Exam 23: Evaluating Variances From Standard Costs

Exam 1: Introduction to Accounting and Business243 Questions

Exam 2: Analyzing Transactions234 Questions

Exam 3: The Adjusting Process225 Questions

Exam 4: The Accounting Cycle211 Questions

Exam 5: Accounting for Retail Businesses273 Questions

Exam 6: Inventories236 Questions

Exam 7: Internal Control and Cash197 Questions

Exam 8: Receivables210 Questions

Exam 9: Long-Term Assets: Fixed and Intangible243 Questions

Exam 10: Liabilities: Current, Installment Notes, and Contingencies199 Questions

Exam 11: Liabilities: Bonds Payable172 Questions

Exam 12: Corporations: Organization, Stock Transactions, and Dividends221 Questions

Exam 13: Statement of Cash Flows193 Questions

Exam 14: Financial Statement Analysis206 Questions

Exam 15: Introduction to Managerial Accounting244 Questions

Exam 16: Job Order Costing212 Questions

Exam 17: Process Cost Systems196 Questions

Exam 18: Activity-Based Costing109 Questions

Exam 19: Support Department and Joint Cost Allocation172 Questions

Exam 20: Cost-Volume-Profit Analysis247 Questions

Exam 21: Variable Costing for Management Analysis136 Questions

Exam 22: Budgeting197 Questions

Exam 23: Evaluating Variances From Standard Costs172 Questions

Exam 24: Evaluating Decentralized Operations210 Questions

Exam 25: Differential Analysis and Product Pricing157 Questions

Exam 26: Capital Investment Analysis191 Questions

Exam 27: Lean Manufacturing and Activity Analysis134 Questions

Exam 28: The Balanced Scorecard and Corporate Social Responsibility170 Questions

Exam 29: Investments137 Questions

Select questions type

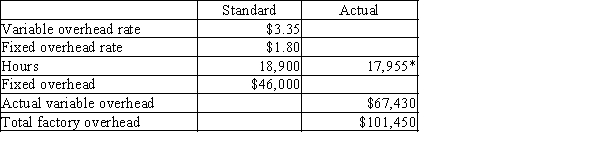

*Actual hours are equal to standard hours for units produced.

-The variable factory overhead controllable variance is

*Actual hours are equal to standard hours for units produced.

-The variable factory overhead controllable variance is

(Multiple Choice)

4.9/5  (32)

(32)

The principle of exceptions allows managers to focus on correcting variances between standard costs and actual costs.

(True/False)

4.9/5 (42)

Standards are performance goals used to evaluate and control operations.

(True/False)

4.9/5 (38)

*Actual hours are equal to standard hours for units produced.

-Planned sales are 10,000 units at $7.00 per unit. Actual sales are 11,000 units at $6.50 per unit. Which of the following statements is not true?

(Multiple Choice)

4.8/5 (37)

Standard and actual costs for direct labor for the manufacture of 300 units of product were as follows:

Actual costs

125 hours at $54

Standard costs

131 hours at $53

Determine the direct labor (a) time variance, (b) rate variance, and (c) total cost variance.

(Essay)

4.9/5 (38)

At the end of the fiscal year, the variances from standard are usually transferred to the finished goods account.

(True/False)

4.8/5 (39)

Accounting systems that use standards for product costs are called standard cost systems.

(True/False)

4.7/5 (35)

The standard costs and actual costs for direct labor in the manufacture of 2,500 units of product are as follows:  The direct labor time variance is

The direct labor time variance is

(Multiple Choice)

4.8/5 (38)

If the price paid per unit differs from the standard price per unit for direct materials, the variance is a _____ variance.

(Multiple Choice)

4.9/5 (35)

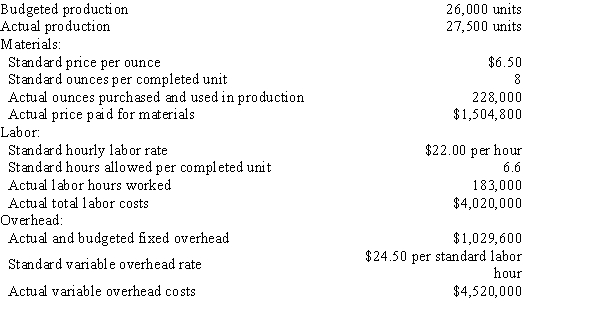

The following data are given for Harry Company:  Overhead is applied on standard labor hours. (Round interim calculations to the nearest cent.)

-The direct labor time variance is

Overhead is applied on standard labor hours. (Round interim calculations to the nearest cent.)

-The direct labor time variance is

(Multiple Choice)

4.8/5 (27)

*Actual hours are equal to standard hours for units produced.

-The total factory overhead cost variance is

(Multiple Choice)

4.9/5 (30)

The standard costs and actual costs for direct materials for the manufacture of 2,500 actual units of product are as follows:  The direct materials quantity variance is

The direct materials quantity variance is

(Multiple Choice)

4.8/5 (40)

If the wage rate paid per hour differs from the standard wage rate per hour for direct labor, the variance is a _____ variance.

(Multiple Choice)

4.8/5 (41)

The following data relate to direct labor costs for the current period: Standard costs

9,000 hours at $5.50

Actual costs

8,500 hours at $5.75

The direct labor rate variance is

(Multiple Choice)

4.9/5 (38)

The following data are given for Harry Company: Overhead is applied on standard labor hours. (Round interim calculations to the nearest cent.)

-The direct labor rate variance is

(Multiple Choice)

4.9/5 (46)

The standard factory overhead rate is $7.50 per machine hour ($6.20 for variable factory overhead and $1.30 for fixed factory overhead) based on 100% of normal capacity of 80,000 machine hours. The standard cost and the actual cost of factory overhead for the production of 15,000 units during August were as follows:

-Favorable volume variances may be harmful when

-Favorable volume variances may be harmful when

(Multiple Choice)

4.9/5 (48)

The volume variance measures the use of fixed factory overhead resources.

(True/False)

4.8/5 (36)

Using the following information, prepare a factory overhead cost budget for Andover Company where the total factory overhead cost is $75,500 at normal capacity (100%). Include capacity at 75%, 90%, 100%, and 110%. Total variable cost is $6.25 per unit and total fixed costs are $38,000. The information is for the month ending August 31. (Hint: Determine units produced at normal capacity.)

(Essay)

4.8/5 (52)

Match each of the following formulas and phrases with the term (a-e) it describes.

-(Actual Price - Standard Price) × Actual Quantity

(Multiple Choice)

4.8/5 (41)

Which of the following conditions normally would not indicate that standard costs should be revised?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)