Exam 9: Forming and Operating Partnerships

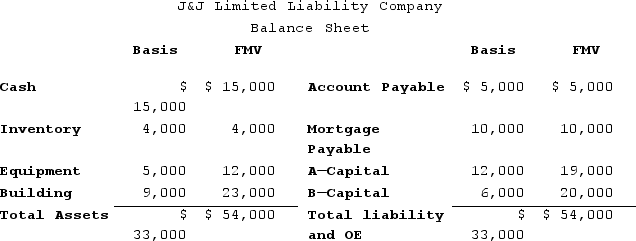

J&J, LLC, was in its third year of operations when J&J decided to expand the number of members from two, A and B, with equal profits and capital interests, to three members, A, B, and C. The third member, C, will contribute her financial expertise to the LLC in exchange for a one-third capital interest in J&J. Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J, when C receives her capital interest? If, instead, member C receives a one-third profits interest, what would be the tax consequences to members A, B, and C, and to J&J?

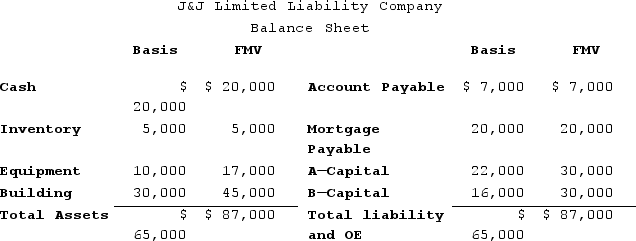

If member C received a one-third capital interest for her services, the following tax consequences would result:A is allocated a ${{[a(20)]:#,###}} expense, reducing A's FMV capital account to ${{[a(23)]:#,###}} and his tax basis capital account to ${{[a(22)]:#,###}}. His tax basis would include a one-third share of the LLC debt, or ${{[a(26)]:#,###}}.B is allocated a ${{[a(21)]:#,###}} expense, reducing B's FMV capital account to ${{[a(25)]:#,###}} and his tax basis capital account to ${{[a(24)]:#,###}}. His tax basis would include a one-third share of the LLC debt, or ${{[a(26)]:#,###}}.C reports ordinary income of ${{[a(19)]:#,###}} as a guaranteed payment for services provided. C's FMV and tax basis capital account will equal ${{[a(19)]:#,###}}. Her tax basis would include a one-third share of the LLC debt, or ${{[a(26)]:#,###}}.J&J, LLC-No gain or loss recognized and no adjustments to assets and liabilities. Members' capital accounts are adjusted as indicated.If member C received a one-third profits interest for her services, the following tax consequences would result:A-No deduction would be available to member A because member C would not receive anything if the LLC were to liquidate immediately after the contribution. His tax basis would include a one-third share of the LLC debt, or ${{[a(26)]:#,###}}.B-No deduction would be available to member B because member C would not receive anything if the LLC were to liquidate immediately after the contribution. His tax basis would include a one-third share of the LLC debt, or ${{[a(26)]:#,###}}.C-Member C would not recognize any income because the liquidation value of her partnership interest is zero with a profits interest. Additionally, member C would have ${{[a(31)]:#}} in both her FMV and tax basis capital accounts. Her tax basis would include a one-third share of the LLC debt, or ${{[a(26)]:#,###}}. From this point forward, C's capital accounts will be adjusted to reflect her share of future LLC profits and losses.J&J, LLC-No gain or loss recognized and no adjustments to assets and liabilities.

Frank and Bob are equal members in Soxy Socks, LLC. When forming the LLC, Frank contributed $50,000 in cash and $50,000 worth of equipment. Frank's adjusted basis in the equipment was $35,000. Bob contributed $50,000 in cash and $50,000 worth of land. Bob's adjusted basis in the land was $30,000. On 3/15/X4, Soxy Socks sells the land Bob contributed for $60,000. How much gain (loss) related to this transaction will Bob report on his X4 return?

C

Which person would generally be treated as a material participant in an activity?

D

Styling Shoes, LLC, filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax bases at the beginning of 20X8: (1) Jane, a member with a 25percent profits and capital interest and a $5,000 outside basis, (2) Joe, a member with a 45percent profits and capital interest and a $10,000 outside basis, and (3) Jack, a member with a 30percent profits and capital interest and a $2,000 outside basis. The following items were reported on Styling's Schedule K for the year: ordinary income of $100,000, Section 1231 gain of $15,000, charitable contributions of $25,000, and tax-exempt income of $3,000. In addition, Styling received an additional bank loan of $12,000 during 20X8. What is Jane's tax basis after adjustment for her share of these items?

Actual or deemed cash distributions in excess of a partner's outside basis are generally taxable as capital gains.

If a partner participates in partnership activities on a regular, continuous, and substantial basis, then the partnership's activities with respect to this individual partner are not considered passive.

On January 1, X9, Gerald received his 50percent profits and capital interest in High Air, LLC, in exchange for $2,000 in cash and real property with a $3,000 tax basis secured by a $2,000 nonrecourse mortgage. High Air reported a $15,000 loss for its X9 calendar year. How much loss can Gerald deduct, and how much loss must he suspend if he only applies the tax basis loss limitation?

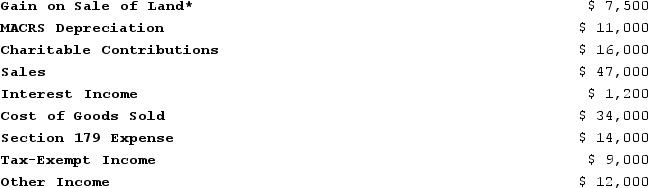

ER General Partnership, a medical supplies business, states in its partnership agreement that Erin and Ryan agree to split profits and losses according to a 40/60 ratio. Additionally, the partnership will provide Erin with a $22,000 guaranteed payment for services she provides to the partnership. ER Partnership reports the following revenues, expenses, gains, losses, and distributions for its current taxable year:

*The land is a Section 1231 asset.

Given these items, answer the following questions:

A. Compute Erin's share of ordinary income (loss) and separately stated items. Include her self-employment income as a separately stated item.

B. Compute Erin's self-employment income but assume ER Partnership is a limited partnership and Erin is a limited partner.

C. Compute Erin's self-employment income but assume ER Partnership is an LLC and Erin is personally liable for half of the debt of the LLC. Apply the IRS's proposed regulations in formulating your answer.

*The land is a Section 1231 asset.

Given these items, answer the following questions:

A. Compute Erin's share of ordinary income (loss) and separately stated items. Include her self-employment income as a separately stated item.

B. Compute Erin's self-employment income but assume ER Partnership is a limited partnership and Erin is a limited partner.

C. Compute Erin's self-employment income but assume ER Partnership is an LLC and Erin is personally liable for half of the debt of the LLC. Apply the IRS's proposed regulations in formulating your answer.

Gerald received a one-third capital and profit (loss) interest in XYZ Limited Partnership (LP). In exchange for this interest, Gerald contributed a building with an FMV of $17,000. His adjusted basis in the building was $8,500. In addition, the building was encumbered with a $5,100 nonrecourse mortgage that XYZ LP assumed at the time the property was contributed. What is Gerald's outside basis immediately after his contribution?

A purchased partnership interest has a holding period beginning on the date of purchase regardless of the type of property held by the partnership.

Frank and Bob are equal members in Soxy Socks, LLC. When forming the LLC, Frank contributed $60,000 in cash and $60,000 worth of equipment. Frank's adjusted basis in the equipment was $45,000. Bob contributed $60,000 in cash and $60,000 worth of land. Bob's adjusted basis in the land was $20,000. On 3/15/X4, Soxy Socks sells the land Bob contributed for $68,000. How much gain (loss) related to this transaction will Bob report on his X4 return?

Tim, a real estate investor, Ken, a dealer in securities, and Hardware, Incorporated, a retail lumber store, form a partnership called HKT, LP. HKT is in the home-building business. Tim recently purchased his interest in HKT, while the other partners purchased their interests several years ago. During X3, HKT reports a $12,000 gain from the sale of a stock in a wholesale lumber company it purchased in X1 for investment purposes. Which of the following statements best represents how their portion of the gain should be reported to the partner?

How does additional debt or relief of debt affect a partner's basis?

Greg, a 40percent partner in GSS Partnership, contributed land to the partnership in exchange for his partnership interest when the partnership was formed. At the time, his basis in the land was $30,000 and its FMV was $133,000. Three years after the partnership was formed, GSS Partnership decided to sell the land to an unrelated party for $150,000. When the land is sold, how much of the gain should be allocated to each partner of GSS Partnership if Sam and Steve are each 30percent partners?

Ruby's tax basis in her partnership interest at the beginning of the partnership's tax year was $13,000. The following items were included in her Schedule K-1 from the partnership for the year:

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

J&J, LLC, was in its third year of operations when J&J decided to expand the number of members from two, A and B, with equal profits and capital interests, to three members, A, B, and C. The third member, C, will contribute her financial expertise to the LLC in exchange for a one-third capital interest in J&J. Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J, when C receives her capital interest? If, instead, member C receives a one-third profits interest, what would be the tax consequences to members A, B, and C, and to J&J?

Ruby's tax basis in her partnership interest at the beginning of the partnership's tax year was $13,500. The following items were included in her Schedule K-1 from the partnership for the year:

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

Determine what amounts related to these items Ruby will report on her tax return assuming her tax basis and at-risk amount are equal and that she is a material participant in the partnership's activities. Further, assume that Ruby and her husband, Gerald, are not involved in any other trade or business and that they file a joint return every year.

What is the difference between a partner's tax basis and at-risk amount?

Which of the following statements regarding the process for determining a partnership's tax year-end is true?

Adjustments to a partner's outside basis are made annually to prevent double taxation on the sale of a partnership interest or at the time of a partnership distribution.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)