Exam 6: Risk, Return, and the Capital Asset Pricing Model

Exam 1: An Overview of Financial Management and the Financial Environment46 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes74 Questions

Exam 3: Analysis of Financial Statements103 Questions

Exam 4: Time Value of Money159 Questions

Exam 5: Bonds, Bond Valuation, and Interest Rates100 Questions

Exam 6: Risk, Return, and the Capital Asset Pricing Model137 Questions

Exam 7: Stocks, Stock Valuation, and Stock Market Equilibrium66 Questions

Exam 8: Financial Options and Applications in Corporate Finance26 Questions

Exam 9: The Cost of Capital90 Questions

Exam 10: The Basics of Capital Budgeting: Evaluating Cash Flows104 Questions

Exam 11: Cash Flow Estimation and Risk Analysis70 Questions

Exam 12: Financial Planning and Forecasting Financial Statements47 Questions

Exam 13: Corporate Valuation, Value-Based Management and Corporate Governance24 Questions

Exam 14: Distributions to Shareholders: Dividends and Repurchases56 Questions

Exam 15: Capital Structure Decisions70 Questions

Exam 16: Working Capital Management128 Questions

Exam 17: Multinational Financial Management47 Questions

Exam 18: Lease Financing22 Questions

Exam 19: Hybrid Financing: Preferred Stock, Warrants, and Convertibles30 Questions

Exam 20: Initial Public Offerings, Investment Banking, and Financial Restructuring25 Questions

Exam 21: Mergers, Lbos, Divestitures, and Holding Companies48 Questions

Exam 22: Bankruptcy, Reorganization, and Liquidation10 Questions

Exam 23: Derivatives and Risk Management14 Questions

Exam 24: Portfolio Theory, Asset Pricing Models, and Behavioral Finance31 Questions

Exam 25: Real Options19 Questions

Exam 26: Analysis of Capital Structure Theory31 Questions

Exam 27: Providing and Obtaining Credit35 Questions

Exam 28: Advanced Issues in Cash Management and Inventory Control24 Questions

Exam 29: Pension Plan Management10 Questions

Exam 30: Financial Management in Not-For-Profit Businesses10 Questions

Select questions type

Stock X has a beta of 0.5 and Stock Y has a beta of 1.5. Which of the following statements must be true, according to the CAPM?

(Multiple Choice)

4.7/5  (38)

(38)

Returns for the Dayton Company over the last 3 years are shown below. What's the standard deviation of the firm's returns? (Hint: This is a sample, not a complete population, so the sample standard deviation formula should be used.)

(Multiple Choice)

4.8/5 (39)

Stock A has an expected return of 12%, a beta of 1.2, and a standard deviation of 20%. Stock B also has a beta of 1.2, but its expected return is 10% and its standard deviation is 15%. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero (that is, rA,B = 0). Which of the following statements is CORRECT?

(Multiple Choice)

4.7/5 (35)

The risk-free rate is 6%; Stock A has a beta of 1.0; Stock B has a beta of 2.0; and the market risk premium, rM − rRF, is positive. Which of the following statements is CORRECT?

(Multiple Choice)

4.9/5 (33)

Stock A has a beta of 0.8 and Stock B has a beta of 1.2. 50% of Portfolio P is invested in Stock A and 50% is invested in Stock B. If the market risk premium (rM − rRF) were to increase but the risk-free rate (rRF) remained constant, which of the following would occur?

(Multiple Choice)

4.7/5 (40)

Stock HB has a beta of 1.5 and Stock LB has a beta of 0.5. The market is in equilibrium, with required returns equaling expected returns. Which of the following statements is CORRECT?

(Multiple Choice)

5.0/5 (43)

Stock A has an expected return of 10% and a standard deviation of 20%. Stock B has an expected return of 13% and a standard deviation of 30%. The risk-free rate is 5% and the market risk premium, rM − rRF, is 6%. Assume that the market is in equilibrium. Portfolio AB has 50% invested in Stock A and 50% invested in Stock B. The returns of Stock A and Stock B are independent of one another, i.e., the correlation coefficient between them is zero. Which of the following statements is CORRECT?

(Multiple Choice)

4.7/5 (33)

Stock A has a beta = 0.8, while Stock B has a beta = 1.6. Which of the following statements is CORRECT?

(Multiple Choice)

4.8/5 (42)

CCC Corp has a beta of 1.5 and is currently in equilibrium. The required rate of return on the stock is 12.00% versus a required return on an average stock of 10.00%. Now the required return on an average stock increases by 30.0% (not percentage points). Neither betas nor the risk-free rate change. What would CCC's new required return be?

(Multiple Choice)

4.9/5 (33)

The Y-axis intercept of the SML represents the required return of a portfolio with a beta of zero, which is the risk-free rate.

(True/False)

4.9/5 (47)

Stock A's beta is 1.5 and Stock B's beta is 0.5. Which of the following statements must be true about these securities? (Assume market equilibrium.)

(Multiple Choice)

4.8/5 (32)

Portfolio A has but one stock, while Portfolio B consists of all stocks that trade in the market, each held in proportion to its market value. Because of its diversification, Portfolio B will by definition be riskless.

(True/False)

4.9/5 (34)

The SML relates required returns to firms' systematic (or market) risk. The slope and intercept of this line can be influenced by a manager's actions.

(True/False)

4.9/5 (44)

Inflation, recession, and high interest rates are economic events that are best characterized as being

(Multiple Choice)

4.9/5 (38)

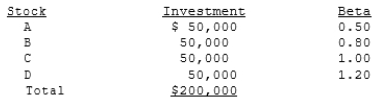

Kristina Raattama holds a $200,000 portfolio consisting of the following stocks. The portfolio's beta is 0.875.

If Kristina replaces Stock A with another stock, , which has a beta of 1. 50 , what will the portfolio'g new beta be?

If Kristina replaces Stock A with another stock, , which has a beta of 1. 50 , what will the portfolio'g new beta be?

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)