Exam 8: Risk, Return, and Portfolio Theory

Exam 1: An Introduction to Finance53 Questions

Exam 2: Business Corporate Finance68 Questions

Exam 3: Financial Statements49 Questions

Exam 4: Financial Statement Analysis and Forecasting90 Questions

Exam 5: Time Value of Money82 Questions

Exam 6: Bond Valuation and Interest Rates77 Questions

Exam 7: Equity Valuation101 Questions

Exam 8: Risk, Return, and Portfolio Theory111 Questions

Exam 9: The Capital Asset Pricing Model Capm115 Questions

Exam 10: Market Efficiency52 Questions

Exam 11: Forwards, Futures, and Swaps56 Questions

Exam 12: Options55 Questions

Exam 13: Capital Budgeting, Risk Considerations, and Other Special Issues149 Questions

Exam 14: Cash Flow Estimation and Capital Budgeting Decisions127 Questions

Exam 15: Mergers and Acquisitions88 Questions

Exam 16: Leasing34 Questions

Exam 17: Investment Banking and Securities Law68 Questions

Exam 18: Debt Instruments52 Questions

Exam 19: Equity and Hybrid Instruments67 Questions

Exam 20: Cost of Capital68 Questions

Exam 21: Capital Structure Decisions69 Questions

Exam 22: Dividend Policy53 Questions

Exam 23: Working Capital Management: General Issues51 Questions

Exam 24: Working Capital Management: Current Assets and Current Liabilities78 Questions

Select questions type

Suppose you own 100 shares of CyberChase Ltd.and 200 shares of NetSurfer Ltd.At the time of purchase, the stocks of CyberChase and NetSurfer were trading at $25 and $15 per share, respectively.What is the expected value of the portfolio if CyberChase has an expected return of 8.0% and NetSurfer has an expected return of 13.0%?

(Multiple Choice)

4.8/5  (31)

(31)

Given the following forecasts, what is the expected return for a portfolio that has $2,200 invested in Stock X, $3,600 in Stock Y, and $4,200 invested in Stock Z?

(Multiple Choice)

4.7/5 (37)

The expected return on Alpha Inc.is 8.0% and the expected return on Beta Inc.is 24.0%.What is the trade-off between investing in Alpha and Beta if the portfolio weight in Alpha is increased by 1%?

(Multiple Choice)

4.9/5 (36)

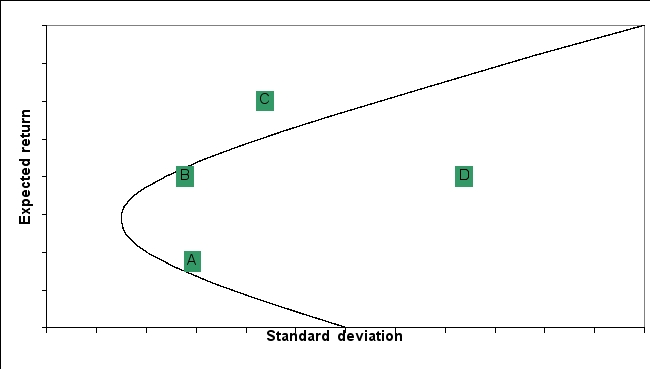

The standard deviation and expected returns for 4 portfolios (A, B, C, and D)are graphed on the following efficient frontier:  Which of the following portfolios are attainable?

Which of the following portfolios are attainable?

(Multiple Choice)

4.8/5 (38)

Which of the following is NOT a disadvantage of Value at Risk (VaR)?

(Multiple Choice)

4.9/5 (33)

Stocks A and B have a correlation coefficient of +1.If stock A went from $10 to $12 over the past month, what is the price of stock B, if its price one month ago was $5?

(Multiple Choice)

4.9/5 (39)

If the closing price of Stock Y was $38.63 on Friday, which was after it had earned daily returns of 8.0%, 23.0%, -30.0%, 20.0%, and -5.0% during the week (Monday to Friday), what was the opening price of Stock Y on Monday?

(Multiple Choice)

4.8/5 (39)

Use the following three statements to answer this question:

I.There will be benefits from diversification as long as  .

II.As long as

.

II.As long as  , an equally weighted portfolio would be risk-free.

III.Diversification can never eliminate the total risk of the portfolio.

, an equally weighted portfolio would be risk-free.

III.Diversification can never eliminate the total risk of the portfolio.

(Multiple Choice)

4.8/5 (28)

Define and discuss expected return with regard to individual securities and a portfolio as a whole.

(Essay)

4.9/5 (26)

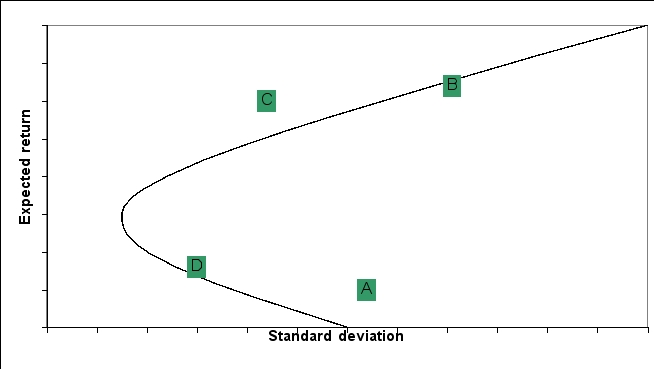

The standard deviation and expected returns for 4 portfolios (A, B, C, and D)are graphed on the following efficient frontier:  Which of the following portfolios are efficient?

Which of the following portfolios are efficient?

(Multiple Choice)

4.8/5 (37)

Which portfolio represents the minimum variance portfolio?

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)