Exam 9: Forming and Operating Partnerships

Exam 1: Business Income, Deductions, and Accounting Methods129 Questions

Exam 2: Property Acquisition and Cost Recovery131 Questions

Exam 3: Property Dispositions132 Questions

Exam 4: Business Entities Overview87 Questions

Exam 5: Corporate Operations126 Questions

Exam 6: Accounting for Income Taxes125 Questions

Exam 7: Corporate Taxation: Non-Liquidating Distributions122 Questions

Exam 8: Corporate Formation, Reorganization, and Liquidation121 Questions

Exam 9: Forming and Operating Partnerships131 Questions

Exam 10: Dispositions of Partnership Interests and Partnership Distributions118 Questions

Exam 11: S Corporations157 Questions

Exam 12: State and Local Taxes139 Questions

Exam 13: The Us Taxation of Multinational Transactions105 Questions

Exam 14: Transfer Taxes and Wealth Planning145 Questions

Select questions type

Clint noticed that the Schedule K-1 he just received from ABC Partnership included a $19,600 ordinary business loss allocation. His tax basis in ABC at the beginning of ABC's most recent tax year was $9,600. Comparing the Schedule K-1 he recently received from ABC with the Schedule K-1 he received from ABC last year, Clint noted that his share of ABC partnership debt changed as follows: recourse debt increased from $0 to $1,600, qualified nonrecourse debt increased from $0 to $2,600, and nonrecourse debt increased from $0 to $2,600. Finally, the Schedule K-1 Clint recently received from ABC reflected a $600 cash contribution he made to ABC during the year.

Clint is not a material participant in ABC Partnership, and he received $9,600 of passive income from another investment during the same year he received the loss allocation from ABC. How much of the $19,600 loss from ABC can Clint deduct currently, and how much of the loss is suspended because of the tax basis, at-risk, and passive activity loss limitations?

(Essay)

4.8/5  (33)

(33)

Lincoln, Incorporated, Washington, Incorporated, and Adams, Incorporated, form Presidential Suites Partnership on February 15, 20X9. Now, Presidential Suites must adopt its required tax year-end. The partners' year-ends, profits interests, and capital interests are reflected in the table below. Given this information, what tax year-end must Presidential Suites use, and what rule requires this year-end?

(Essay)

4.7/5 (35)

Partnerships can request up to a six-month extension by filing IRS Form 7004 prior to the original due date of the partnership return.

(True/False)

4.7/5 (37)

Jay has a tax basis of $20,000 in his partnership interest at the beginning of the partnership tax year. The following amounts of partnership debt were allocated to Jay and are included in his beginning-of-the-year tax basis: (1) recourse debt-$9,000, (2) qualified nonrecourse debt-$1,000, and (3) nonrecourse debt-$1,100. There were no changes to the debt allocated to Jay during the tax year. If Jay is allocated a $21,000 loss for the current year, how much of the loss will be suspended under the tax basis and at-risk limitations?

(Multiple Choice)

4.9/5 (24)

Sue and Andrew form SA general partnership. Each person receives an equal interest in the newly created partnership. Sue contributes $28,000 of cash and land with an FMV of $73,000. Her basis in the land is $38,000. Andrew contributes equipment with an FMV of $30,000 and a building with an FMV of $51,000. His basis in the equipment is $26,000, and his basis in the building is $38,000. How much gain must the SA general partnership recognize on the transfer of these assets from Sue and Andrew?

(Multiple Choice)

4.9/5 (49)

Sarah, Sue, and AS Incorporated formed a partnership on May 1, 20X9, called SSAS, LP. Now that the partnership is formed, they must determine its appropriate year-end. Sarah has a 30percent profits and capital interest while Sue has a 35percent profits and capital interest. Both Sarah and Sue have calendar year-ends. AS Incorporated holds the remaining profits and capital interest in the LP, and it has a September 30 year-end. What tax year-end must SSAS, LP, use for 20X9, and which test or rule requires this year-end?

(Multiple Choice)

4.8/5 (43)

XYZ, LLC, has several individual and corporate members. Abe and Joe, individuals with 4/30 year-ends, each have a 23percent profits and capital interest. RST, Incorporated, a corporation with a 6/30 year-end, owns a 4percent profits and capital interest, while DEF, Incorporated, a corporation with an 8/30 year-end, owns a 4.9percent profits and capital interest. Finally, 30 other calendar year-end individual partners (each with less than a 2percent profits and capital interest) own the remaining 45percent of the profits and capital interests in XYZ. What tax year-end should XYZ use, and which test or rule requires this year-end?

(Multiple Choice)

4.9/5 (37)

Which of the following statements exemplifies the entity theory of partnership taxation?

(Multiple Choice)

4.9/5 (28)

Hilary had an outside basis in LTL General Partnership of $10,000 at the beginning of the year. LTL reported the following items on Hilary's K-1 for the year: ordinary business income of $5,000, a $10,000 reduction in Hilary's share of partnership debt, a cash distribution of $20,000, and tax-exempt income of $3,000. What is Hilary's adjusted basis at the end of the year?

(Multiple Choice)

4.8/5 (30)

Kim received a one-third profits and capital interest in Bright Line, LLC, in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $23,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: sales-$143,000, cost of goods sold-$83,000, depreciation expense-$40,000, long-term capital gains-$8,000, qualified dividends-$5,300, and municipal Bond interest-$3,300. How much ordinary business income (loss) will Bright Line allocate to Kim on her Schedule K-1 for X4?

(Multiple Choice)

4.8/5 (31)

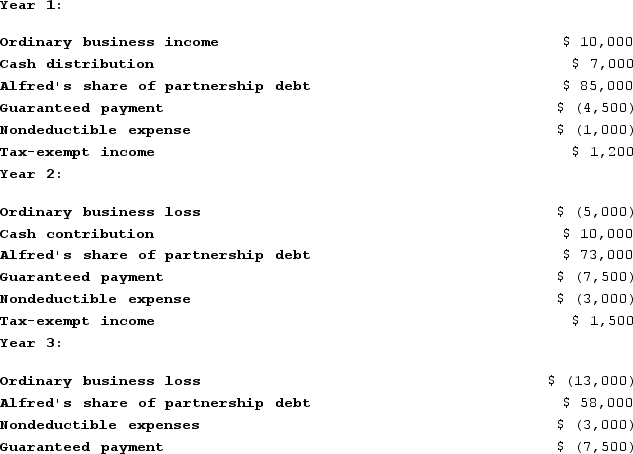

Alfred, a one-third profits and capital partner in Pizzeria Partnership, needs help in adjusting his tax basis to reflect the information contained in his most recent Schedule K-1 from the partnership. Unfortunately, the Schedule K-1 he recently received was for Year 3 of the partnership, but Alfred only knows that his tax basis at the beginning of Year 2 of the partnership was $23,000. Thankfully, Alfred still has his Schedule K-1 from the partnership for Years 1 and 2.

Using the following information from Alfred's Year 1, Year 2, and Year 3 Schedule K-1, calculate his tax basis the end of Year 2 and Year 3.

(Essay)

4.8/5 (32)

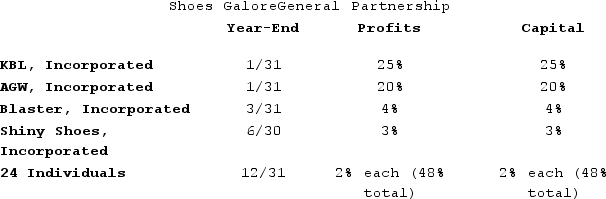

KBL, Incorporated, AGW, Incorporated, Blaster, Incorporated, Shiny Shoes, Incorporated, and a group of 24 individuals form Shoes Galore General Partnership on October 11, 20X9. Now, Shoes Galore must adopt its required tax year-end. The partners' year-ends, profits interests, and capital interests are reflected in the table below. Given this information, what tax year-end must Shoes Galore use, and what rule requires this year-end?

(Essay)

4.8/5 (33)

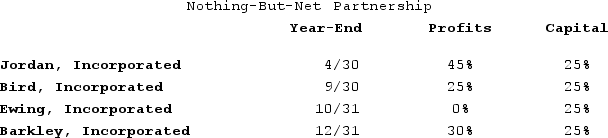

Jordan, Incorporated, Bird, Incorporated, Ewing, Incorporated, and Barkley, Incorporated, formed Nothing-But-Net Partnership on June 1st, 20X9. Now, Nothing-But-Net must adopt its required tax year-end. The partners' year-ends, profits interests, and capital interests are reflected in the table below. Given this information, what tax year-end must Nothing-But-Net use, and what rule requires this year-end?

(Essay)

4.9/5 (41)

Which of the following rationales for adjusting a partner's basis is false?

(Multiple Choice)

4.8/5 (33)

Erica and Brett decide to form their new motorcycle business as an LLC. Each will receive an equal profits (loss) interest by contributing cash, property, or both. In addition to the members' contributions, their LLC will obtain a $45,000 nonrecourse loan from First Bank at the time it is formed. Brett contributes cash of $4,000 and a building he bought as a storefront for the motorcycles. The building has an FMV of $40,000 and an adjusted basis of $25,000 and is secured by a $30,000 nonrecourse mortgage that the LLC will assume. What is Brett's outside tax basis in his LLC interest?

(Multiple Choice)

4.8/5 (37)

The character of each separately stated item is determined at the partner level.

(True/False)

4.8/5 (35)

In what order are the loss limitations for partnerships applied?

(Multiple Choice)

4.9/5 (35)

Erica and Brett decide to form their new motorcycle business as an LLC . Each will receive an equal profits (loss) interest by contributing cash, property, or both. In addition to the members' contributions, their LLC will obtain a $50,000 nonrecourse loan from First Bank at the time it is formed. Brett contributes cash of $5,000 and a building he bought as a storefront for the motorcycles. The building has an FMV of $45,000and an adjusted basis of $30,000 and is secured by a $35,000 nonrecourse mortgage that the LLC will assume. What is Brett's outside tax basis in his LLC interest?

(Multiple Choice)

4.7/5 (36)

An additional allocation of partnership debt or relief of partnership debt is considered to be a deemed cash contribution or cash distribution, respectively.

(True/False)

4.9/5 (35)

A partner's tax basis or at-risk amount can be increased by making capital contributions, by paying off partnership debt, or by increasing the profitability of the partnership.

(True/False)

5.0/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)