Exam 15: Monopolistic Competition and Product Differentiation

Exam 1: First Principles233 Questions

Exam 2: Economic Models: Trade-Offs and Trade 25382 Questions

Exam 3: Supply and Demand290 Questions

Exam 4: Consumer and Producer Surplus224 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets227 Questions

Exam 6: Elasticity300 Questions

Exam 7: Taxes298 Questions

Exam 8: International Trade272 Questions

Exam 9: Decision Making by Individuals Firms201 Questions

Exam 10: The Rational Consumer372 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs362 Questions

Exam 12: Perfect Competition and the Supply Curve355 Questions

Exam 13: Monopoly350 Questions

Exam 14: Oligopoly294 Questions

Exam 15: Monopolistic Competition and Product Differentiation262 Questions

Exam 16: Externalities199 Questions

Exam 17: Public Goods Common Resources224 Questions

Exam 18: The Economics of the Welfare140 Questions

Exam 19: Factor Markets and the Distribution of Income369 Questions

Exam 20: Uncertainty, Risk, and Private Information202 Questions

Select questions type

In long-run equilibrium in perfect competition, marginal cost is:

(Multiple Choice)

4.7/5  (36)

(36)

A firm operating in a monopolistically competitive market is producing a quantity at which MC = MR. Profit:

(Multiple Choice)

4.9/5 (32)

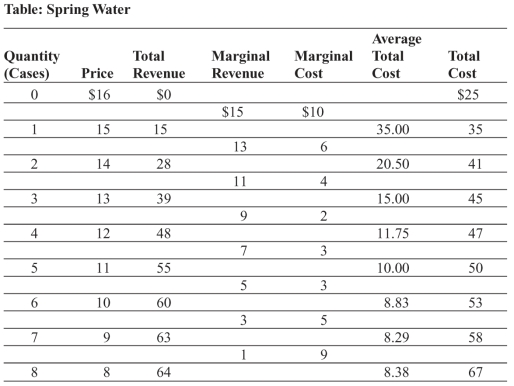

Use the following to answer questions:  -(Table: Spring Water) The table Spring Water shows the demand and cost data for a firm in a monopolistically competitive industry producing drinking water from underground springs. The profit-maximizing output is _____ cases.

-(Table: Spring Water) The table Spring Water shows the demand and cost data for a firm in a monopolistically competitive industry producing drinking water from underground springs. The profit-maximizing output is _____ cases.

(Multiple Choice)

4.7/5 (33)

Which of the following is TRUE of firms in both perfect competition and monopolistic competition?

(Multiple Choice)

4.9/5 (37)

Why are some rational consumers willing to pay more for a bottle of Advil than for a bottle of generic ibuprofen tablets, when ibuprofen is the active ingredient in Advil?

(Essay)

4.9/5 (43)

Use the following to answer questions:

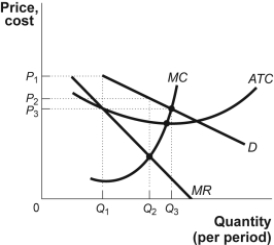

Figure: The Market for Gas Stations  -(Figure: The Market for Gas Stations) Look at the figure The Market for Gas Stations. This market is characterized by many firms, differentiated products, easy entry, and easy exit. In long-run equilibrium, the economic profit earned by the typical gas station will be:

-(Figure: The Market for Gas Stations) Look at the figure The Market for Gas Stations. This market is characterized by many firms, differentiated products, easy entry, and easy exit. In long-run equilibrium, the economic profit earned by the typical gas station will be:

(Multiple Choice)

5.0/5 (44)

To maximize profit, a monopolistically competitive firm should produce the level of output at which:

(Multiple Choice)

4.8/5 (36)

An industry with a few interdependent firms is best described as an example of:

(Multiple Choice)

4.9/5 (43)

The market for soft drinks, which is dominated by Coca Cola and Pepsi, is best considered to be an example of:

(Multiple Choice)

4.8/5 (28)

In many cities you can stay at a Holiday Inn in the downtown area, in a suburban community, or near the airport. These Holiday Inn establishments are examples of product differentiation by:

(Multiple Choice)

4.8/5 (44)

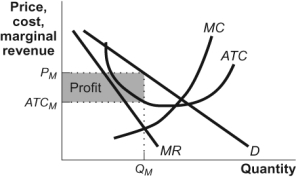

Use the following to answer questions:

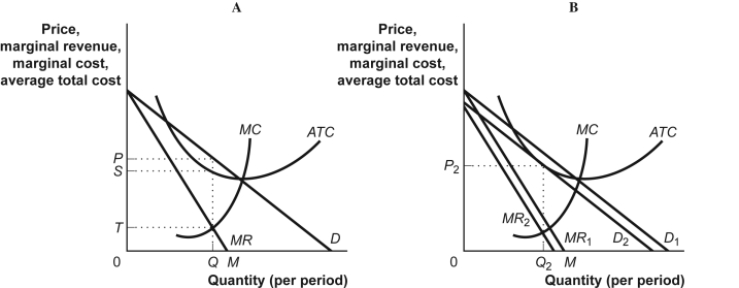

Figure: Profit Maximization in Monopolistic Competition  -(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit Maximization in Monopolistic Competition. A firm in monopolistic competition will maximize profits by producing so that:

-(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit Maximization in Monopolistic Competition. A firm in monopolistic competition will maximize profits by producing so that:

(Multiple Choice)

4.9/5 (40)

As product differentiation increases, the price elasticity of demand falls and the firm increases its market power.

(True/False)

4.9/5 (38)

Use the following to answer questions:

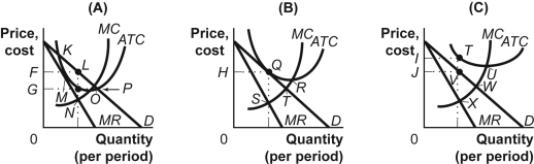

Figure: Firms in Monopolistic Competition  -(Figure: Firms in Monopolistic Competition) In panel (C) of the figure Firms in Monopolistic Competition, the profit-maximizing quantity of output is determined by the intersection at point:

-(Figure: Firms in Monopolistic Competition) In panel (C) of the figure Firms in Monopolistic Competition, the profit-maximizing quantity of output is determined by the intersection at point:

(Multiple Choice)

4.8/5 (30)

Firms in monopolistic competition can acquire some market power by:

(Multiple Choice)

4.7/5 (41)

Monopolistic competition describes an industry characterized by:

(Multiple Choice)

4.9/5 (42)

Use the following to answer questions:

Figure: Monopolistic Competition V  -(Figure: Monopolistic Competition V) The figure Monopolistic Competition V illustrates a firm in the _____; in the _____, the demand and marginal revenue curves will shift to the _____.

-(Figure: Monopolistic Competition V) The figure Monopolistic Competition V illustrates a firm in the _____; in the _____, the demand and marginal revenue curves will shift to the _____.

(Multiple Choice)

4.8/5 (31)

In a long-run equilibrium, firms in a monopolistically competitive industry sell at a price:

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)