Exam 15: Monopolistic Competition and Product Differentiation

Exam 1: First Principles233 Questions

Exam 2: Economic Models: Trade-Offs and Trade 25382 Questions

Exam 3: Supply and Demand290 Questions

Exam 4: Consumer and Producer Surplus224 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets227 Questions

Exam 6: Elasticity300 Questions

Exam 7: Taxes298 Questions

Exam 8: International Trade272 Questions

Exam 9: Decision Making by Individuals Firms201 Questions

Exam 10: The Rational Consumer372 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs362 Questions

Exam 12: Perfect Competition and the Supply Curve355 Questions

Exam 13: Monopoly350 Questions

Exam 14: Oligopoly294 Questions

Exam 15: Monopolistic Competition and Product Differentiation262 Questions

Exam 16: Externalities199 Questions

Exam 17: Public Goods Common Resources224 Questions

Exam 18: The Economics of the Welfare140 Questions

Exam 19: Factor Markets and the Distribution of Income369 Questions

Exam 20: Uncertainty, Risk, and Private Information202 Questions

Select questions type

Use the following to answer questions:

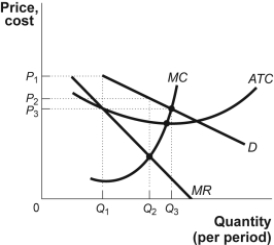

Figure: The Market for Gas Stations  -(Figure: The Market for Gas Stations) The figure The Market for Gas Stations shows curves facing a typical gas station in a large town. The market is characterized by many firms, differentiated products, easy entry, and easy exit. If the gas station here is typical, prices charged by firms in the market are likely to:

-(Figure: The Market for Gas Stations) The figure The Market for Gas Stations shows curves facing a typical gas station in a large town. The market is characterized by many firms, differentiated products, easy entry, and easy exit. If the gas station here is typical, prices charged by firms in the market are likely to:

(Multiple Choice)

4.7/5  (32)

(32)

If a firm operating in monopolistic competition is producing a quantity that generates MC > MR, then the marginal decision rule tells us that profit:

(Multiple Choice)

4.8/5 (32)

The model of monopolistic competition characterizes the market for plumbing services in a city. Suppose that the market is in long-run equilibrium. For a typical plumbing firm, price:

(Multiple Choice)

4.8/5 (30)

The restaurant industry is characterized by excess capacity. This means that:

(Multiple Choice)

4.9/5 (31)

Use the following to answer questions:

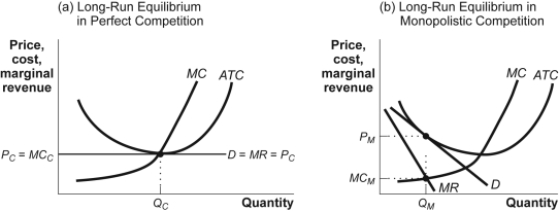

Figure: Comparing Long-Run Equilibriums  -(Figure: Comparing Long-Run Equilibriums) In the figure Comparing Long-Run Equilibriums, which of the following statements is FALSE?

-(Figure: Comparing Long-Run Equilibriums) In the figure Comparing Long-Run Equilibriums, which of the following statements is FALSE?

(Multiple Choice)

4.9/5 (40)

Use the following to answer questions:

Scenario: Monopolistically Competitive Firm

For a monopolistically competitive firm, Q = 160 - P; MC = 20 + 2Q; and TC = 20Q + Q2 + 20.

-(Scenario: Monopolistically Competitive Firm) Given the information in the scenario Monopolistically Competitive Firm, in the long run, this firm can expect that:

(Multiple Choice)

4.9/5 (31)

The excess capacity in monopolistic competition may be viewed as:

(Multiple Choice)

4.7/5 (33)

Monopolistic competition describes an industry characterized by a _____ number of firms producing _____ products with _____ entry.

(Multiple Choice)

5.0/5 (41)

If a monopolistically competitive firm is in long-run equilibrium, price:

(Multiple Choice)

4.8/5 (35)

The best way for firms in monopolistic competition to gain market power is to engage in tacit collusion.

(True/False)

4.8/5 (34)

The fact that firms in a monopolistically competitive industry are competing for a limited market is called competition among sellers.

(True/False)

4.8/5 (46)

Use the following to answer questions:

Figure: Comparing Long-Run Equilibriums

-(Figure: Comparing Long-Run Equilibriums) Look at the figure Comparing Long-Run Equilibriums. Which of the following statements is FALSE?

(Multiple Choice)

4.7/5 (41)

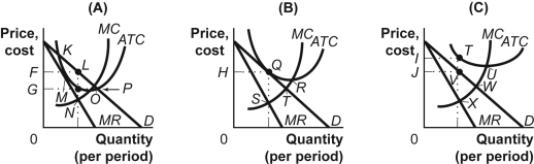

Use the following to answer questions:

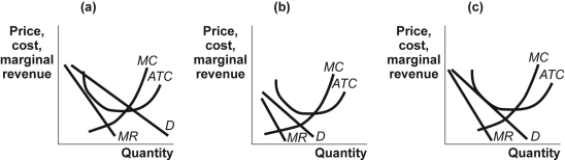

Figure: Monopolistic Competition II  -(Figure: Monopolistic Competition II) Which of the panels in the figure Monopolistic Competition II shows a monopolistic competitor earning a profit in the short run?

-(Figure: Monopolistic Competition II) Which of the panels in the figure Monopolistic Competition II shows a monopolistic competitor earning a profit in the short run?

(Multiple Choice)

4.8/5 (41)

Use the following to answer question:

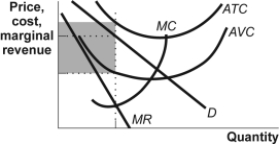

Figure: Monopolistic Competition  -(Figure: Monopolistic Competition) The firm in the figure Monopolistic Competition is producing at the output level that maximizes profits (minimizes losses). The shaded rectangle depicts the level of:

-(Figure: Monopolistic Competition) The firm in the figure Monopolistic Competition is producing at the output level that maximizes profits (minimizes losses). The shaded rectangle depicts the level of:

(Multiple Choice)

4.9/5 (35)

Consider the demand curve for a firm in perfect competition, a firm in monopolistic competition, and a monopolist. Which is likely to be the least elastic and which is likely to be the most elastic? Explain.

(Essay)

4.8/5 (43)

Gas stations are not monopolistically competitive, because everyone knows the gasoline is the same regardless of where it is purchased.

(True/False)

4.8/5 (37)

Use the following to answer questions:

Figure: Firms in Monopolistic Competition  -(Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic Competition. There will be a negative economic profit (or an economic loss) earned at the profit-maximizing price _____ in panel _____.

-(Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic Competition. There will be a negative economic profit (or an economic loss) earned at the profit-maximizing price _____ in panel _____.

(Multiple Choice)

4.8/5 (40)

A firm in monopolistic competition maximizes its profit by producing so that:

(Multiple Choice)

4.8/5 (38)

Which industry type, perfect competition or monopolistic competition, produces less deadweight loss? Which industry type is preferred by society? Explain.

(Essay)

4.7/5 (41)

If the Boston doughnut market is monopolistically competitive and the firms are earning short-run profits, consumers in Boston will see less diversity in the doughnuts offered over time.

(True/False)

5.0/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)