Exam 8: Risk, Return, and Portfolio Theory

Exam 1: An Introduction to Finance53 Questions

Exam 2: Business Corporate Finance68 Questions

Exam 3: Financial Statements49 Questions

Exam 4: Financial Statement Analysis and Forecasting90 Questions

Exam 5: Time Value of Money82 Questions

Exam 6: Bond Valuation and Interest Rates77 Questions

Exam 7: Equity Valuation101 Questions

Exam 8: Risk, Return, and Portfolio Theory111 Questions

Exam 9: The Capital Asset Pricing Model Capm115 Questions

Exam 10: Market Efficiency52 Questions

Exam 11: Forwards, Futures, and Swaps56 Questions

Exam 12: Options55 Questions

Exam 13: Capital Budgeting, Risk Considerations, and Other Special Issues149 Questions

Exam 14: Cash Flow Estimation and Capital Budgeting Decisions127 Questions

Exam 15: Mergers and Acquisitions88 Questions

Exam 16: Leasing34 Questions

Exam 17: Investment Banking and Securities Law68 Questions

Exam 18: Debt Instruments52 Questions

Exam 19: Equity and Hybrid Instruments67 Questions

Exam 20: Cost of Capital68 Questions

Exam 21: Capital Structure Decisions69 Questions

Exam 22: Dividend Policy53 Questions

Exam 23: Working Capital Management: General Issues51 Questions

Exam 24: Working Capital Management: Current Assets and Current Liabilities78 Questions

Select questions type

You have observed the following for Montreal Smoked Meat Ltd.:

What are the arithmetic and geometric average weekly returns over the 6-week period ended June 15, 2016?

What are the arithmetic and geometric average weekly returns over the 6-week period ended June 15, 2016?

(Multiple Choice)

4.8/5  (39)

(39)

You have given the following forecasts for the economy and Stock A: (1)the probability of having a recession next year is 30.0%, a normal economy is 55.0%, and an expansion is 15.0%, and (2)the price of Stock A will be $9 if the economy is in recession, $15 if the economy is normal, and $18 if the economy is in expansion.What is the ex ante standard deviation of Stock A's returns if it is currently selling for $12?

(Multiple Choice)

4.9/5 (35)

Given the following forecasts, what is the expected return for a portfolio that has $1,500 invested in Stock A and $4,500 invested in Stock B?

(Multiple Choice)

4.8/5 (32)

Which of the following is a FALSE statement of the correlation coefficient?

(Multiple Choice)

4.9/5 (41)

Given the information in the following table, what is the expected return of the security?

(Multiple Choice)

4.8/5 (35)

The expected returns for Hickory Inc.and Dickory Inc.are 8.0% and 13.0%, respectively.The standard deviation is 12.0% for Hickory and 18.0% for Dickory.What is the portfolio standard deviation if 40.0% of the portfolio is in Hickory and there is no relationship between the returns on the two securities?

(Multiple Choice)

4.9/5 (40)

Suppose you own a two-security portfolio.You have 35.0% of your money invested in Security X and the remainder in Security Y.The standard deviations of Securities X and Y are 10.0% and 15.0%, respectively.What is the correlation between the two securities if the portfolio variance is 0.013225?

(Multiple Choice)

4.9/5 (43)

If a company's stock price decreases due to the poor sales in one of its product lines, this is an example of:

(Multiple Choice)

4.9/5 (32)

La Maudite Ltd.'s annual returns for the past five years were: 11.5%, 18%, -12%, -16.5%, and 28%.What are the arithmetic and geometric average annual returns for La Maudite over the five-year period?

(Multiple Choice)

4.8/5 (36)

Baxter Inc.'s annual returns for the past four years were: 2.75%, -1.8%, 7.2%, and 6.5%.What are the arithmetic and geometric average annual returns for Baxter over the four-year period?

(Multiple Choice)

4.9/5 (36)

The following table shows the closing prices and daily returns of Toronto Skates Inc.over a week:

Calculate the weekly geometric mean (GM)and the arithmetic mean (AM)returns of Toronto Skates Inc.(your answer should be four decimals, margin of error is +/- 0.0050%)

Calculate the weekly geometric mean (GM)and the arithmetic mean (AM)returns of Toronto Skates Inc.(your answer should be four decimals, margin of error is +/- 0.0050%)

(Multiple Choice)

4.9/5 (34)

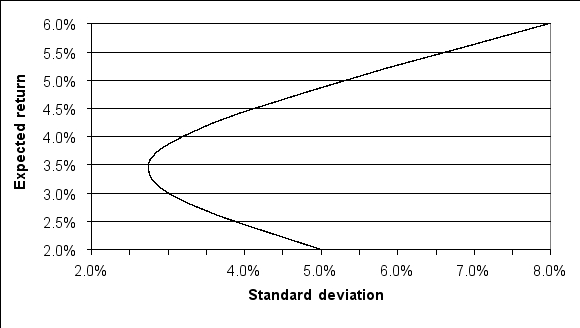

For the following efficient frontier, the expected return of the minimum variance portfolio is:

(Multiple Choice)

4.7/5 (35)

A portfolio consists of three securities: Treachery (T), Sleazy (S), and Felony (F).The expected returns for Treachery, Sleazy, and Felony are 10.0%, 8.0%, and 16.0%, respectively.The standard deviation is 15.0% for Treachery, 20.0% for Sleazy, and 25.0% for Felony.The covariance of the returns on the three securities is: COVTS = 0.0144, COVTF = 0.0084, and COVSF = 0.03.What is the portfolio standard deviation if 20.0% of the portfolio is in Treachery and 35.0% is in Sleazy?

(Multiple Choice)

4.8/5 (30)

The expected returns for ABC Company and XYZ Company are 12.0% and 9.0%, respectively.The standard deviation is 20.0% for ABC and 15.0% for XYZ.What is the portfolio standard deviation if one-third of the portfolio is in ABC and the two securities have perfect positive correlation?

(Multiple Choice)

4.7/5 (40)

A portfolio consists of two securities: Nervy and Goofy.The expected return of Nervy is 12.0% with a standard deviation of 15.0%.The expected return of Goofy is 9.0% with a standard deviation of 10.0%.What is the portfolio standard deviation if 35% of the portfolio is in Nervy and the two securities have a correlation of 0.6?

(Multiple Choice)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)