Exam 6: Risk, Return, and the Capital Asset Pricing Model

Exam 1: An Overview of Financial Management and the Financial Environment46 Questions

Exam 2: Financial Statements, Cash Flow, and Taxes74 Questions

Exam 3: Analysis of Financial Statements103 Questions

Exam 4: Time Value of Money159 Questions

Exam 5: Bonds, Bond Valuation, and Interest Rates100 Questions

Exam 6: Risk, Return, and the Capital Asset Pricing Model137 Questions

Exam 7: Stocks, Stock Valuation, and Stock Market Equilibrium66 Questions

Exam 8: Financial Options and Applications in Corporate Finance26 Questions

Exam 9: The Cost of Capital90 Questions

Exam 10: The Basics of Capital Budgeting: Evaluating Cash Flows104 Questions

Exam 11: Cash Flow Estimation and Risk Analysis70 Questions

Exam 12: Financial Planning and Forecasting Financial Statements47 Questions

Exam 13: Corporate Valuation, Value-Based Management and Corporate Governance24 Questions

Exam 14: Distributions to Shareholders: Dividends and Repurchases56 Questions

Exam 15: Capital Structure Decisions70 Questions

Exam 16: Working Capital Management128 Questions

Exam 17: Multinational Financial Management47 Questions

Exam 18: Lease Financing22 Questions

Exam 19: Hybrid Financing: Preferred Stock, Warrants, and Convertibles30 Questions

Exam 20: Initial Public Offerings, Investment Banking, and Financial Restructuring25 Questions

Exam 21: Mergers, Lbos, Divestitures, and Holding Companies48 Questions

Exam 22: Bankruptcy, Reorganization, and Liquidation10 Questions

Exam 23: Derivatives and Risk Management14 Questions

Exam 24: Portfolio Theory, Asset Pricing Models, and Behavioral Finance31 Questions

Exam 25: Real Options19 Questions

Exam 26: Analysis of Capital Structure Theory31 Questions

Exam 27: Providing and Obtaining Credit35 Questions

Exam 28: Advanced Issues in Cash Management and Inventory Control24 Questions

Exam 29: Pension Plan Management10 Questions

Exam 30: Financial Management in Not-For-Profit Businesses10 Questions

Select questions type

One key conclusion of the Capital Asset Pricing Model is that the value of an asset should be measured by considering both the risk and the expected return of the asset, assuming that the asset is held in a

well-diversified portfolio. The risk of the asset held in isolation is not relevant under the CAPM.

(True/False)

4.8/5  (41)

(41)

The Y-axis intercept of the SML indicates the required return on an individual asset whenever the realized return on an average (b = 1) stock is zero.

(True/False)

4.8/5 (38)

The realized return on a stock portfolio is the weighted average of the expected returns on the stocks in the portfolio.

(True/False)

4.8/5 (35)

Stock A has a beta of 0.7, whereas Stock B has a beta of 1.3. Portfolio P has 50% invested in both A and B. Which of the following would occur if the market risk premium increased by 1% but the risk- free rate remained constant?

(Multiple Choice)

4.8/5 (42)

Stock X has a beta of 0.6, while Stock Y has a beta of 1.4. Which of the following statements is CORRECT?

(Multiple Choice)

4.8/5 (36)

A mutual fund manager has a $40 million portfolio with a beta of 1.00. The risk-free rate is 4.25%, and the market risk premium is 6.00%. The manager expects to receive an additional $60 million which she plans to invest in additional stocks. After investing the additional funds, she wants the fund's required and expected return to be 13.00%. What must the average beta of the new stocks be to achieve the target required rate of return?

(Multiple Choice)

4.7/5 (39)

Stocks A and B each have an expected return of 15%, a standard deviation of 20%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of +0.6. You have a portfolio that consists of 50% A and 50% B. Which of the following statements is CORRECT?

(Multiple Choice)

4.8/5 (38)

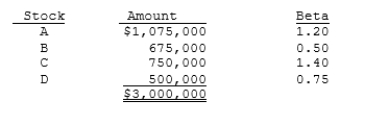

Assume that you are the portfolio manager of the SF Fund, a $3 million hedge fund that contains the following stocks. The required rate of return on the market is 11.00% and the risk-free rate is 5.00%. What rate of return should investors expect (and require) on this fund?

(Multiple Choice)

4.8/5 (40)

Under the CAPM, the required rate of return on a firm's common stock is determined only by the firm's market risk. If its market risk is known, and if that risk is expected to remain constant, then analysts have all the information they need to calculate the firm's required rate of return.

(True/False)

4.8/5 (31)

Over the past 75 years, we have observed that investments with the highest average annual returns also tend to have the highest standard deviations of annual returns. This observation supports the notion that there is a positive correlation between risk and return. Which of the following answers correctly ranks investments from highest to lowest risk (and return), where the security with the highest risk is shown first, the one with the lowest risk last?

(Multiple Choice)

4.7/5 (32)

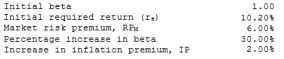

Data for Dana Industries is shown below. Now Dana assets that cause its beta to increase by 30%. In inflation increases by 2.00%. What is the stock's return?

(Multiple Choice)

4.8/5 (36)

Stock A's beta is 1.5 and Stock B's beta is 0.5. Which of the following statements must be true, assuming the CAPM is correct.

(Multiple Choice)

4.9/5 (40)

The coefficient of variation, calculated as the standard deviation of expected returns divided by the expected return, is a standardized measure of the risk per unit of expected return.

(True/False)

4.9/5 (39)

The CAPM is a multi-period model that takes account of differences in securities' maturities, and it can be used to determine the required rate of return for any given level of systematic risk.

(True/False)

4.9/5 (38)

An individual stock's diversifiable risk, which is measured by its beta, can be lowered by adding more stocks to the portfolio in which the stock is held.

(True/False)

4.8/5 (43)

Which of the following is most likely to occur as you add randomly selected stocks to your portfolio, which currently consists of 3 average stocks?

(Multiple Choice)

4.8/5 (39)

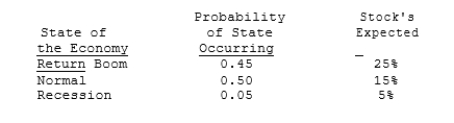

Choudhary Corp believes the following probability distribution exists for its stock. What is the coefficient of variation on the company's stock?

(Multiple Choice)

4.8/5 (36)

Assume that the risk-free rate, rRF, increases but the market risk premium, (rM − rRF), declines with the net effect being that the overall required return on the market, rM, remains constant. Which of the following statements is CORRECT?

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)