Exam 12: Perfect Competition and the Supply Curve

Exam 1: First Principles246 Questions

Exam 2: Economic Models: Trade-Offs and Trade72 Questions

Exam 3: Supply and Demand266 Questions

Exam 4: Consumer and Producer Surplus196 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets203 Questions

Exam 6: Elasticity329 Questions

Exam 7: Taxes284 Questions

Exam 8: International Trade265 Questions

Exam 9: Decision Making by Individuals and Firms209 Questions

Exam 10: The Rational Consumer477 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs282 Questions

Exam 12: Perfect Competition and the Supply Curve320 Questions

Exam 13: Monopoly258 Questions

Exam 14: Oligopoly212 Questions

Exam 15: Monopolistic Competition and Product Differentiation223 Questions

Exam 16: Externalities234 Questions

Exam 17: Public Goods and Common Resources237 Questions

Exam 18: The Economics of the Welfare State144 Questions

Exam 19: Factor Markets and the Distribution of Income241 Questions

Exam 20: Uncertainty, Risk, and Private Information199 Questions

Select questions type

Bob runs a pedicure business in a perfectly competitive industry.He knows that he will break even if the price of pedicures is $15 but that he will have to shut down if the price is $11.If the market demand in the industry is P = 30 - (0.2)Q and the market supply is P = (0.2)Q, then in the short run, Bob will:

A.shut down, since he cannot cover any of his variable costs.

B.produce, since he is at his break-even level.

C.produce with a loss, since he is operating at a price below his break-even level.

D.shut down, although he is making a positive economic profit.

Free

(Essay)

4.9/5  (39)

(39)

Correct Answer: Verified

Verified

produce, since he is at his break-even level.

In a perfectly competitive industry, each firm:

A.is a price-maker.

B.produces about half of the total industry output.

C.produces a differentiated product.

D.produces a standardized product.

Free

(Essay)

4.8/5 (34)

Correct Answer:Verified

produces a standardized product.

Price-takers are individuals in a market who:

A.select a price from a wide range of alternatives.

B.select the lowest price available in a competitive market.

C.select the average of prices available in a competitive market.

D.have no ability to affect the price of a good in a market.

Free

(Essay)

4.8/5 (34)

Correct Answer:Verified

have no ability to affect the price of a good in a market.

(Table: Total Cost and Output) The table describes Sergei's total costs for his perfectly competitive all natural ice cream firm.If there are 100 firms in the all-natural ice cream industry, which of the following is a point on the industry short-run supply curve?

A.P = $10; Q = 0.

B.P = $20; Q = 200.

C.P = $110; Q = 3.

D.P = $75; Q = 500.

(Essay)

4.9/5 (28)

If a perfectly competitive firm is producing a quantity where MC = MR, then profit:

A.is maximized.

B.can be increased by increasing production.

C.can be increased by decreasing production.

D.can be increased by decreasing the price.

(Essay)

4.9/5 (29)

Lilly is the price-taking owner of an apple orchard.The price of apples is high enough that Lilly is earning positive economic profits.In the long run, Lilly should expect:

A.lower apple prices due to the entry of new firms.

B.higher apple prices due to the exit of existing firms.

C.lower apple prices due to the exit of existing firms.

D.higher apple prices due to the entry of new firms.

(Essay)

4.8/5 (42)

Figure: Revenues, Costs, and Profits III for Tomato Producers

(Figure: Revenues, Costs, and Profits III for Tomato Producers) Look at the figure Revenues, Costs, and Profits III for Tomato Producers.The market for tomatoes is perfectly competitive, and an individual tomato farmer faces the cost curves shown in the figure.If the market price of a bushel of tomatoes is $14, the farmer's profit-maximizing output is bushels.

(Multiple Choice)

4.8/5 (35)

If a firm in perfect competition sells 10 units of output at a market price of $5 per unit, its marginal revenue is:

A.$5.

B.more than $5 but less than $50.

C.$50.

D.$250.

(Essay)

4.9/5 (38)

Which of the following is true?

A.If the price falls below the average total cost, the firm will shut down in the short run.

B.Price and marginal revenue are the same in perfect competition.

C.Economic profit per unit is found by subtracting AVC from the price.

D.Economic profit is always positive in the short run.

(Essay)

4.8/5 (27)

If firms are experiencing economic losses in the short run, firms will leave the industry, industry output will ________, and economic losses will in the long run.

A.fall; fall

B.rise; fall

C.rise; rise

D.fall; rise

(Essay)

4.7/5 (42)

A perfectly competitive firm will earn a profit in the short run when it produces the profit- maximizing quantity of output and the price is:

A.greater than marginal cost.

B.less than marginal cost.

C.less than average variable cost.

D.greater than average total cost.

(Essay)

4.7/5 (34)

Figure: Revenues, Costs, and Profits II for Tomato Producers

(Figure: Revenues, Costs, and Profits II for Tomato Producers) Look at the figure Revenues, Costs, and Profits II for Tomato Producers.The market for tomatoes is perfectly competitive, and an individual tomato farmer faces the cost curves shown in the figure.The market price of a bushel of tomatoes is $10.At the farmer's profit-maximizing output, total revenue is

________, total cost is ________, and profit is _.

A.$90; $72; $18

B.$56; $56; $0

C.$30; $48; -$18

D.$48; $56; -$8

(Essay)

4.9/5 (35)

The assumptions of perfect competition imply that:

A.individuals in the market accept the market price as given.

B.individuals can influence the market price.

C.the price will be fair.

D.the price will be low.

(Essay)

4.8/5 (29)

(Table: Variable Costs for Lawns) Look at the table Variable Costs for Lawns.During the summer Alex runs a lawn-mowing service, and lawn-mowing is a perfectly competitive industry made up of 100 identical firms.The table shows his variable costs for lawn-mowing and the number of lawns mowed.Alex's fixed cost is $1,000 for the mower.His variable costs include fuel, his time, and mower parts.If the price for mowing a lawn is $60, how much is Alex's total revenue at the profit-maximizing output?

A.$60

B.$1,100

C.$2,400

D.$2,100

(Essay)

5.0/5 (37)

Which of the following is not a characteristic of a perfectly competitive industry?

A.Firms seek to maximize profits.

B.Profits may be positive in the short run.

C.There are many firms.

D.There are differentiated products.

(Essay)

4.8/5 (35)

The slope of the total revenue curve is:

A.marginal cost.

B.net revenue.

C.constant under perfect competition.

D.varying under perfect competition.

(Essay)

4.7/5 (35)

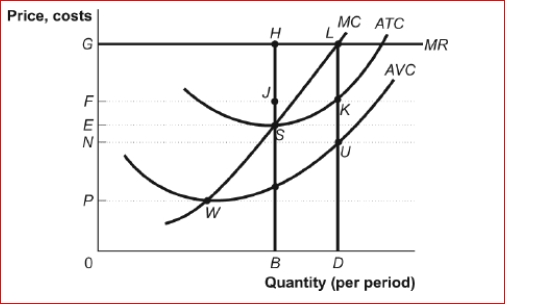

Figure: A Perfectly Competitive Firm in the Short Run

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly Competitive Firm in the Short Run.The firm's total cost of producing its most profitable level of output is:

A.BS.

B.DK.

C.0FKD.

D.0ESB.

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly Competitive Firm in the Short Run.The firm's total cost of producing its most profitable level of output is:

A.BS.

B.DK.

C.0FKD.

D.0ESB.

(Essay)

4.8/5 (25)

A perfectly competitive tomato industry is in long-run equilibrium.Now suppose that some consumers are getting sick by eating tomatoes that contain salmonella.Describe how this change will affect short-run economic profits.What will happen to the number of tomato growers in the long run? How will price and output in this industry adjust in the long run?

(Essay)

4.9/5 (26)

The slope of the total cost curve is:

A.marginal cost.

B.marginal revenue.

C.constant under perfect competition.

D.always negative.

(Essay)

4.8/5 (31)

A perfectly competitive industry with constant costs initially operates in long-run equilibrium.When demand increases, one will observe that:

A.in the short run, prices and profits will be higher, but in the long run, price will fall back to its original level and firms will again earn zero economic profit.

B.in the long and short runs, prices and profits will be higher relative to what they were before the demand increase.

C.in the short run, prices and profits will fall, but in the long run, price will rise back to its initial level, as will profits.

D.in the long and short runs, prices and profits will be lower relative to what they were before the demand increase.

(Essay)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)