Exam 20: Forming and Operating Partnerships

Exam 1: An Introduction to Tax134 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities109 Questions

Exam 3: Tax Planning Strategies and Related Limitations137 Questions

Exam 4: Individual Income Tax Overview, Dependents, and Filing Status130 Questions

Exam 5: Gross Income and Exclusions152 Questions

Exam 6: Individual Deductions117 Questions

Exam 7: Investments93 Questions

Exam 8: Individual Income Tax Computation and Tax Credits179 Questions

Exam 9: Business Income, Deductions, and Accounting Methods129 Questions

Exam 10: Property Acquisition and Cost Recovery131 Questions

Exam 11: Property Dispositions132 Questions

Exam 12: Compensation122 Questions

Exam 13: Retirement Savings and Deferred Compensation157 Questions

Exam 14: Tax Consequences of Home Ownership126 Questions

Exam 15: Entities Overview87 Questions

Exam 16: Corporate Operations126 Questions

Exam 17: Accounting for Income Taxes125 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions122 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation121 Questions

Exam 20: Forming and Operating Partnerships131 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions118 Questions

Exam 22: S Corporations157 Questions

Exam 23: State and Local Taxes139 Questions

Exam 24: The Us Taxation of Multinational Transactions105 Questions

Exam 25: Transfer Taxes and Wealth Planning145 Questions

Select questions type

John, a limited partner of Candy Apple, LP, is allocated $30,000 of ordinary business loss from the partnership. Before the loss allocation, his tax basis is $20,000 and his at-risk amount is $10,000. John also has ordinary business income of $20,000 from Sweet Pea, LP, as a general partner and ordinary business income of $5,000 from Red Tomato as a limited partner. How much of the $30,000 loss from Candy Apple can John deduct currently?

(Multiple Choice)

4.8/5  (44)

(44)

Peter, Matt, Priscilla, and Mary began the year in the PMPM General Partnership sharing profits, losses, and capital equally. They had a tax basis at the beginning of the year of $3,000, $10,000, $8,000, and $11,000, respectively. Early in the year, Mary provided general consulting services to the partnership and received an additional 15 percent profits, losses, and capital interest in the partnership. The liquidation value of her additional interest was $45,000. Later the same year, the partnership received cash contributions of $25,000 from Peter and Matt that it used to repay the partnership's $35,000 recourse debt. According to state law, the partners shared responsibility for this debt in accordance with their loss-sharing ratios. What is each partner's tax basis after adjustment for these transactions?

(Essay)

4.8/5 (35)

Jerry, a partner with 30percent capital and profits interest, received his Schedule K-1 from Plush Pillows, LP. At the beginning of the year, Jerry's tax basis in his partnership interest was $50,000. His current-year Schedule K-1 reported an ordinary loss of $15,000, long-term capital gain of $3,000, qualified dividends of $2,000, $500 of non-deductible expenses, a $10,000 cash contribution, and a reduction of $4,000 in his share of partnership debt. What is Jerry's adjusted basis in his partnership interest at the end of the year?

(Multiple Choice)

4.9/5 (34)

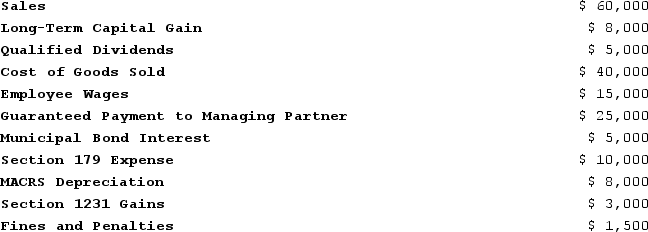

Illuminating Light Partnership had the following revenues, expenses, gains, losses, and distributions:

Given these items, what is Illuminating Light's ordinary business income (loss)for the year?

Given these items, what is Illuminating Light's ordinary business income (loss)for the year?

(Essay)

4.9/5 (34)

A partner's self-employment earnings (loss)may be affected by her share of ordinary business income (loss)and any guaranteed payments she receives. The impact of these amounts typically depends on the status of the partner. Which of the following statements correctly describes the effect these items have on the partner's self-employment earnings (loss)?

(Multiple Choice)

4.7/5 (45)

Which of the following items will affect a partner's tax basis?

(Multiple Choice)

5.0/5 (35)

What general accounting methods may be used by a partnership, and how and by whom are they selected?

(Essay)

4.8/5 (43)

Partnerships can use special allocations to shift built-in gains and built-in losses on contributed property from a partner who contributed the property to other partners.

(True/False)

4.8/5 (42)

What is the correct order for applying the following three items to adjust a partner's tax basis in his partnership interest: (1)Increase for share of ordinary business income, (2)Decrease for share of separately stated loss items, and (3)Decrease for distributions?

(Multiple Choice)

4.9/5 (41)

A partnership may use the cash method despite having a corporate partner when the partnership's average gross receipts for the prior three taxable years don't exceed _____.

(Multiple Choice)

4.9/5 (34)

A purchased partnership interest has a holding period beginning on the date of purchase regardless of the type of property held by the partnership.

(True/False)

4.7/5 (37)

Which of the following would not be classified as a material participant in an activity?

(Multiple Choice)

4.8/5 (38)

An additional allocation of partnership debt or relief of partnership debt is considered to be a deemed cash contribution or cash distribution, respectively.

(True/False)

4.9/5 (32)

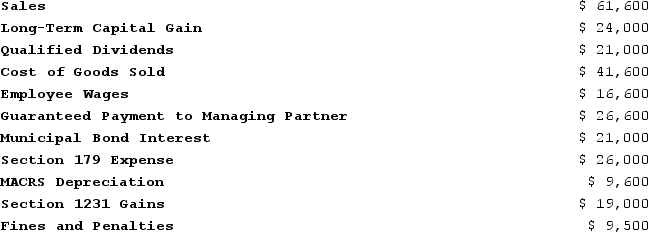

Illuminating Light Partnership had the following revenues, expenses, gains, losses, and distributions:

Given these items, what is Illuminating Light's ordinary business income (loss)for the year?

Given these items, what is Illuminating Light's ordinary business income (loss)for the year?

(Essay)

4.9/5 (35)

What is the difference between a partner's tax basis and at-risk amount?

(Essay)

4.7/5 (41)

The character of each separately stated item is determined at the partner level.

(True/False)

4.9/5 (38)

How does additional debt or relief of debt affect a partner's basis?

(Multiple Choice)

4.7/5 (39)

What type of debt is not included in calculating a partner's at-risk amount?

(Multiple Choice)

4.8/5 (33)

Fred has a 45 percent profits interest and 30percent capital interest in the SAP Partnership, and his tax basis before considering his share of SAP's current-year loss is $13,000. Included in his tax basis is a $4,600 share of recourse debt and a $7,300 share of nonrecourse debt. Fred is a limited partner in SAP. He is not involved in any other activities. If SAP has a $17,000 ordinary loss for the year, how much of the loss can be deducted currently, and how much of the loss is suspended because of the tax basis, at-risk, and passive activity loss limitations?

(Essay)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)