Exam 6: Risk, Return, and the Capital Asset Pricing Model

Exam 1: An Overview of Financial Management and the Financial Environment46 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes74 Questions

Exam 3: Analysis of Financial Statements103 Questions

Exam 4: Time Value of Money159 Questions

Exam 5: Bonds, Bond Valuation, and Interest Rates100 Questions

Exam 6: Risk, Return, and the Capital Asset Pricing Model137 Questions

Exam 7: Stocks, Stock Valuation, and Stock Market Equilibrium66 Questions

Exam 8: Financial Options and Applications in Corporate Finance26 Questions

Exam 9: The Cost of Capital90 Questions

Exam 10: The Basics of Capital Budgeting: Evaluating Cash Flows104 Questions

Exam 11: Cash Flow Estimation and Risk Analysis70 Questions

Exam 12: Financial Planning and Forecasting Financial Statements47 Questions

Exam 13: Corporate Valuation, Value-Based Management and Corporate Governance24 Questions

Exam 14: Distributions to Shareholders: Dividends and Repurchases56 Questions

Exam 15: Capital Structure Decisions70 Questions

Exam 16: Working Capital Management128 Questions

Exam 17: Multinational Financial Management47 Questions

Exam 18: Lease Financing22 Questions

Exam 19: Hybrid Financing: Preferred Stock, Warrants, and Convertibles30 Questions

Exam 20: Initial Public Offerings, Investment Banking, and Financial Restructuring25 Questions

Exam 21: Mergers, Lbos, Divestitures, and Holding Companies48 Questions

Exam 22: Bankruptcy, Reorganization, and Liquidation10 Questions

Exam 23: Derivatives and Risk Management14 Questions

Exam 24: Portfolio Theory, Asset Pricing Models, and Behavioral Finance31 Questions

Exam 25: Real Options19 Questions

Exam 26: Analysis of Capital Structure Theory31 Questions

Exam 27: Providing and Obtaining Credit35 Questions

Exam 28: Advanced Issues in Cash Management and Inventory Control24 Questions

Exam 29: Pension Plan Management10 Questions

Exam 30: Financial Management in Not-For-Profit Businesses10 Questions

Select questions type

A stock's beta measures its diversifiable risk relative to the diversifiable risks of other firms.

(True/False)

4.9/5  (39)

(39)

Diversification will normally reduce the riskiness of a portfolio of stocks.

(True/False)

4.8/5 (33)

Tom O'Brien has a 2-stock portfolio with a total value of $100,000. $37,500 is invested in Stock A with a beta of 0.75 and the remainder is invested in Stock B with a beta of 1.42. What is his portfolio's beta?

(Multiple Choice)

4.7/5 (40)

Generally, the SML is used to find the required return, but on occasion the required return is given and we must solve for one of the other variables. We warn our students before the test that to answer a number of the questions they will have to transform the SML equation to solve for beta, the market risk premium, the risk-free rate, or the market return.

-Maxwell Inc.'s stock has a 50% chance of producing a 25% return, a 30% chance of producing a 10% return, and a 20% chance of producing a -28% return. What is the firm's expected rate of return?

(Multiple Choice)

4.8/5 (33)

For a portfolio of 40 randomly selected stocks, which of the following is most likely to be true?

(Multiple Choice)

4.7/5 (32)

Someone who is risk averse has a general dislike for risk and a preference for certainty. If risk aversion exists in the market, then investors in general are willing to accept somewhat lower returns on less risky securities. Different investors have different degrees of risk aversion, and the end result is that investors with greater risk aversion tend to hold securities with lower risk (and therefore a lower expected return) than investors who have more tolerance for risk.

(True/False)

4.8/5 (35)

Which is the best measure of risk for a single asset held in isolation, and which is the best measure for an asset held in a diversified portfolio?

(Multiple Choice)

4.8/5 (35)

Stocks A and B each have an expected return of 12%, a beta of 1.2, and a standard deviation of 25%. The returns on the two stocks have a correlation of 0.6. Portfolio P has 50% in Stock A and 50% in Stock B. Which of the following statements is CORRECT?

(Multiple Choice)

4.9/5 (29)

It is possible for a firm to have a positive beta, even if the correlation between its returns and those of another firm is negative.

(True/False)

4.7/5 (37)

Which of the following is NOT a potential problem when estimating and using betas, i.e., which statement is FALSE?

(Multiple Choice)

4.7/5 (46)

If investors are risk averse and hold only one stock, we can conclude that the required rate of return on a stock whose standard deviation is

0.21 will be greater than the required return on a stock whose standard deviation is 0.10. However, if stocks are held in portfolios, it is possible that the required return could be higher on the stock with the low standard deviation.

(True/False)

4.9/5 (33)

Suppose you hold a portfolio consisting of a $10,000 investment in each of 8 different common stocks. The portfolio's beta is 1.25. Now suppose you decided to sell one of your stocks that has a beta of 1.00 and to use the proceeds to buy a replacement stock with a beta of 1.35. What would the portfolio's new beta be?

(Multiple Choice)

4.8/5 (37)

Mike Flannery holds the following portfolio:

the portfolio's beta?

the portfolio's beta?

(Multiple Choice)

4.7/5 (35)

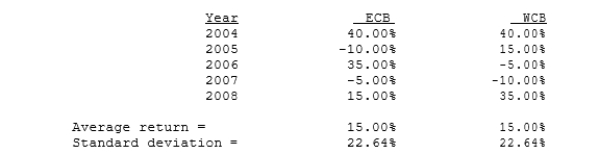

Assume that your uncle holds just one stock, East Coast Bank (ECB), which he thinks has very little risk. You agree that the stock is relatively safe, but you want to demonstrate that his risk would be even lower if he were more diversified. You obtain the following returns data for West Coast Bank (WCB). Both banks have had less variability than most other stocks over the past 5 years. Measured by the standard deviation of returns, by how much would your uncle's risk have been reduced if he had held a portfolio consisting of 60% in ECB and the remainder in WCB? (Hint: Use the sample standard deviation formula.)

(Multiple Choice)

5.0/5 (39)

A stock's beta is more relevant as a measure of risk to an investor who holds only one stock than to an investor who holds a well-diversified portfolio.

(True/False)

4.8/5 (31)

Moerdyk Company's stock has a beta of 1.40, the risk-free rate is 4.25%, and the market risk premium is 5.50%. What is the firm's required rate of return?

(Multiple Choice)

4.8/5 (37)

Which of the following statements is CORRECT? (Assume that the risk- free rate is a constant.)

(Multiple Choice)

4.7/5 (41)

Calculate the required rate of return for Climax Inc., assuming that (1) investors expect a 4.0% rate of inflation in the future, (2) the real risk-free rate is 3.0%, (3) the market risk premium is 5.0%, (4) the firm has a beta of 1.00, and (5) its realized rate of return has averaged 15.0% over the last 5 years.

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)