Exam 8: Risk, Return, and Portfolio Theory

Exam 1: An Introduction to Finance53 Questions

Exam 2: Business Corporate Finance68 Questions

Exam 3: Financial Statements49 Questions

Exam 4: Financial Statement Analysis and Forecasting90 Questions

Exam 5: Time Value of Money82 Questions

Exam 6: Bond Valuation and Interest Rates77 Questions

Exam 7: Equity Valuation101 Questions

Exam 8: Risk, Return, and Portfolio Theory111 Questions

Exam 9: The Capital Asset Pricing Model Capm115 Questions

Exam 10: Market Efficiency52 Questions

Exam 11: Forwards, Futures, and Swaps56 Questions

Exam 12: Options55 Questions

Exam 13: Capital Budgeting, Risk Considerations, and Other Special Issues149 Questions

Exam 14: Cash Flow Estimation and Capital Budgeting Decisions127 Questions

Exam 15: Mergers and Acquisitions88 Questions

Exam 16: Leasing34 Questions

Exam 17: Investment Banking and Securities Law68 Questions

Exam 18: Debt Instruments52 Questions

Exam 19: Equity and Hybrid Instruments67 Questions

Exam 20: Cost of Capital68 Questions

Exam 21: Capital Structure Decisions69 Questions

Exam 22: Dividend Policy53 Questions

Exam 23: Working Capital Management: General Issues51 Questions

Exam 24: Working Capital Management: Current Assets and Current Liabilities78 Questions

Select questions type

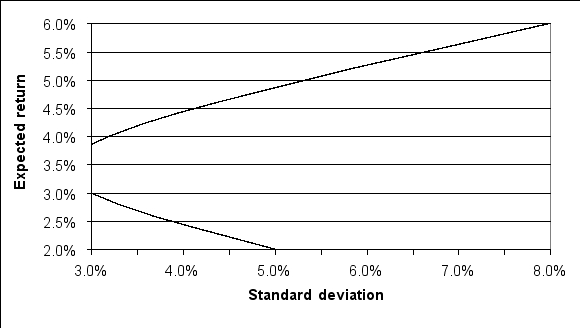

For the following efficient frontier, the standard deviation of the minimum variance portfolio is:

(Multiple Choice)

4.8/5  (33)

(33)

Given the following forecasts, what is the correlation between securities X and Y?

(Multiple Choice)

4.8/5 (35)

The geometric average quarterly return of ROM Company was 5.0% for the previous year.What was the return for the third quarter if the returns for the first, second, and fourth quarters were 10.0%, -9.05%, and 8.0%, respectively?

(Multiple Choice)

4.8/5 (35)

Use the following two statements to answer this question:

I.Risk is the possibility of incurring harm.

II.Ex post returns are expected returns while ex ante returns are future returns.

(Multiple Choice)

4.7/5 (38)

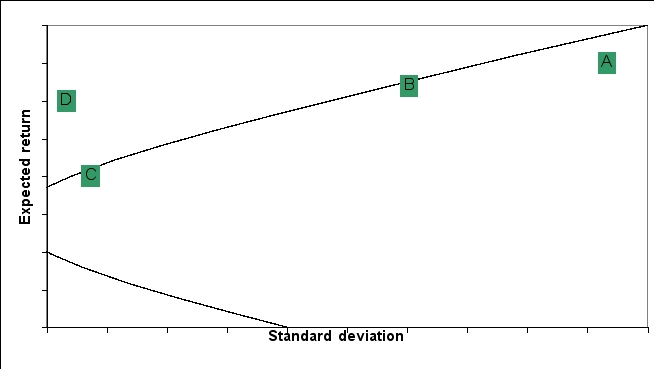

The standard deviation and expected returns for 4 portfolios (A, B, C, and D)are graphed on the following efficient frontier:  Which of the following portfolios (or combinations)are likely to be preferred by a risk-averse investor? Which of the following portfolios (or combinations)are likely to be preferred by a risk-loving investor? Explain your reasoning.

Which of the following portfolios (or combinations)are likely to be preferred by a risk-averse investor? Which of the following portfolios (or combinations)are likely to be preferred by a risk-loving investor? Explain your reasoning.

(Essay)

4.9/5 (44)

AMC Corp had a geometric weekly return of 5.0% for this past week.The daily returns for Monday through Thursday are 4.0%, 3.0%, -7.0%, and 9.0%, respectively.If AMC's stock traded at $16.22 when the market closed on Friday, what is the opening price of the stock on Friday?

(Multiple Choice)

4.9/5 (50)

Suppose you plan to create a portfolio with three securities: Dizzy (D), Lazy (L), and Crazy (C).The expected returns for Dizzy, Lazy and Crazy are 6.0%, 8.0%, and 10.0%, respectively.The standard deviation is 9.0% for Dizzy, 15.0% for Lazy, and 12.0% for Crazy.The correlation coefficients among the returns for the three securities are: CORRDL= 0.6, CORRDC = -0.3, and CORRLC = 0.4.What is the portfolio standard deviation if 30.0% of the portfolio is in Dizzy and 10.0% is in Lazy?

(Multiple Choice)

4.8/5 (42)

Laura purchased a share of MVP Company for $26.43 one year ago.The stock paid a quarterly dividend of $0.50 during the year.What is the capital gain yield if the current stock price is $28.26?

(Multiple Choice)

5.0/5 (42)

Your portfolio that has $500 invested in Stock A and $1,500 invested in Stock B.If the expected returns on Stock A and Stock B are 7% and 23%, respectively, what is the portfolio return?

(Multiple Choice)

4.9/5 (42)

What is the expected return from an investment that has an equally likely probability to lose half of the investment or double the investment?

(Multiple Choice)

4.9/5 (41)

You have been given the following forecasts for the economy and Stock A: (1)the probability of having a recession next year is 30.0%, a normal economy is 55.0%, and an expansion is 15.0%, and (2)the price of Stock A will be $9 if the economy is in recession, $15 if the economy is normal, and $18 if the economy is in expansion.What is the ex ante variance of Stock A's returns if it is currently selling for $12?

(Multiple Choice)

4.8/5 (38)

Suppose you plan to create a portfolio with two securities: Tobin and Bino, with weights to be greater than or equal to zero.The expected return of Tobin is 10 percent with a standard deviation of 12 percent.The expected return of Bino is 16 percent with a standard deviation of 20 percent.The correlation between the two securities is 0.30.

a)What percentage of your investment should be invested in Tobin to obtain a portfolio standard deviation of 12.2638 percent?

b)What is the expected return of the portfolio?

(Essay)

4.9/5 (35)

What is the expected return for a portfolio that has $800 invested in Stock A and $1,200 invested in Stock B, if the expected returns on Stock A and Stock B are 10% and 18%, respectively?

(Multiple Choice)

4.8/5 (34)

Suppose you are given the following forecasts for the economy and for Sneezy Company at the beginning of the year:

During the year, you observed the following:

During the year, you observed the following:

a)Calculate the ex-ante expected return

b)Calculate the ex-ante standard deviation of returns

c)Calculate the ex-post average return

d)Calculate the ex-post standard deviation of returns

a)Calculate the ex-ante expected return

b)Calculate the ex-ante standard deviation of returns

c)Calculate the ex-post average return

d)Calculate the ex-post standard deviation of returns

(Essay)

4.8/5 (42)

The expected returns for Bumpy Inc.and Bouncy Inc.are 20.0% and 8.0%, respectively.The standard deviation is 35.0% for Bumpy and 16.0% for Bouncy.What is the portfolio standard deviation if 45.0% of the portfolio is in Bumpy and the two securities have perfect negative correlation?

(Multiple Choice)

4.7/5 (44)

Cinderella plans to form a portfolio with two securities: Jaq and Gus.The correlation between the two securities is -1.Given the following forecasts, what are the weights in Jaq and Gus that will set the standard deviation of the portfolio equal to zero?

(Multiple Choice)

4.9/5 (30)

Richards & Co.Analysts has recently published a study claiming that the benefits to diversification are constant.In other words, adding one more stock to a three stock portfolio will have the same impact as adding one more stock to a 500‐stock portfolio.You are not convinced and you decide to evaluate the claim.

a .Assume that all the stocks have the same standard deviation, 10.0%, and all are independent (correlation equals 0.0).Create equally weighted portfolios of 1 to 10 stocks and calculate the standard deviation for each portfolio.Graph the portfolio standard deviation as a function of the number of stocks.Based on the results of your analysis, evaluate the Richard & Co.Analysts ' claim.

b .As the number of firms increases, what do you expect will happen to the risk of the portfolio? Can the risk of the portfolio come close to zero?

(Essay)

4.8/5 (42)

Which of the following is not a method of estimating Value at Risk (VaR)?

(Multiple Choice)

5.0/5 (40)

Given the following forecasts, what is the covariance of the returns on securities A and B?

(Multiple Choice)

4.7/5 (47)

Given the following forecasts, what is the standard deviation of returns?

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)