figure 4-7. Equilibrium price and quantity are, respectively,

-Refer to Figure 4-7. Equilibrium price and quantity are, respectively,

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

C

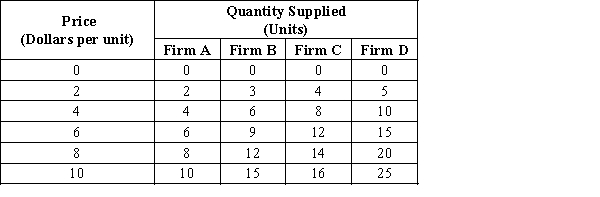

Table 4-4

-Refer to Table 4-4. If these are the only four sellers in the market, then when the price increases from $4 to $6, the market quantity supplied

-Refer to Table 4-4. If these are the only four sellers in the market, then when the price increases from $4 to $6, the market quantity supplied

Free

(Multiple Choice)

4.7/5 (32)

Correct Answer:Verified

B

The market supply curve shows how the total quantity supplied of a good varies as input prices vary, holding constant all the other factors that influence producers' decisions about how much to sell.

(True/False)

4.9/5 (34)

A decrease in the price of pizza will shift the supply curve for pizza to the left.

(True/False)

4.8/5 (27)

Sellers as a group determine the demand for a product, and buyers as a group determine the supply of a product.

(True/False)

4.8/5 (35)

What would happen to the equilibrium price and quantity of lattés if the cost of producing steamed milk, which is used to make lattés, rises?

(Multiple Choice)

4.8/5 (32)

Whenever a determinant of supply other than price changes, the supply curve shifts.

(True/False)

4.8/5 (34)

The law of demand states that, other things equal, when the price of a good rises, the quantity demanded of the good rises, and when the price falls, the quantity demanded falls.

(True/False)

4.7/5 (32)

A decrease in the price of sugar will shift the supply curve for cookies to the right.

(True/False)

4.9/5 (27)

If the price of steel, an input into the production of automobiles, rises, and at the same time the price of gasoline rises, what will happen to the equilibrium price and quantity of automobiles?

(Essay)

4.7/5 (30)

Which of the following events would cause the price of oranges to fall?

(Multiple Choice)

4.9/5 (32)

Table 4-1

Price (Dollarsper unit) Quantity Demanded (Units) 16 80 21

-Refer to Table 4-1. If the law of demand applies to this good, then Q1 could be

(Multiple Choice)

4.7/5 (34)

Suppose the United States had a short-term shortage of farmers. Which market mechanisms would adjust to remove the shortage?

(Multiple Choice)

4.8/5 (31)

Figure 4-6  -Refer to Figure 4-6. The shift from S to S' in the market for muffins could be caused by

-Refer to Figure 4-6. The shift from S to S' in the market for muffins could be caused by

(Multiple Choice)

4.8/5 (40)

If a good or service has only one seller, then the seller is called a monopoly.

(True/False)

4.7/5 (35)

What would happen to the equilibrium price and quantity of smartphones if consumers' incomes rise and smartphones are a normal good?

(Multiple Choice)

4.9/5 (33)

Suppose the supply and demand of corn both increase. As a result, what will happen to the equilibrium price and equilibrium quantity in the market?

(Essay)

4.8/5 (27)

If something happens to alter the quantity supplied at any given price, then we move along the fixed supply curve to a new quantity supplied.

(True/False)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)