Exam 12: Corporations: Organization, Capital Structure, and Operating Rules

Exam 1: Introduction to Taxation122 Questions

Exam 2: Working With the Tax Law101 Questions

Exam 3: Taxes on the Financial Statements70 Questions

Exam 4: Gross Income100 Questions

Exam 5: Business Deductions143 Questions

Exam 6: Losses and Loss Limitations147 Questions

Exam 7: Property Transactions: Basis, Gain and Loss, and Nontaxable Exchanges126 Questions

Exam 8: Property Transactions: Capital Gains and Losses, Section 1231, and Recapture Provisions119 Questions

Exam 9: Individuals As the Taxpayer132 Questions

Exam 10: Individuals: Income, Deductions, and Credits129 Questions

Exam 11: Individuals As Employees and Proprietors116 Questions

Exam 12: Corporations: Organization, Capital Structure, and Operating Rules136 Questions

Exam 13: Corporations: Earnings and Profits and Distributions127 Questions

Exam 14: Partnerships and Limited Liability Entities142 Questions

Exam 15: S Corporations109 Questions

Exam 16: Multijurisdictional Taxation91 Questions

Exam 17: Business Tax Credits and the Alternative Minimum Tax94 Questions

Exam 18: Comparative Forms of Doing Business84 Questions

Select questions type

The use of § 351 is not limited to the initial formation of a corporation, and it can apply to later transfers as well.

(True/False)

4.9/5  (49)

(49)

In general, the basis of property to a corporation in a transfer that qualifies as a nontaxable exchange under § 351 is the basis in the hands of the transferor shareholder decreased by the amount of any gain recognized on the transfer.

(True/False)

4.9/5 (40)

When Pheasant Corporation was formed under § 351, Kristen transferred property (basis of $26,000 and fair market value of $22,500) for § 1244 stock.Kristen's basis in the Pheasant stock is $26,000.Three years later, Pheasant Corporation goes bankrupt and its stock becomes worthless.Kristen, who is single, owned the stock as an investment.Kristen's loss is:

(Multiple Choice)

4.8/5 (35)

Leah transfers equipment (basis of $400,000 and fair market value of $500,000) for additional stock in Crow Corporation.After the transfer, Leah owns 80% of Crow's stock.Associated with the equipment is § 1245 depreciation recapture potential of $70,000.As a result of the transfer:

(Multiple Choice)

4.9/5 (34)

Earl and Mary form Crow Corporation.Earl transfers property, basis of $200,000 and value of $1,600,000, for 50 shares in Crow Corporation.Mary transfers property, basis of $80,000 and value of $1,480,000, and agrees to serve as manager of Crow for one year; in return Mary receives 50 shares of Crow.The value of Mary's services is $120,000.With respect to the transfers:

(Multiple Choice)

4.7/5 (28)

Eve transfers property (basis of $120,000 and fair market value of $400,000) to Green Corporation for 80% of its stock (worth $350,000) and a long-term note (worth $50,000) executed by Green Corporation and made payable to Eve.As a result of the transfer:

(Multiple Choice)

5.0/5 (39)

A transferor who receives stock for both property and services may not be included in the control group in determining whether an exchange meets the requirements of § 351.

(True/False)

4.8/5 (34)

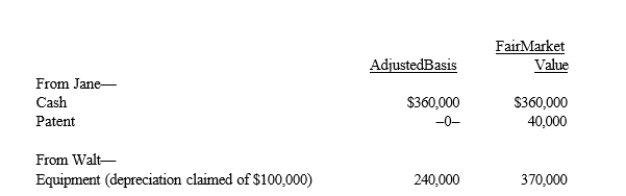

Four individuals form Chickadee Corporation under § 351.Two of these individuals, Jane and Walt, made the following contributions:  Both Jane and Walt receive stock in Chickadee Corporation equal to the value of their investments.

Both Jane and Walt receive stock in Chickadee Corporation equal to the value of their investments.

(Multiple Choice)

4.8/5 (38)

Canary Corporation, a calendar year C corporation, received an $80,000 dividend from Stork Corporation.Canary owns 18% of the Stork Corporation stock.Assuming it is not subject to the taxable income limitation, Canary's dividends received deduction is $40,000.

(True/False)

4.9/5 (43)

When a taxpayer transfers property subject to a mortgage to a controlled corporation in an exchange qualifying under § 351, the transferor shareholder's basis in stock received in the transferee corporation is increased by the amount of the mortgage on the property.

(True/False)

4.9/5 (33)

Donald owns a 45% interest in a partnership that earned $130,000 in the current year.He also owns 45% of the stock in a C corporation that earned $130,000 during the year.Donald received $20,000 in distributions from each of the two entities during the year.With respect to this information, Donald must report $78,500 of income on his individual income tax return for the year.

(True/False)

4.8/5 (36)

Jane and Walt form Yellow Corporation.Jane transfers equipment worth $950,000 (basis of $200,000) and cash of $50,000 to Yellow Corporation for 50% of its stock.Walt transfers a building and land worth $1,050,000 (basis of $400,000) for 50% of Yellow's stock and $50,000 in cash.

(Multiple Choice)

4.8/5 (37)

To ease a liquidity problem, all of the shareholders of Osprey Corporation contribute additional cash to its capital. Osprey has no tax consequences from the contribution.

(True/False)

4.8/5 (38)

Schedule M-1 is used to reconcile net income as computed for financial accounting purposes with taxable income reported on the corporation's income tax return.

(True/False)

4.8/5 (37)

In order to retain the services of Eve, a key employee in Ted's sole proprietorship, Ted contracts with Eve to make her a 30% owner.Ted incorporates the business, receiving in return 100% of the stock.Three days later, Ted transfers 30% of the stock to Eve.Under these circumstances, § 351 will apply to the incorporation of Ted's business.

(True/False)

4.8/5 (39)

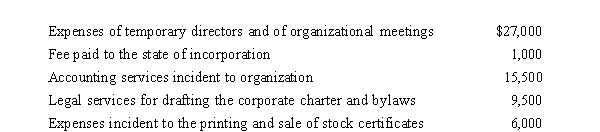

Emerald Corporation, a calendar year C corporation, was formed and began operations on April 1, 2019.The following expenses were incurred during the first tax year (April 1 through December 31, 2019) of operations.  Assuming a § 248 election, what is the Emerald's deduction for organizational expenditures for 2019?

Assuming a § 248 election, what is the Emerald's deduction for organizational expenditures for 2019?

(Multiple Choice)

4.8/5 (31)

When depreciable property is transferred to a controlled corporation under § 351, any recapture potential disappears and does not carry over to the corporation.

(True/False)

4.9/5 (27)

A taxpayer may never recognize a loss on the transfer of property in a transaction subject to § 351.

(True/False)

4.7/5 (32)

In determining whether § 357(c) applies, assess whether the liabilities involved exceed the bases of all assets a shareholder transfers to the corporation.

(True/False)

4.7/5 (45)

Schedule M-1 of Form 1120 is used to reconcile financial net income with taxable income reported on the corporation's income tax return as follows: net income per books + additions - subtractions = taxable income.Which of the following items is an addition on Schedule M-1?

(Multiple Choice)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)