Exam 3: Consolidationssubsequent to the Date of Acquisition

Exam 1: The Equity Method of Accounting for Investments123 Questions

Exam 2: Consolidation of Financial Information120 Questions

Exam 3: Consolidationssubsequent to the Date of Acquisition123 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership120 Questions

Exam 5: Consolidated Financial Statements Intra-Entity Asset Transactions126 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues119 Questions

Exam 7: Foreign Currency Transactions and Hedging Foreign Exchange Risk107 Questions

Exam 8: Translation of Foreign Currency Financial Statements101 Questions

Exam 9: Partnerships: Formation and Operation91 Questions

Exam 10: Partnerships: Termination and Liquidation71 Questions

Exam 11: Accounting for State and Local Governments Part 187 Questions

Exam 12: Accounting for State and Local Governments Part 250 Questions

Select questions type

Beatty, Inc. acquires 100% of the voting stock of Gataux Company on January 1, 2020 for $80,000, consisting of $20,000 in cash and 6,000 shares of stock. A contingent payment of $12,000 in cash will be paid on April 1, 2021 if Gataux generates cash flows from operations of $26,500 or more in the next year. Beatty estimates that there is a 30% probability that Gataux will generate at least $26,500 next year, and uses an interest rate of 4% to incorporate the time value of money. The fair value of $12,000 at 4%, using a probability-weighted approach, is $3,461. A contingent payment of $20,000, payable in stock, will be paid to the former owners of Gataux on April 1, 2021 if the market value of Beatty stock drops below $10 per share. Beatty estimates there is a 15% probability that its share price will not exceed that threshold. Using the same interest rate and probability-weighted approach, Beatty calculates the market value of the stock contingency to be $2,884.On April 1, 2021, Beatty stock closes with a market value of $8.98 per share. How many shares of stock, rounded to the next whole number, must it issue to the former owners of Gataux?

(Multiple Choice)

4.8/5  (39)

(39)

When consolidating parent and subsidiary financial statements, which of the following statements is true?

(Multiple Choice)

4.7/5 (42)

Reeder Corp. acquired one hundred percent of O'Neill Inc. on January 1, 2019, at a price in excess of the subsidiary's fair value. On that date, Reeder's equipment (ten-year life)had a book value of $380,000 but a fair value of $460,000. O'Neill had equipment (ten-year life)with a book value of $240,000 and a fair value of $370,000. Reeder used the partial equity method to record its investment in O'Neill. On December 31, 2021, Reeder had equipment with a book value of $270,000 and a fair value of $400,000. O'Neill had equipment with a book value of $180,000 and a fair value of $300,000. What is the consolidated balance for the Equipment account as of December 31, 2021?

(Multiple Choice)

4.8/5 (44)

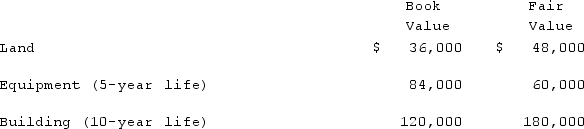

Utah Inc. acquired all of the outstanding common stock of Trimmer Corp. on January 1, 2019. At that date, Trimmer owned only three assets and had no liabilities:

If Utah paid $300,000 in cash for Trimmer, what allocation and amortization should have been assigned to the subsidiary's Building account and its Equipment account in a December 31, 2021 consolidation?

If Utah paid $300,000 in cash for Trimmer, what allocation and amortization should have been assigned to the subsidiary's Building account and its Equipment account in a December 31, 2021 consolidation?

(Essay)

4.8/5 (33)

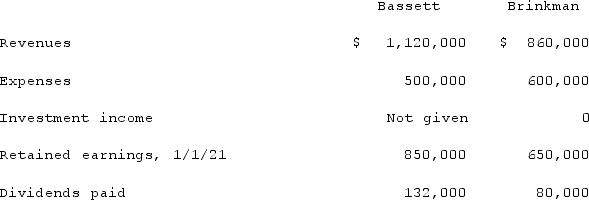

Bassett Inc. acquired all of the outstanding common stock of Brinkman Corp. on January 1, 2019, for $422,000. Equipment with a ten-year life was undervalued on Brinkman's financial records by $48,000. Brinkman also owned an unrecorded customer list with an assessed fair value of $71,000 and an estimated remaining life of five years.Brinkman earned reported net income of $185,000 in 2019 and $226,000 in 2020. Dividends of $75,000 were paid in each of these two years. Selected account balances as of December 31, 2021, for the two companies follow.  If the partial equity method had been applied, what was 2021 consolidated net income?

If the partial equity method had been applied, what was 2021 consolidated net income?

(Multiple Choice)

4.8/5 (35)

How is the fair value allocation of an intangible asset allocated to expense when the asset has no legal, regulatory, contractual, competitive, economic, or other factors that limit its life?

(Multiple Choice)

4.8/5 (40)

Fesler Inc. acquired all of the outstanding common stock of Pickett Company on January 1, 2020. Annual amortization of $22,000 resulted from this transaction. On the date of the acquisition, Fesler reported retained earnings of $520,000 while Pickett reported a $240,000 balance for retained earnings. Fesler reported net income of $100,000 in 2020 and $68,000 in 2021, and paid dividends of $25,000 in dividends each year. Pickett reported net income of $24,000 in 2020 and $36,000 in 2021, and paid dividends of $10,000 in dividends each year.If the parent's net income reflected use of the initial value method, what were the consolidated retained earnings on December 31, 2021?

(Essay)

4.8/5 (40)

When a company applies the initial value method in accounting for its investment in a subsidiary, and the subsidiary reports income in excess of dividends paid, what entry would be made to convert to full-accrual totals in a consolidation worksheet for the second year?

(Multiple Choice)

4.9/5 (30)

All of the following are acceptable methods to account for a majority-owned investment in subsidiary except

(Multiple Choice)

4.8/5 (42)

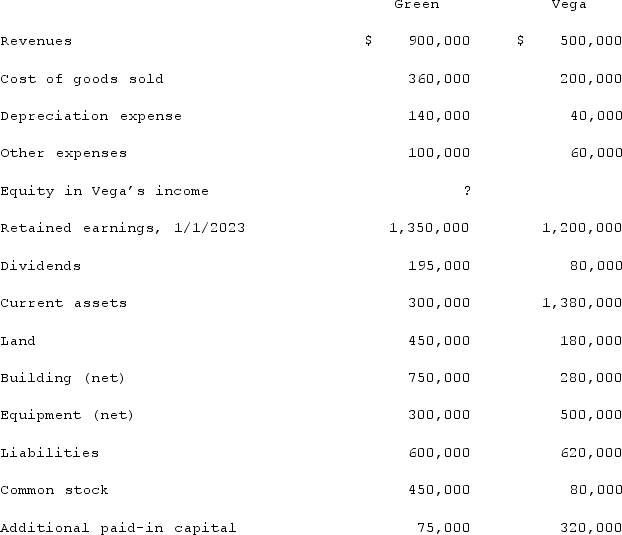

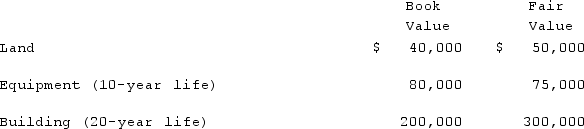

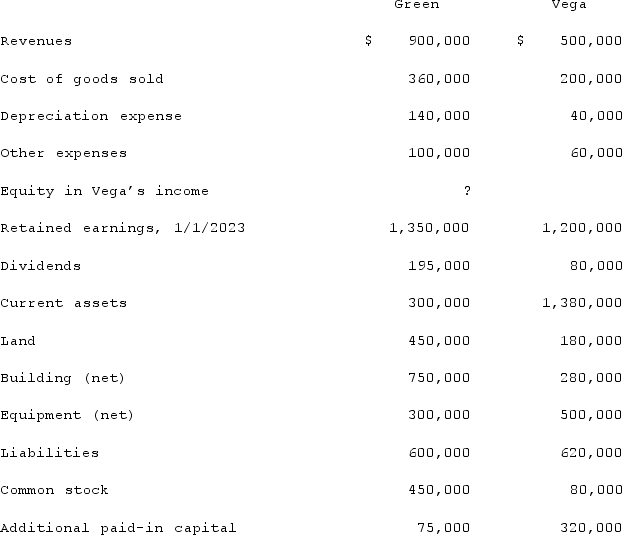

Following are selected accounts for Green Corporation and Vega Company as of December 31, 2023. Several of Green's accounts have been omitted.  Green acquired 100% of Vega on January 1, 2019, by issuing 10,500 shares of its $10 par value common stock with a fair value of $95 per share. On January 1, 2019, Vega's land was undervalued by $40,000, its buildings were overvalued by $30,000, and equipment was undervalued by $80,000. The buildings have a 20-year life and the equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a 16-year remaining life. There was no goodwill associated with this investment.Compute the book value of Vega at January 1, 2019.

Green acquired 100% of Vega on January 1, 2019, by issuing 10,500 shares of its $10 par value common stock with a fair value of $95 per share. On January 1, 2019, Vega's land was undervalued by $40,000, its buildings were overvalued by $30,000, and equipment was undervalued by $80,000. The buildings have a 20-year life and the equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a 16-year remaining life. There was no goodwill associated with this investment.Compute the book value of Vega at January 1, 2019.

(Multiple Choice)

4.8/5 (33)

What is the partial equity method? How does it differ from the equity method? What are its advantages and disadvantages compared to the equity method?

(Essay)

4.8/5 (40)

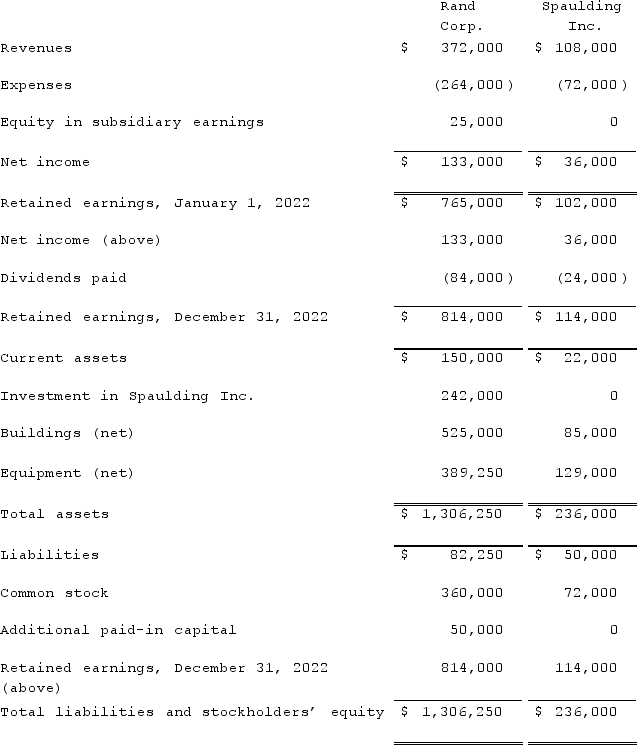

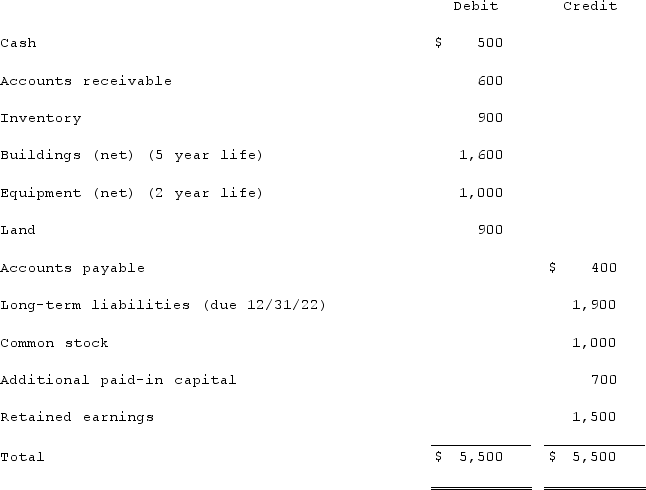

On January 1, 2019, Rand Corp. issued shares of its common stock to acquire all of the outstanding common stock of Spaulding Inc. Spaulding's book value was only $140,000 at the time, but Rand issued 12,000 shares having a par value of $1 per share and a fair value of $20 per share. Rand was willing to convey these shares because it felt that buildings (ten-year life)were undervalued on Spaulding's records by $60,000 while equipment (five-year life)was undervalued by $25,000. Any consideration transferred over fair value of identified net assets acquired is assigned to goodwill.Following are the individual financial records for these two companies for the year ended December 31, 2022.

Required:Prepare a consolidation worksheet for this business combination.

Required:Prepare a consolidation worksheet for this business combination.

(Essay)

4.9/5 (38)

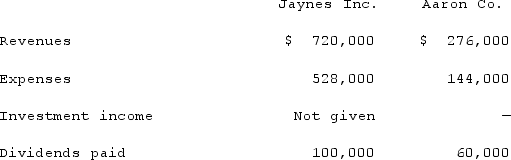

Jaynes Inc. acquired all of Aaron Co.'s common stock on January 1, 2020, by issuing 11,000 shares of $1 par value common stock. Jaynes' shares had a $17 per share fair value. On that date, Aaron reported a net book value of $120,000. However, its equipment (with a five-year remaining life)was undervalued by $6,000 in the company's accounting records. Any excess of consideration transferred over fair value of assets and liabilities acquired is assigned to an unrecorded patent to be amortized over ten years.The following figures came from the individual accounting records of these two companies as of December 31, 2020:

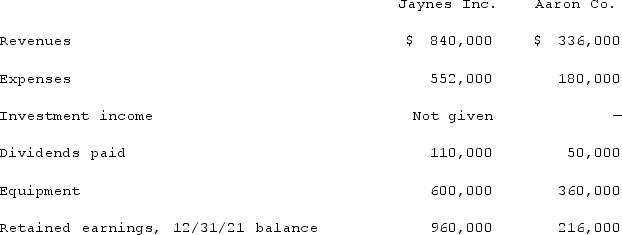

The following figures came from the individual accounting records of these two companies as of December 31, 2021:

The following figures came from the individual accounting records of these two companies as of December 31, 2021:

What balance would Jaynes' Investment in Aaron Co. account have shown on December 31, 2021, when the equity method was applied for this acquisition?

What balance would Jaynes' Investment in Aaron Co. account have shown on December 31, 2021, when the equity method was applied for this acquisition?

(Essay)

4.7/5 (39)

Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on January 1, 2020. At that date, Glen owns only three assets and has no liabilities:  If Watkins pays $450,000 in cash for Glen, what acquisition-date fair value allocation, net of amortization, should be attributed to the subsidiary's Equipment in consolidation at December 31, 2022?

If Watkins pays $450,000 in cash for Glen, what acquisition-date fair value allocation, net of amortization, should be attributed to the subsidiary's Equipment in consolidation at December 31, 2022?

(Multiple Choice)

4.8/5 (38)

Hanson Co. acquired all of the common stock of Roberts Inc. on January 1, 2020, transferring consideration in an amount slightly more than the fair value of Roberts' net assets. At that time, Roberts had buildings with a twenty-year useful life, a book value of $600,000, and a fair value of $696,000. On December 31, 2021, Roberts had buildings with a book value of $570,000 and a fair value of $648,000. On that date, Hanson had buildings with a book value of $1,878,000 and a fair value of $2,160,000.Required:What amount should be shown for buildings on the consolidated balance sheet dated December 31, 2021?

(Essay)

4.8/5 (34)

Following are selected accounts for Green Corporation and Vega Company as of December 31, 2023. Several of Green's accounts have been omitted.  Green acquired 100% of Vega on January 1, 2019, by issuing 10,500 shares of its $10 par value common stock with a fair value of $95 per share. On January 1, 2019, Vega's land was undervalued by $40,000, its buildings were overvalued by $30,000, and equipment was undervalued by $80,000. The buildings have a 20-year life and the equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a 16-year remaining life. There was no goodwill associated with this investment.Compute the December 31, 2023, consolidated buildings.

Green acquired 100% of Vega on January 1, 2019, by issuing 10,500 shares of its $10 par value common stock with a fair value of $95 per share. On January 1, 2019, Vega's land was undervalued by $40,000, its buildings were overvalued by $30,000, and equipment was undervalued by $80,000. The buildings have a 20-year life and the equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a 16-year remaining life. There was no goodwill associated with this investment.Compute the December 31, 2023, consolidated buildings.

(Multiple Choice)

4.7/5 (30)

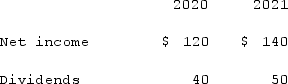

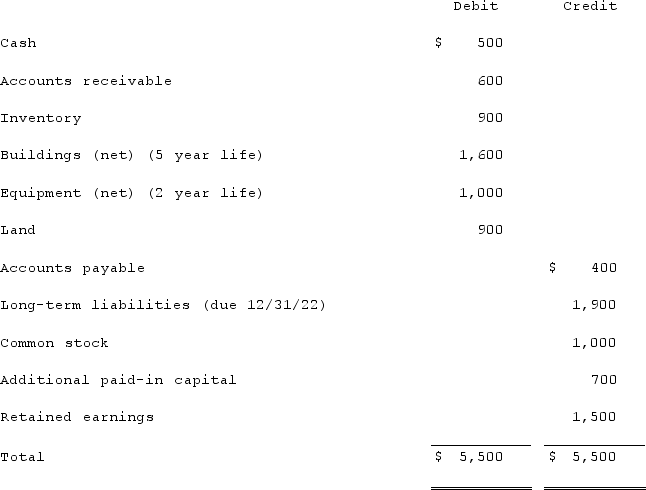

Jackson Company acquires 100% of the stock of Clark Corporation on January 1, 2020, for $4,100 cash. As of that date Clark has the following trial balance:  Net income and dividends reported by Clark for 2020 and 2021 follow:

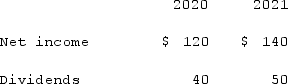

Net income and dividends reported by Clark for 2020 and 2021 follow:

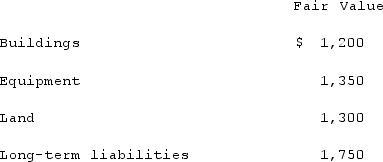

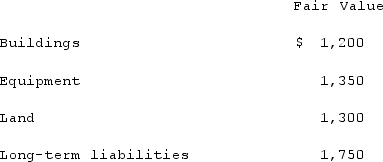

The fair value of Clark's net assets that differ from their book values are listed below:

The fair value of Clark's net assets that differ from their book values are listed below:

Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life.Compute the consideration transferred in excess of book value acquired at January 1, 2020.

Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life.Compute the consideration transferred in excess of book value acquired at January 1, 2020.

(Multiple Choice)

4.9/5 (41)

Jackson Company acquires 100% of the stock of Clark Corporation on January 1, 2020, for $4,100 cash. As of that date Clark has the following trial balance:  Net income and dividends reported by Clark for 2020 and 2021 follow:

Net income and dividends reported by Clark for 2020 and 2021 follow:

The fair value of Clark's net assets that differ from their book values are listed below:

The fair value of Clark's net assets that differ from their book values are listed below:

Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life.Compute the amount of Clark's equipment that would be reported in a December 31, 2021, consolidated balance sheet.

Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life.Compute the amount of Clark's equipment that would be reported in a December 31, 2021, consolidated balance sheet.

(Multiple Choice)

4.9/5 (35)

Anderson, Inc. acquires all of the voting stock of Kenneth, Inc. on January 4, 2020, at an amount in excess of Kenneth's fair value. On that date, Kenneth has equipment with a book value of $90,000 and a fair value of $120,000 (10-year remaining life). Anderson has equipment with a book value of $800,000 and a fair value of $1,200,000 (10-year remaining life). On December 31, 2021, Anderson has equipment with a book value of $975,000 but a fair value of $1,350,000 and Kenneth has equipment with a book value of $105,000 but a fair value of $125,000.If Anderson applies the equity method in accounting for Kenneth, what is the consolidated balance for the Equipment account as of December 31, 2021?

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)