Exam 12: An Alternative View of Risk and Return: the Arbitrage Pricing Theory

Exam 1: Introduction to Corporate Finance38 Questions

Exam 2: Accounting Statements and Cash Flow59 Questions

Exam 3: Financial Planning and Growth39 Questions

Exam 4: Financial Markets and Net Present Value: First Principles of Finance36 Questions

Exam 5: The Time Value of Money73 Questions

Exam 6: How to Value Bonds and Stocks81 Questions

Exam 7: Net Present Value and Other Investment Rules57 Questions

Exam 8: Net Present Value and Capital Budgeting48 Questions

Exam 9: Risk Analysis, Real Options, and Capital Budgeting35 Questions

Exam 10: Risk and Return: Lessons From Market History51 Questions

Exam 11: Risk and Return: the Capital Asset Pricing Model65 Questions

Exam 12: An Alternative View of Risk and Return: the Arbitrage Pricing Theory42 Questions

Exam 13: Risk, Return, and Capital Budgeting63 Questions

Exam 14: Corporate Financing Decisions and Efficient Capital Markets46 Questions

Exam 15: Long-Term Financing: an Introduction46 Questions

Exam 16: Capital Structure: Basic Concepts56 Questions

Exam 17: Capital Structure: Limits to the Use of Debt53 Questions

Exam 18: Valuation and Capital Budgeting for the Levered Firm54 Questions

Exam 19: Dividends and Other Payouts47 Questions

Exam 20: Issuing Equity Securities to the Public43 Questions

Exam 21: Long-Term Debt50 Questions

Exam 22: Leasing42 Questions

Exam 23: Options and Corporate Finance: Basic Concepts63 Questions

Exam 24: Options and Corporate Finance: Extensions and Applications24 Questions

Exam 25: Warrants and Convertibles47 Questions

Exam 26: Derivatives and Hedging Risk50 Questions

Exam 27: Short-Term Finance and Planning51 Questions

Exam 28: Cash Management35 Questions

Exam 29: Credit Management31 Questions

Exam 30: Mergers and Acquisitions55 Questions

Exam 31: Financial Distress22 Questions

Exam 32: International Corporate Finance54 Questions

Select questions type

To estimate the required return for a security using APT or CAPM, it is necessary to have:

Free

(Multiple Choice)

4.9/5  (35)

(35)

Correct Answer: Verified

Verified

C

An advantage of the APT over CAPM is:

Free

(Multiple Choice)

4.8/5 (45)

Correct Answer:Verified

D

If company A makes a new product discovery and their stock rises 5% this will have:

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

B

Explain the conceptual differences in the theoretical development of the CAPM and APT.

(Essay)

4.7/5 (38)

You have a 3 factor model to explain returns. Explain what a factor represents in the context of the APT? Each factor is multiplied by a what do these represent and how do they relate to the actual return?

(Essay)

4.8/5 (41)

Assume that the single factor APT model applies and a portfolio exists such that 2/3 of the funds are invested in Security Q and the rest in the risk-free asset. Security Q has a beta of 1.5. The portfolio has a beta of:

(Multiple Choice)

4.8/5 (31)

The betas along with the factors in the APT adjust the expected return for:

(Multiple Choice)

4.9/5 (42)

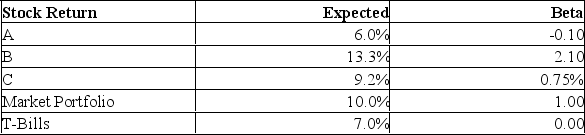

An investor is considering the three stocks given below:

C. Demonstrate that holding stock A actually reduces risk by comparing the risk of a portfolio equally weighted between stock B and T-Bills with a portfolio equally weighted between stock B and

A.

Stock B and C: Rp = .5(13.3%) + .5(9.2%) = 11.25%

Stock B and C: p = .5(2.1) + .5(0.75) = 1.425

Stock B and T-bills: B&TBILL = .5(2.1) + .5(0) = 1.05

Stock's B and A: B&A = .5(2.1) + .5(-0.1) = 1.00

C. Demonstrate that holding stock A actually reduces risk by comparing the risk of a portfolio equally weighted between stock B and T-Bills with a portfolio equally weighted between stock B and

A.

Stock B and C: Rp = .5(13.3%) + .5(9.2%) = 11.25%

Stock B and C: p = .5(2.1) + .5(0.75) = 1.425

Stock B and T-bills: B&TBILL = .5(2.1) + .5(0) = 1.05

Stock's B and A: B&A = .5(2.1) + .5(-0.1) = 1.00

(Essay)

4.8/5 (34)

Suppose the JumpStart Corporation's common stock has a beta of 0.8. If the risk-free rate is 4% and the expected market return is 9%, the expected return for JumpStart's common stock is:

(Multiple Choice)

4.9/5 (42)

Based on a multi-factor APT model, the concept of portfolio diversification is to minimize which one of the following?

(Multiple Choice)

4.9/5 (37)

Identify at least two accounting measures that are used in empirical asset pricing models and explain how these measures can be used to identify assets that are expected to have higher returns in the future.

(Essay)

4.9/5 (43)

Suppose that we have identified three important systematic risk factors given by exports, inflation, and industrial production. In the beginning of the year, growth in these three factors is estimated at -1%, 2.5%, and 3.5% respectively. However, actual growth in these factors turns out to be 1%, -2%, and 2%. The factor betas are given by EX = 1.8, I = 0.7, and IP = 1.0. What would the stock's total return be if the actual growth in each of the factors was equal to growth expected? Assume no unexpected news on the patent. Assume expected return on the stock is 6%.

(Multiple Choice)

4.8/5 (40)

Financial models used to describe returns are based either on a theoretical construct or parametric methods. Parametric models rely on:

(Multiple Choice)

4.9/5 (34)

In the One Factor (APT) Model, the characteristic line to estimate i passes through the origin, unlike the estimate used in the CAPM because:

(Multiple Choice)

4.8/5 (34)

If the expected rate of inflation was 3% and the actual rate was 6.2%; the systematic response coefficient from inflation, I, would result in a change in any security return of:

(Multiple Choice)

4.8/5 (36)

A security that has a beta of zero will have an expected return of:

(Multiple Choice)

4.8/5 (29)

Assuming that the single factor APT model applies, the beta for the market portfolio is:

(Multiple Choice)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)