Exam 9: Forming and Operating Partnerships

Exam 1: Business Income, Deductions, and Accounting Methods129 Questions

Exam 2: Property Acquisition and Cost Recovery131 Questions

Exam 3: Property Dispositions132 Questions

Exam 4: Business Entities Overview87 Questions

Exam 5: Corporate Operations126 Questions

Exam 6: Accounting for Income Taxes125 Questions

Exam 7: Corporate Taxation: Non-Liquidating Distributions122 Questions

Exam 8: Corporate Formation, Reorganization, and Liquidation121 Questions

Exam 9: Forming and Operating Partnerships131 Questions

Exam 10: Dispositions of Partnership Interests and Partnership Distributions118 Questions

Exam 11: S Corporations157 Questions

Exam 12: State and Local Taxes139 Questions

Exam 13: The Us Taxation of Multinational Transactions105 Questions

Exam 14: Transfer Taxes and Wealth Planning145 Questions

Select questions type

Styling Shoes, LLC, filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax bases at the beginning of 20X8: (1) Jane, a member with a 25 percent profits and capital interest and a $8,500 outside basis, (2) Joe, a member with a 45 percent profits and capital interest and a $13,500 outside basis, and (3) Jack, a member with a 30 percent profits and capital interest and a $5,500 outside basis. The following items were reported on Styling's Schedule K for the year: ordinary income of $107,000, Section 1231 gain of $18,500, charitable contributions of $28,500, and tax-exempt income of $6,500. In addition, Styling received an additional bank loan of $15,500 during 20X8. What is Jane's tax basis after adjustment for her share of these items?

(Multiple Choice)

4.9/5  (32)

(32)

Ruby's tax basis in her partnership interest at the beginning of the partnership's tax year was $13,800. The following items were included in her Schedule K-1 from the partnership for the year:

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

(Essay)

4.8/5 (29)

What is the rationale for the specific rules partnerships must follow in determining a partnership's taxable year-end?

(Multiple Choice)

4.7/5 (44)

Which of the following statements is true when property is contributed in exchange for a partnership interest?

(Multiple Choice)

4.8/5 (47)

Ruby's tax basis in her partnership interest at the beginning of the partnership's tax year was $13,000. The following items were included in her Schedule K-1 from the partnership for the year:

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

(Essay)

4.9/5 (43)

This year, Reggie's distributive share from Almonte Partnership includes $18,000 of interest income, $14,000 of dividend income, and $70,000 of ordinary business income.

A. Assume that Reggie materially participates in the partnership. How much of his distributive share from Almonte Partnership is potentially subject to the net investment income tax?

B. Assume that Reggie does not materially participate in the partnership. How much of his distributive share from Almonte Partnership is potentially subject to the net investment income tax?

(Essay)

4.9/5 (38)

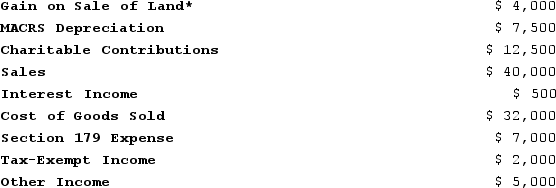

ER General Partnership, a medical supplies business, states in its partnership agreement that Erin and Ryan agree to split profits and losses according to a 40/60 ratio. Additionally, the partnership will provide Erin with a $15,000 guaranteed payment for services she provides to the partnership. ER Partnership reports the following revenues, expenses, gains, losses, and distributions for its current taxable year:

*The land is a Section 1231 asset.

Given these items, answer the following questions:

A. Compute Erin's share of ordinary income (loss) and separately stated items. Include her self-employment income as a separately stated item.

B. Compute Erin's self-employment income but assume ER Partnership is a limited partnership and Erin is a limited partner.

C. Compute Erin's self-employment income but assume ER Partnership is an LLC and Erin is personally liable for half of the debt of the LLC. Apply the IRS's proposed regulations in formulating your answer.

*The land is a Section 1231 asset.

Given these items, answer the following questions:

A. Compute Erin's share of ordinary income (loss) and separately stated items. Include her self-employment income as a separately stated item.

B. Compute Erin's self-employment income but assume ER Partnership is a limited partnership and Erin is a limited partner.

C. Compute Erin's self-employment income but assume ER Partnership is an LLC and Erin is personally liable for half of the debt of the LLC. Apply the IRS's proposed regulations in formulating your answer.

(Essay)

4.7/5 (33)

On June 12, 20X9, Kevin, Chris, and Candy Corporation came together to form Scrumptious Sweets General Partnership. Now, Scrumptious Sweets must decide which tax year-end to use. Kevin and Chris have calendar year-ends, and each holds a 35percent profits and capital interest. However, Candy Corporation has a September 30 th year-end and holds the remaining 30percent profits and capital interest. What tax year-end must Scrumptious Sweets adopt, and what rule mandates this year-end?

(Essay)

4.8/5 (33)

A partnership can elect to amortize organization and start-up costs; however, syndication costs are not deductible.

(True/False)

4.8/5 (33)

Guaranteed payments are included in the calculation of a partnership's ordinary business income (loss) and are also treated as separately stated items.

(True/False)

5.0/5 (36)

If a taxpayer sells a passive activity with suspended passive activity losses from prior years, what type of income can generally be offset by the suspended passive losses in the year of sale?

(Multiple Choice)

4.8/5 (37)

Fred has a 45 percent profits interest and 30percent capital interest in the SAP Partnership, and his tax basis before considering his share of SAP's current-year loss is $13,000. Included in his tax basis is a $4,600 share of recourse debt and a $7,300 share of nonrecourse debt. Fred is a limited partner in SAP. He is not involved in any other activities. If SAP has a $17,000 ordinary loss for the year, how much of the loss can be deducted currently, and how much of the loss is suspended because of the tax basis, at-risk, and passive activity loss limitations?

(Essay)

4.9/5 (31)

Partnerships may maintain their capital accounts according to which of the following rules?

(Multiple Choice)

4.9/5 (35)

On April 18, 20X8, Robert sold his 35 percent partnership interest in Fruit Wonder, LLC, to Richard for $121,000. Prior to selling his interest, Robert had a basis in Fruit Wonder of $81,000. Robert's basis included $6,000 of recourse debt and $16,000 of nonrecourse debt that had been allocated to him. Immediately after the purchase, what is Richard's tax basis in Fruit Wonder?

(Essay)

4.9/5 (36)

Why are guaranteed payments deducted in calculating the ordinary business income (loss) of partnerships and treated as a separately stated item for the partners that receive the payment?

(Essay)

4.9/5 (38)

Under general circumstances, debt is allocated from the partnership to each partner in the following manner:

(Multiple Choice)

4.9/5 (41)

How does a partnership make a tax election for the current year?

(Multiple Choice)

4.7/5 (45)

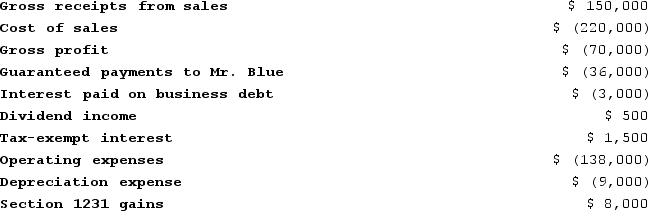

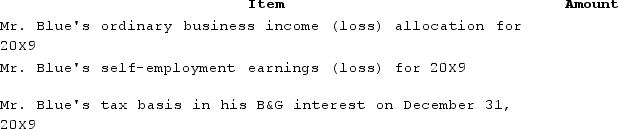

On January 1, 20X9, Mr. Blue and Mr. Grey each contributed $100,000 to form the B&G General Partnership. Their partnership agreement states that they will each receive a 50percent profits and loss interest. The partnership agreement also provides that Mr. Blue will receive an annual $36,000 guaranteed payment. B&G began business on January 1, 20X9. For its first taxable year, its accounting records contained the following information:

The $3,000 of interest was paid on a $60,000 loan made to B&G by Key Bank on June 30, 20X9. B&G repaid $10,000 of the loan on December 15, 20X9. Neither of the partners received a cash distribution from B&G in 20X9.Complete the following table related to Mr. Blue's interest in B&G partnership:

The $3,000 of interest was paid on a $60,000 loan made to B&G by Key Bank on June 30, 20X9. B&G repaid $10,000 of the loan on December 15, 20X9. Neither of the partners received a cash distribution from B&G in 20X9.Complete the following table related to Mr. Blue's interest in B&G partnership:

(Essay)

4.8/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)