Exam 23: Evaluating Variances From Standard Costs

Exam 1: Introduction to Accounting and Business243 Questions

Exam 2: Analyzing Transactions234 Questions

Exam 3: The Adjusting Process225 Questions

Exam 4: The Accounting Cycle211 Questions

Exam 5: Accounting for Retail Businesses273 Questions

Exam 6: Inventories236 Questions

Exam 7: Internal Control and Cash197 Questions

Exam 8: Receivables210 Questions

Exam 9: Long-Term Assets: Fixed and Intangible243 Questions

Exam 10: Liabilities: Current, Installment Notes, and Contingencies199 Questions

Exam 11: Liabilities: Bonds Payable172 Questions

Exam 12: Corporations: Organization, Stock Transactions, and Dividends221 Questions

Exam 13: Statement of Cash Flows193 Questions

Exam 14: Financial Statement Analysis206 Questions

Exam 15: Introduction to Managerial Accounting244 Questions

Exam 16: Job Order Costing212 Questions

Exam 17: Process Cost Systems196 Questions

Exam 18: Activity-Based Costing109 Questions

Exam 19: Support Department and Joint Cost Allocation172 Questions

Exam 20: Cost-Volume-Profit Analysis247 Questions

Exam 21: Variable Costing for Management Analysis136 Questions

Exam 22: Budgeting197 Questions

Exam 23: Evaluating Variances From Standard Costs172 Questions

Exam 24: Evaluating Decentralized Operations210 Questions

Exam 25: Differential Analysis and Product Pricing157 Questions

Exam 26: Capital Investment Analysis191 Questions

Exam 27: Lean Manufacturing and Activity Analysis134 Questions

Exam 28: The Balanced Scorecard and Corporate Social Responsibility170 Questions

Exam 29: Investments137 Questions

Select questions type

Standard costs are used in companies for a variety of reasons. Which of the following is not one of the benefits for using standard costs?

(Multiple Choice)

4.8/5  (27)

(27)

The standard factory overhead rate is $7.50 per machine hour ($6.20 for variable factory overhead and $1.30 for fixed factory overhead) based on 100% of normal capacity of 80,000 machine hours. The standard cost and the actual cost of factory overhead for the production of 15,000 units during August were as follows:

-The following data are given for Bahia Company:

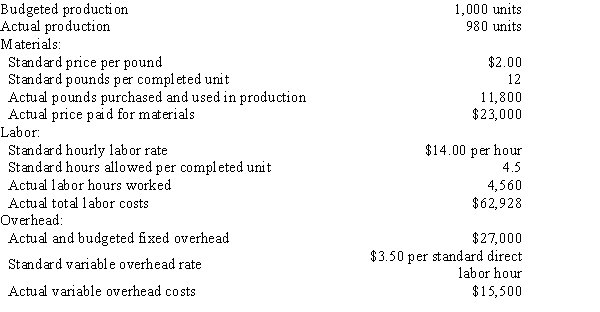

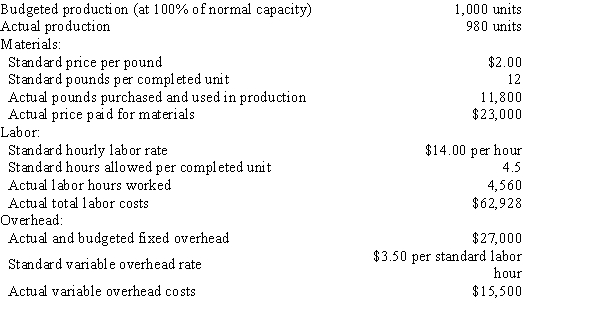

-The following data are given for Bahia Company:  Overhead is applied on standard labor hours.The variable factory overhead controllable variance is

Overhead is applied on standard labor hours.The variable factory overhead controllable variance is

(Multiple Choice)

4.8/5 (39)

Because accountants have financial expertise, they are the only ones that are able to set standard costs for the production area.

(True/False)

4.8/5 (39)

Ajay Company records standard costs and variances in its accounts. Journalize the entry to record the purchase of 6,000 widgets at $8.00 per unit, assuming widgets have a standard cost of $8.15 per unit.

(Essay)

4.9/5 (29)

Favorable fixed factory overhead volume variances are never harmful, since achieving them encourages managers to run the factory above normal capacity.

(True/False)

4.8/5 (45)

If the standard to produce a given amount of product is 1,000 units of direct materials at $11 and the actual direct materials used are 800 units at $12, the direct materials price variance is $800 unfavorable.

(True/False)

4.9/5 (47)

Match each of the following phrases with the term (a-e) it describes.

-Summarizes actual costs, standard costs, and the differences for units produced

(Multiple Choice)

4.9/5 (42)

Jaxson Corporation has the following data related to direct labor costs for September: actual costs for 10,200 hours at $15.75 per hour and standard costs for 10,800 hours at $15.50 per hour. The direct labor time variance is

(Multiple Choice)

4.9/5 (42)

Since the variable factory overhead controllable variance measures the efficiency of using variable overhead resources, if budgeted variable overhead exceeds actual results, the variance is favorable.

(True/False)

4.9/5 (40)

Rosser Company records standard costs and variances in its accounts. Rosser Company produces a container that requires 4 yards of material per unit. The standard price of one yard of material is $4.50. During the month, 9,500 chairs were manufactured using 37,300 yards of material.

Journalize the entry to record the direct materials used in production.

(Essay)

4.8/5 (31)

The principle of exceptions allows managers to focus on correcting variances between

(Multiple Choice)

4.8/5 (28)

Lucy Corporation purchased and used 129,000 board feet of lumber in production at a total cost of $1,548,000. Original production had been budgeted for 22,000 units with a standard materials quantity of 5.7 board feet per unit and a standard price of $12 per board foot. Actual production was 23,500 units.

-The direct materials quantity variance is

(Multiple Choice)

4.9/5 (30)

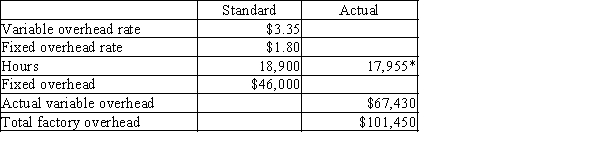

*Actual hours are equal to standard hours for units produced.

-An unfavorable fixed overhead volume variance can be due to all of the following except

*Actual hours are equal to standard hours for units produced.

-An unfavorable fixed overhead volume variance can be due to all of the following except

(Multiple Choice)

4.8/5 (40)

The standard factory overhead rate is $7.50 per machine hour ($6.20 for variable factory overhead and $1.30 for fixed factory overhead) based on 100% of normal capacity of 80,000 machine hours. The standard cost and the actual cost of factory overhead for the production of 15,000 units during August were as follows:

-The following data are given for Bahia Company:  Overhead is applied on standard labor hours.The fixed factory overhead volume variance is

Overhead is applied on standard labor hours.The fixed factory overhead volume variance is

(Multiple Choice)

4.8/5 (29)

Match each of the following formulas and phrases with the term (a-e) it describes.

-(Actual Rate per Hour - Standard Rate per Hour) × Actual Hours

(Multiple Choice)

4.9/5 (34)

Variances from standard costs are usually not included in reports to stockholders.

(True/False)

4.8/5 (30)

The standard factory overhead rate is $7.50 per machine hour ($6.20 for variable factory overhead and $1.30 for fixed factory overhead) based on 100% of normal capacity of 80,000 machine hours. The standard cost and the actual cost of factory overhead for the production of 15,000 units during August were as follows:

-The fixed factory overhead volume variance is

(Multiple Choice)

4.7/5 (37)

Aquatic Corp.'s standard material requirement to produce one Model 2000 is 15 pounds of material at $110 per pound. Last month, Aquatic purchased 170,000 pounds of material at a total cost of $17,850,000. It used 162,000 pounds to produce 10,000 units of Model 2000.

Determine the direct materials price variance and direct materials quantity variance, and indicate whether each variance is favorable or unfavorable.

(Essay)

4.8/5 (41)

The following data relate to direct materials costs for February:

Materials cost per yard: standard, $2.00; actual, $2.10

Yards per unit: standard, 4.5 yards; actual, 4.75 yards

Units of production: 9,500

-The direct materials quantity variance is

(Multiple Choice)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)