Exam 11: Risk and Return: the Capital Asset Pricing Model

Exam 1: Introduction to Corporate Finance38 Questions

Exam 2: Accounting Statements and Cash Flow59 Questions

Exam 3: Financial Planning and Growth39 Questions

Exam 4: Financial Markets and Net Present Value: First Principles of Finance36 Questions

Exam 5: The Time Value of Money73 Questions

Exam 6: How to Value Bonds and Stocks81 Questions

Exam 7: Net Present Value and Other Investment Rules57 Questions

Exam 8: Net Present Value and Capital Budgeting48 Questions

Exam 9: Risk Analysis, Real Options, and Capital Budgeting35 Questions

Exam 10: Risk and Return: Lessons From Market History51 Questions

Exam 11: Risk and Return: the Capital Asset Pricing Model65 Questions

Exam 12: An Alternative View of Risk and Return: the Arbitrage Pricing Theory42 Questions

Exam 13: Risk, Return, and Capital Budgeting63 Questions

Exam 14: Corporate Financing Decisions and Efficient Capital Markets46 Questions

Exam 15: Long-Term Financing: an Introduction46 Questions

Exam 16: Capital Structure: Basic Concepts56 Questions

Exam 17: Capital Structure: Limits to the Use of Debt53 Questions

Exam 18: Valuation and Capital Budgeting for the Levered Firm54 Questions

Exam 19: Dividends and Other Payouts47 Questions

Exam 20: Issuing Equity Securities to the Public43 Questions

Exam 21: Long-Term Debt50 Questions

Exam 22: Leasing42 Questions

Exam 23: Options and Corporate Finance: Basic Concepts63 Questions

Exam 24: Options and Corporate Finance: Extensions and Applications24 Questions

Exam 25: Warrants and Convertibles47 Questions

Exam 26: Derivatives and Hedging Risk50 Questions

Exam 27: Short-Term Finance and Planning51 Questions

Exam 28: Cash Management35 Questions

Exam 29: Credit Management31 Questions

Exam 30: Mergers and Acquisitions55 Questions

Exam 31: Financial Distress22 Questions

Exam 32: International Corporate Finance54 Questions

Select questions type

A stock with a beta of zero would be expected to:

Free

(Multiple Choice)

4.9/5  (34)

(34)

Correct Answer: Verified

Verified

A

Covariance measures the interrelationship between two securities in terms of:

Free

(Multiple Choice)

4.8/5 (25)

Correct Answer:Verified

B

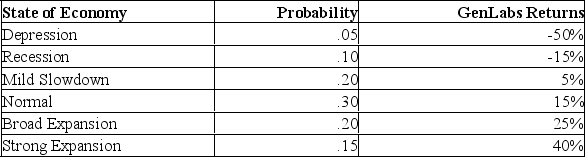

GenLabs has been a hot stock the last few years, but is risky. The expected returns for GenLabs are highly dependent on the state of the economy as follows:  The variance and standard deviation of GenLabs returns are:

The variance and standard deviation of GenLabs returns are:

Free

(Multiple Choice)

4.9/5 (31)

Correct Answer:Verified

A

The dominant portfolio with the lowest possible risk measures is:

(Multiple Choice)

4.8/5 (37)

A portfolio is entirely invested into Buzz's Bauxite Boring Equity, which is expected to return 16%, and Zum's Inc. bonds, which are expected to return 8%. Sixty percent of the funds are invested in Buzz's and the rest in Zum's. What is the expected return on the portfolio?

(Multiple Choice)

4.9/5 (37)

If the covariance of stock 1 with stock 2 is -.0065, then what is the covariance of stock 2 with stock 1?

(Multiple Choice)

4.9/5 (33)

The total number of variance and covariance terms in portfolio is N2. How many of these would be (including non-unique) covariances?

(Multiple Choice)

4.9/5 (35)

Why are some risks diversifiable and some nondiversifiable? Give an example of each.

(Essay)

4.8/5 (41)

According to the CAPM, the expected return on a risky asset depends on three components. Describe each component, and explain its role in determining expected return.

(Essay)

4.9/5 (35)

You want your portfolio beta to be 1.20. Currently, your portfolio consists of $100 invested in stock A with a beta of 1.4 and $300 in stock B with a beta of.6. You have another $400 to invest and want to divide it between an asset with a beta of 1.6 and a risk-free asset. How much should you invest in the risk-free asset?

(Multiple Choice)

4.9/5 (39)

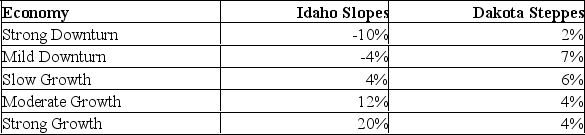

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  If IS and DS are combined in a portfolio with 50% invested in each, the expected return and risk would be:

If IS and DS are combined in a portfolio with 50% invested in each, the expected return and risk would be:

(Multiple Choice)

4.8/5 (42)

A portfolio exists containing stocks D, E, and F held in proportions 30%, 40%, and 30% respectively. The expected returns on the three stocks are given by 12%, 20%, and 28% respectively. Calculate the portfolio's expected return.

(Essay)

4.9/5 (36)

When many assets are included in a portfolio or index the risk of the portfolio or index will be:

(Multiple Choice)

4.8/5 (41)

We routinely assume that investors are risk-averse return-seekers; i.e., they like returns and dislike risk. If so, why do we contend that only systematic risk and not total risk is important?

(Essay)

4.9/5 (42)

When stocks with the same expected return are combined into a portfolio:

(Multiple Choice)

4.9/5 (38)

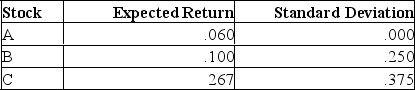

Given the following information on three stocks:

= -.05333

bc

Suppose you desire to invest in any one of the stocks listed above. Can any be recommended?

= -.05333

bc

Suppose you desire to invest in any one of the stocks listed above. Can any be recommended?

(Essay)

4.8/5 (37)

Suppose the MiniCD Corporation's common stock has a return of 12%. Assume the risk-free rate is 4%, the expected market return is 9%, and no unsystematic influence affected Mini's return. The beta for MiniCD is:

(Multiple Choice)

4.9/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)