Exam 13: The Us Taxation of Multinational Transactions

Exam 1: Business Income, Deductions, and Accounting Methods129 Questions

Exam 2: Property Acquisition and Cost Recovery131 Questions

Exam 3: Property Dispositions132 Questions

Exam 4: Business Entities Overview87 Questions

Exam 5: Corporate Operations126 Questions

Exam 6: Accounting for Income Taxes125 Questions

Exam 7: Corporate Taxation: Non-Liquidating Distributions122 Questions

Exam 8: Corporate Formation, Reorganization, and Liquidation121 Questions

Exam 9: Forming and Operating Partnerships131 Questions

Exam 10: Dispositions of Partnership Interests and Partnership Distributions118 Questions

Exam 11: S Corporations157 Questions

Exam 12: State and Local Taxes139 Questions

Exam 13: The Us Taxation of Multinational Transactions105 Questions

Exam 14: Transfer Taxes and Wealth Planning145 Questions

Select questions type

Ypsi Corporation has a precredit U.S. tax of $420,000 on $2,000,000 of taxable income in the current year. Ypsi has $400,000 of foreign source taxable income characterized as foreign branch income and $150,000 of foreign source taxable income characterized as passive category income. Ypsi paid $100,000 of foreign income taxes on the foreign branch income and $30,000 of foreign income taxes on the passive category income. What amount of foreign tax credit (FTC) can Ypsi use on its U.S. tax return and what is the amount of the FTC carryforward, if any?

Free

(Essay)

4.7/5  (40)

(40)

Correct Answer: Verified

Verified

$114,000 FTC with an FTC carryforward of $16,000 in the foreign branch income basket.

The foreign tax credit in the foreign branch basket is limited to the lesser of $100,000 or the FTC limitation, computed as $400,000/$2,000,000 × $420,000 = $84,000. The foreign tax credit in the passive category basket is limited to the lesser of $30,000 or the FTC limitation, computed as $150,000/$2,000,000 × $420,000 = $31,500. The total FTC is $84,000 + $30,000 = $114,000, leaving a $16,000 carryforward in the foreign branch income basket.

Gwendolyn was physically present in the United States for 106 days in 2020, 228 days in 2019, and 126 days in 2018. Under the substantial presence test formula, how many days is Gwendolyn deemed physically present in the United States in 2020?

Free

(Multiple Choice)

4.9/5 (36)

Correct Answer:Verified

B

Giselle is a citizen and resident of Brazil, a country with which the United States does not have an income tax treaty. Giselle earned $24,000 of compensation while working within the United States. She worked 60 days in the United States and 180 days in Brazil. How much of her compensation earned in the United States will be subject to U.S. tax?

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

A

Rafael is a citizen of Spain and a resident of the United States. During the current year, Rafael received the following income:

Compensation of $5 million from competing in tennis matches in the U.S.

Cash dividends of $10,000 from a Spanish corporation that earns 50 percent of its income from sales in the United States

Interest of $2,000 from a Spanish citizen who is a resident of the U.S.

Rent of $5,000 from U.S. residents who rented his villa in Italy

Gain of $10,000 on the sale of stock in a German corporation

Determine the source (U.S. or foreign) of each item of income Rafael received.

(Essay)

4.8/5 (41)

Reno Corporation, a U.S. corporation, reported total taxable income of $6,000,000 in the current year. Taxable income included $1,800,000 of foreign source taxable income from the company's branch operations in Canada. All of the branch income is foreign branch income. Reno paid Canadian income taxes of $450,000 on its branch income. Compute Reno's net U.S. tax liability and any foreign tax credit carryover. Assume an exchange rate of C$1 = $1.

(Essay)

4.7/5 (34)

Reno Corporation, a U.S. corporation, reported total taxable income of $6,260,000 in the current year. Taxable income included $1,878,000 of foreign source taxable income from the company's branch operations in Canada. All of the branch income is foreign branch income. Reno paid Canadian income taxes of $463,000 on its branch income. Compute Reno's net U.S. tax liability and any foreign tax credit carryover. Assume an exchange rate of C$1 = $1.

(Essay)

4.8/5 (38)

U.S. corporations are eligible for a foreign tax credit for withholding taxes imposed on dividends received from 100 percent owned foreign corporations, even if the dividend qualifies for the 100 percent dividends received deduction.

(True/False)

4.7/5 (42)

Which of the following persons should not be treated as a "U.S. shareholder" of a controlled foreign corporation (CFC) for subpart F purposes?

(Multiple Choice)

4.9/5 (38)

Spartan Corporation, a U.S. company, manufactures widgets for sale in the United States and Europe. All manufacturing activities take place in the United States. During the current year, Spartan sold 150,000 widgets to European customers at a price of $6.00 each. Each widget costs $4.00 to produce. All of Spartan's production assets are located in the United States. Spartan ships its widgets FOB, place of destination. What amount of Spartan's gross profit is treated as coming from foreign sources?

(Essay)

4.8/5 (34)

Pierre Corporation has a precredit U.S. tax of $315,000 on $1,500,000 of taxable income in the current year. Pierre has $300,000 of foreign source taxable income characterized as foreign branch income and $150,000 of foreign source taxable income characterized as passive category income. Pierre paid $60,000 of foreign income taxes on the foreign branch income and $15,000 of foreign income taxes on the passive category income. What amount of foreign tax credit (FTC) can Pierre use on its current U.S. tax return and what is the amount of the carryforward, if any?

(Multiple Choice)

4.9/5 (34)

Cecilia, a Brazilian citizen and resident, spent 120 days working in the United States in the current year and earned $50,000. Because she spent more than 90 days in the United States, Cecilia's income will be treated as U.S. source and subject to U.S. taxation. The United States does not have an income tax treaty with Brazil.

(True/False)

4.7/5 (24)

A hybrid entity established in Ireland is treated as a flow-through entity for U.S. tax purposes and a corporation for Irish tax purposes.

(True/False)

4.9/5 (33)

Horton Corporation is a 100 percent owned Canadian subsidiary of Cruller Corporation, a U.S. corporation. During the current year, Horton paid a dividend of C$630,000 to Cruller. The dividend qualifies for the 100 percent dividends received deduction. The dividend was subject to a withholding tax of C$38,000. Assume an exchange rate of C$1 = $1. Cruller reported U.S. source taxable income of $2,400,000 before considering the dividend received from Horton Corporation. Compute the tax consequences to Cruller as a result of this dividend.

(Multiple Choice)

4.7/5 (38)

Austin Corporation, a U.S. corporation, received the following investment income during the current year: $50,000 of dividend income from ownership of stock in a French corporation, $20,000 interest on a loan to its Dutch subsidiary, $40,000 royalty from its 50 percent owned Irish venture, and $30,000 capital gain from sale of its stock in a Brazilian corporation. How much of Austin's income is treated as foreign source?

(Multiple Choice)

4.9/5 (36)

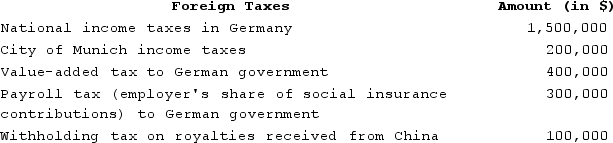

Rainier Corporation, a U.S. corporation, manufactures and sells quidgets in the United States and Europe. Rainier conducts its operations in Europe through a German GmbH, which the company elects to treat as a branch for U.S. tax purposes. Rainier also licenses the rights to manufacture quidgets to an unrelated company in China. During the current year, Rainier paid the following foreign taxes, translated into U.S. dollars at the appropriate exchange rate:

What amount of creditable foreign taxes does Rainier incur?

What amount of creditable foreign taxes does Rainier incur?

(Essay)

4.9/5 (42)

Portsmouth Corporation, a British corporation, is a wholly owned subsidiary of Salem Corporation, a U.S. corporation. During the year, Portsmouth reported the following income:

$250,000 interest income received from a loan to an unrelated French corporation.

$100,000 dividend income received from a less than 1 percent owned unrelated Dutch corporation.

$150,000 rent income from an unrelated British corporation on property Portsmouth actively manages.

$500,000 gross profit from the sale of inventory manufactured by Portsmouth in Great Britain and sold to a 100 percent owned subsidiary in Germany.

What amount of subpart F income does Portsmouth recognize in the current year?

(Essay)

4.8/5 (29)

Subpart F income earned by a CFC will always be treated as a deemed dividend to the CFC's U.S. shareholders in the year the subpart F income is earned.

(True/False)

4.8/5 (35)

Gwendolyn was physically present in the United States for 90 days in 2020, 180 days in 2019, and 30 days in 2018. Under the substantial presence test formula, how many days is Gwendolyn deemed physically present in the United States in 2020?

(Multiple Choice)

4.8/5 (30)

Which of the following transactions engaged in by a Swiss controlled foreign corporation creates foreign base company sales income?

(Multiple Choice)

4.8/5 (41)

Boca Corporation, a U.S. corporation, reported U.S. taxable income of $1,000,000 in the current year. Boca also received a dividend of $100,000 from the corporation's 100 percent owned subsidiary in Italy. The dividend qualifies for the 100 percent dividends received deduction. The Italian government imposed a withholding tax of $5,000 on the dividend. Compute Boca Corporation's net U.S. tax liability for the current year.

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)