Exam 6: Reporting and Analyzing Inventory

Exam 1: Introduction to Financial Statements218 Questions

Exam 2: A Further Look at Financial Statements238 Questions

Exam 3: The Accounting Information System275 Questions

Exam 4: Accrual Accounting Concepts310 Questions

Exam 5: Merchandising Operations and the Multiple-Step Income Statement261 Questions

Exam 6: Reporting and Analyzing Inventory250 Questions

Exam 7: Fraud, Internal Control, and Cash245 Questions

Exam 8: Reporting and Analyzing Receivables262 Questions

Exam 9: Reporting and Analyzing Long-Lived Assets276 Questions

Exam 10: Reporting and Analyzing Liabilities294 Questions

Exam 11: Reporting and Analyzing Stockholders Equity263 Questions

Exam 12: Statement of Cash Flows216 Questions

Exam 13: Financial Analysis: The Big Picture271 Questions

Exam 14: Time Value of Money295 Questions

Select questions type

Condensed income statements for Werly Corporation are shown below for two years.  Compute the corrected net income for 2013 and 2014 assuming that the inventory as of the end of 2013 was mistakenly overstated by $5,000.

2013 $ __________ 2014 $__________

Compute the corrected net income for 2013 and 2014 assuming that the inventory as of the end of 2013 was mistakenly overstated by $5,000.

2013 $ __________ 2014 $__________

(Short Answer)

4.8/5  (39)

(39)

Many companies use just-in-time inventory methods. Which of the following is not an advantage of this method?

(Multiple Choice)

4.8/5 (33)

Which inventory method generally results in costs allocated to ending inventory that will approximate their current cost?

(Multiple Choice)

4.9/5 (45)

Johnson Company reports the following for the month of June.  (a) Compute the cost of the ending inventory and the cost of goods sold under (1) FIFO, (2) LIFO, and (3) average cost.

(b) Which costing method gives the highest ending inventory? The highest cost of goods sold? Why?

(c) How do the average-cost values for ending inventory and cost of goods sold relate to ending inventory and cost of goods sold for FIFO and LIFO?

(a) Compute the cost of the ending inventory and the cost of goods sold under (1) FIFO, (2) LIFO, and (3) average cost.

(b) Which costing method gives the highest ending inventory? The highest cost of goods sold? Why?

(c) How do the average-cost values for ending inventory and cost of goods sold relate to ending inventory and cost of goods sold for FIFO and LIFO?

(Essay)

4.8/5 (44)

An error in the ending inventory of the current period will have a similar effect on net income of the next accounting period.

(True/False)

4.8/5 (38)

For companies that use a perpetual inventory system, all of the following are purposes for taking a physical inventory except to:

(Multiple Choice)

4.8/5 (38)

Plato Company reports the following for the month of June. ![Plato Company reports the following for the month of June. Instructions (a) Calculate the cost of the ending inventory and the cost of goods sold for each cost flow assumption, using a perpetual inventory system. Assume a sale of 570 units occurred on June 15 for a selling price of $8 and a sale of 600 units on June 27 for $9. (Note: For the average-cost method, round unit cost to three decimal places.) (b) Why is the average unit cost not $6 [($5 + $6 + $7) / 3 = $6]?](https://storage.examlex.com/TB4437/11eb232e_d402_9990_aa27_5541aa00bf1d_TB4437_00.jpg) Instructions

(a) Calculate the cost of the ending inventory and the cost of goods sold for each cost flow assumption, using a perpetual inventory system. Assume a sale of 570 units occurred on June 15 for a selling price of $8 and a sale of 600 units on June 27 for $9. (Note: For the average-cost method, round unit cost to three decimal places.)

(b) Why is the average unit cost not $6 [($5 + $6 + $7) / 3 = $6]?

Instructions

(a) Calculate the cost of the ending inventory and the cost of goods sold for each cost flow assumption, using a perpetual inventory system. Assume a sale of 570 units occurred on June 15 for a selling price of $8 and a sale of 600 units on June 27 for $9. (Note: For the average-cost method, round unit cost to three decimal places.)

(b) Why is the average unit cost not $6 [($5 + $6 + $7) / 3 = $6]?

(Essay)

4.8/5 (34)

Which of the following should not be included in the physical inventory of a company?

(Multiple Choice)

4.8/5 (34)

A manufacturer's inventory consists of raw materials, work in process, and finished goods.

(True/False)

4.9/5 (43)

Inventory costing methods place primary reliance on assumptions about the flow of

(Multiple Choice)

4.8/5 (42)

An overstatement of ending inventory in one period results in

(Multiple Choice)

4.8/5 (40)

At May 1, 2014, Heineken Company had beginning inventory consisting of 200 units with a unit cost of $7. During May, the company purchased inventory as follows: 400 units at $7

600 units at $8

The company sold 1,000 units during the month for $12 per unit. Heineken uses the average cost method. The value of Heineken's inventory at May 31, 2014 is

(Multiple Choice)

4.7/5 (35)

The difference between ending inventory using LIFO and ending inventory using FIFO is referred to as the

(Multiple Choice)

4.9/5 (31)

Serene Stereos has the following inventory data:  A physical count of merchandise inventory on November 30 reveals that there are 100 units on hand. Cost of goods sold under FIFO is

A physical count of merchandise inventory on November 30 reveals that there are 100 units on hand. Cost of goods sold under FIFO is

(Multiple Choice)

4.8/5 (40)

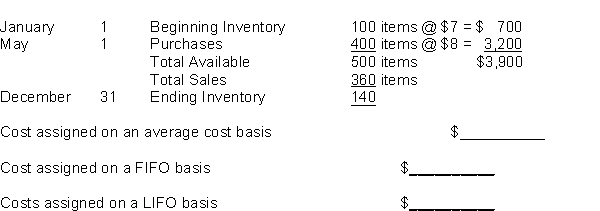

Compute the cost to be assigned to ending inventory for each of the methods indicated given the following information about purchases and sales during the year.

(Essay)

4.7/5 (37)

The Cain Company has just completed a physical inventory count at year end, December 31, 2014. Only the items on the shelves, in storage, and in the receiving area were counted and costed on the FIFO basis. The inventory amounted to $80,000. During the audit, the independent CPA discovered the following additional information:

(a) There were goods in transit on December 31, 2014, from a supplier with terms FOB destination, costing $10,000. Because the goods had not arrived, they were excluded from the physical inventory count.

(b) On December 27, 2014, a regular customer purchased goods for cash amounting to $1,000 and had them shipped to a bonded warehouse for temporary storage on December 28, 2014. The goods were shipped via common carrier with terms FOB shipping point. The customer picked the goods up from the warehouse on January 4, 2015. Cain Company had paid $500 for the goods and, because they were in storage, Cain included them in the physical inventory count.

(c) Cain Company, on the date of the inventory, received notice from a supplier that goods ordered earlier, at a cost of $4,000, had been delivered to the transportation company on December 28, 2014; the terms were FOB shipping point. Because the shipment had not arrived on December 31, 2014, it was excluded from the physical inventory.

(d) On December 31, 2014, there were goods in transit to customers, with terms FOB shipping point, amounting to $800 (expected delivery on January 8, 2015). Because the goods had been shipped, they were excluded from the physical inventory count.

(e) On December 31, 2014, Cain Company shipped $2,500 worth of goods to a customer, FOB destination. The goods arrived on January 5, 2014. Because the goods were not on hand, they were not included in the physical inventory count.

(f) Cain Company, as the consignee, had goods on consignment that cost $3,000. Because these goods were on hand as of December 31, 2014, they were included in the physical inventory count.

Instructions

Analyze the above information and calculate a corrected amount for the ending inventory. Explain the basis for your treatment of each item.

(Essay)

4.8/5 (33)

If prices never changed there would be no need for alternative inventory methods.

(True/False)

4.8/5 (35)

Which of the following items will increase inventoriable costs for the buyer of goods?

(Multiple Choice)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)