Exam 13: Liability-Driven and Index-Based Strategies

The following information relates to Questions

Chaopraya av is an investment advisor for high-net-worth individuals. one of her clients,Schuylkill Cy, plans to fund her grandson's college education and considers two options:

option 1 Contribute a lump sum of $300,000 in 10 years.

option 2 Contribute four level annual payments of $76,500 starting in 10 years.The grandson will start college in 10 years. Cy seeks to immunize the contribution today.For option 1, av calculates the present value of the $300,000 as $234,535. to immunize the future single outflow, av considers three bond portfolios given that no zero-coupon govern- ment bonds are available. The three portfolios consist of non-callable, fixed-rate, coupon-bearing government bonds considered free of default risk. av prepares a comparative analysis of the three portfolios, presented in exhibit 1.

EXHIBIT 1 Results of Comparative Analysis of Potential Portfolios Portfolio A Portfolio B Portfolio C Market value \ 235,727 \ 233,428 \ 235,306 Cash flow yield 2.504\% 2.506\% 2.502\% Macaulay duration 9.998 10.002 9.503 Convexity 119.055 121.498 108.091

av evaluates the three bond portfolios and selects one to recommend to Cy.

-Determine the most appropriate immunization portfolio in exhibit 2. Justify your decision.

(circle one) Justify your decision. Portfolio 1 Portfolio 2 Portfolio 3

after selecting a portfolio to immunize Cy's multiple future outflows, av prepares a report on how this immunization strategy would respond to various interest rate scenarios. The sce-nario analysis is presented in exhibit 3. EXHIBIT 3 Projected Portfolio Response to Interest Rate Scenarios Immunizing Portfolio Outflow Portfolio Difference Upward parallel shift \Delta Market value -6,410 -6,427 18 \Delta Cash flow yield 0.250\% 0.250\% 0.000\% \Delta Portfolio BPV -9 -8 -1 Downwardparallel shift \Delta Market value 6,626 6,622 4 Immunizing Portfolio Outflow Portfolio Difference \Delta Cash flow yield -0.250\% -0.250\% 0.000\% \Delta Portfolio BPV 9 8 1 Steepening twist \Delta Market value -1,912 347 -2,259 \Delta Cash flow yield 0.074\% -0.013\% 0.087\% \Delta Portfolio BPV -3 0 -3 Flattening twist \Delta Market value 1,966 -343 2,309 \Delta Cash flow yield -0.075\% 0.013\% -0.088\% \Delta Portfolio BPV 3 0 3

Money Duration: Money durations of all three possible immunizing portfolios match or closely match the money duration of the outflow portfolio. Matching

money durations is useful because the market values and cash flow yields of theimmunizing portfolio and the outflow portfolio are not necessarily equal."

"2. convexity: given that the money duration requirement is met by all three

possible immunizing portfolios, the portfolio with the lowest convexity that

is above the outflow portfolio's convexity of 135.142 should be selected. The

dispersion, as measured by convexity, of the immunizing portfolio should be aslow as possible subject to being greater than or equal to the dispersion of the

outflow portfolio. This will minimize the effect of non-parallel shifts in the yield curve. Portfolio 3's convexity of 132.865 is less than the outflow portfolio's con-vexity, so Portfolio 3 is not appropriate. both Portfolio 1 and Portfolio 2 have convexities that exceed the convexity of the outflow portfolio, but Portfolio 2'sconvexity of 139.851 is lower than Portfolio 1's convexity of 147.640. There-fore, Portfolio 2 is the most appropriate immunizing portfolio.

The immunizing portfolio needs to be greater than the convexity (and dispersion)of the outflow portfolio. but, the convexity of the immunizing portfolio should be minimized in order to minimize dispersion and reduce structural risk."

The following information relates to Questions

Doug Kepler, the newly hired chief financial officer for the City of radford, asks the dep-uty financial manager, hui ng, to prepare an analysis of the current investment portfolio and the city's current and future obligations. The city has multiple liabilities of different amounts and maturities relating to the pension fund, infrastructure repairs, and various other obligations. ng observes that the current fixed-income portfolio is structured to match the duration of each liability. Previously, this structure caused the city to access a line of credit for temporary mismatches resulting from changes in the term structure of interest rates.

Kepler asks ng for different strategies to manage the interest rate risk of the city's fixed-income investment portfolio against one-time shifts in the yield curve. ng considers two different strategies:

Strategy 1: immunization of the single liabilities using zero-coupon bonds held to maturity.

Strategy 2: immunization of the single liabilities using coupon-bearing bonds while continuously matching duration. The city also manages a separate, smaller bond portfolio for the radford School District. During the next five years, the school district has obligations for school expansions and ren- ovations. The funds needed for those obligations are invested in the loomberg barclays US aggregate index. Kepler asks ng which portfolio management strategy would be most efficient in mimicking this index.

a radford School board member has stated that she prefers a bond portfolio structure that provides diversification over time, as well as liquidity. in addressing the board member's

inquiry, ng examines a bullet portfolio, a barbell portfolio, and a laddered portfolio.

-ng's response to Kepler's question about the most efficient portfolio management strategy should be:

C

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

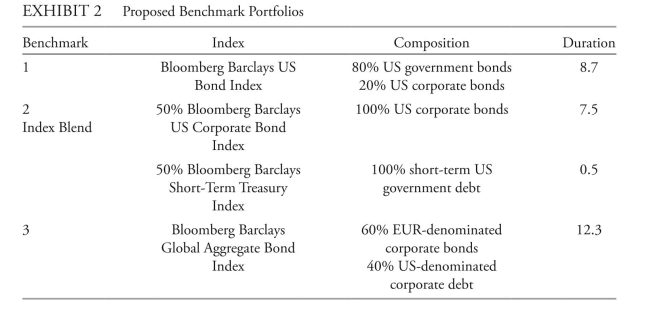

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-The investment process followed by DFC's previous fixed-income manager is best described as:

-The investment process followed by DFC's previous fixed-income manager is best described as:

C

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-Which of the portfolios in exhibit 1 best minimizes the structural risk to a single-liability immunization strategy?

The following information relates to Questions

Serena Soto is a risk management specialist with Liability Protection advisors. trey hudgens, CFo of Kiest Manufacturing, enlists Soto's help with three projects. The first project is to defease some of Kiest's existing fixed-rate bonds that are maturing in each of the next three years. The bonds have no call or put provisions and pay interest annually. exhibit 1 presents the payment schedule for the bonds.

EXHIBIT 1 Kiest Manufacturing Bond Payment Schedule as of 1 October 2017

Maturity Date Payment Amount 1 October 2018 \ 9,572,000 1 October 2019 \ 8,392,000 1 October 2020 \ 8,200,000

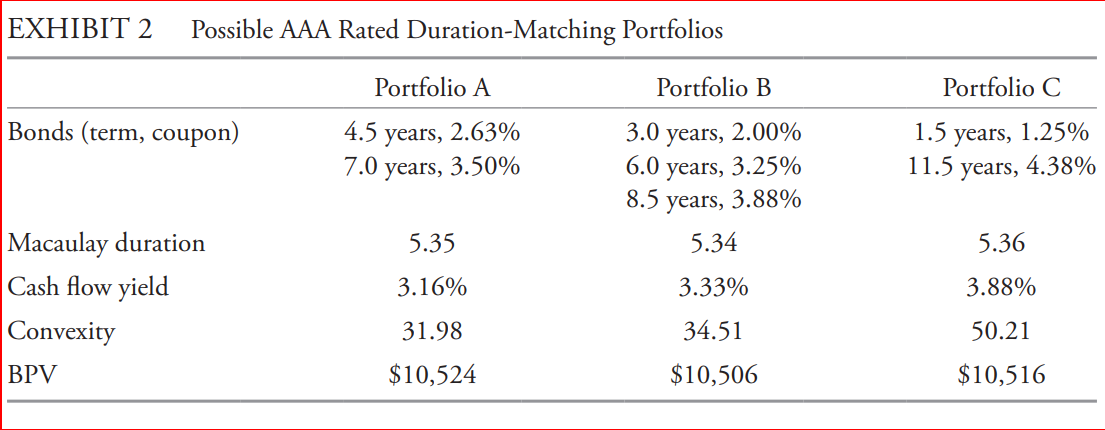

The second project for Soto is to help hudgens immunize a $20 million portfolio of liabilities. The liabilities range from 3.00 years to 8.50 years with a Macaulay duration of 5.34 years, cash flow yield of 3.25%, portfolio convexity of 33.05, and basis point value (bPv) of $10,505. Soto suggested employing a duration-matching strategy using one of the three aaa rated bond portfolios presented in exhibit 2.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

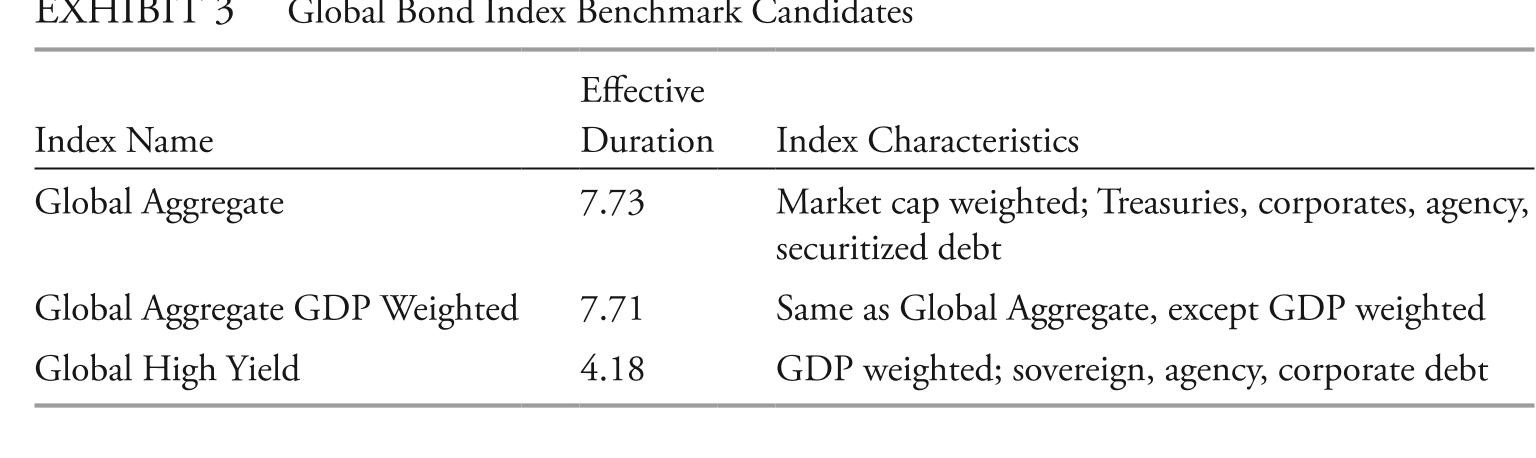

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs), and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-Soto's three assumptions regarding the duration-matching strategy indicate the presence of:

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs), and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-Soto's three assumptions regarding the duration-matching strategy indicate the presence of:

The following information relates to Questions

Serena Soto is a risk management specialist with Liability Protection advisors. trey hudgens, CFo of Kiest Manufacturing, enlists Soto's help with three projects. The first project is to defease some of Kiest's existing fixed-rate bonds that are maturing in each of the next three years. The bonds have no call or put provisions and pay interest annually. exhibit 1 presents the payment schedule for the bonds.

EXHIBIT 1 Kiest Manufacturing Bond Payment Schedule as of 1 October 2017

Maturity Date Payment Amount 1 October 2018 \ 9,572,000 1 October 2019 \ 8,392,000 1 October 2020 \ 8,200,000

The second project for Soto is to help hudgens immunize a $20 million portfolio of liabilities. The liabilities range from 3.00 years to 8.50 years with a Macaulay duration of 5.34 years, cash flow yield of 3.25%, portfolio convexity of 33.05, and basis point value (bPv) of $10,505. Soto suggested employing a duration-matching strategy using one of the three aaa rated bond portfolios presented in exhibit 2.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs), and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-Which portfolio in exhibit 2 fails to meet the requirements to achieve immunization for multiple liabilities?

The following information relates to Questions

Serena Soto is a risk management specialist with Liability Protection advisors. trey hudgens, CFo of Kiest Manufacturing, enlists Soto's help with three projects. The first project is to defease some of Kiest's existing fixed-rate bonds that are maturing in each of the next three years. The bonds have no call or put provisions and pay interest annually. exhibit 1 presents the payment schedule for the bonds.

EXHIBIT 1 Kiest Manufacturing Bond Payment Schedule as of 1 October 2017

Maturity Date Payment Amount 1 October 2018 \ 9,572,000 1 October 2019 \ 8,392,000 1 October 2020 \ 8,200,000

The second project for Soto is to help hudgens immunize a $20 million portfolio of liabilities. The liabilities range from 3.00 years to 8.50 years with a Macaulay duration of 5.34 years, cash flow yield of 3.25%, portfolio convexity of 33.05, and basis point value (bPv) of $10,505. Soto suggested employing a duration-matching strategy using one of the three aaa rated bond portfolios presented in exhibit 2.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs), and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-based on exhibit 2, the portfolio with the greatest structural risk is:

The following information relates to Questions

Doug Kepler, the newly hired chief financial officer for the City of radford, asks the dep-uty financial manager, hui ng, to prepare an analysis of the current investment portfolio and the city's current and future obligations. The city has multiple liabilities of different amounts and maturities relating to the pension fund, infrastructure repairs, and various other obligations. ng observes that the current fixed-income portfolio is structured to match the duration of each liability. Previously, this structure caused the city to access a line of credit for temporary mismatches resulting from changes in the term structure of interest rates.

Kepler asks ng for different strategies to manage the interest rate risk of the city's fixed-income investment portfolio against one-time shifts in the yield curve. ng considers two different strategies:

Strategy 1: immunization of the single liabilities using zero-coupon bonds held to maturity.

Strategy 2: immunization of the single liabilities using coupon-bearing bonds while continuously matching duration. The city also manages a separate, smaller bond portfolio for the radford School District. During the next five years, the school district has obligations for school expansions and ren- ovations. The funds needed for those obligations are invested in the loomberg barclays US aggregate index. Kepler asks ng which portfolio management strategy would be most efficient in mimicking this index.

a radford School board member has stated that she prefers a bond portfolio structure that provides diversification over time, as well as liquidity. in addressing the board member's

inquiry, ng examines a bullet portfolio, a barbell portfolio, and a laddered portfolio.

-an upward shift in the yield curve on Strategy 2 will most likely result in the:

The following information relates to Questions

Serena Soto is a risk management specialist with Liability Protection advisors. trey hudgens, CFo of Kiest Manufacturing, enlists Soto's help with three projects. The first project is to defease some of Kiest's existing fixed-rate bonds that are maturing in each of the next three years. The bonds have no call or put provisions and pay interest annually. exhibit 1 presents the payment schedule for the bonds.

EXHIBIT 1 Kiest Manufacturing Bond Payment Schedule as of 1 October 2017

Maturity Date Payment Amount 1 October 2018 \ 9,572,000 1 October 2019 \ 8,392,000 1 October 2020 \ 8,200,000

The second project for Soto is to help hudgens immunize a $20 million portfolio of liabilities. The liabilities range from 3.00 years to 8.50 years with a Macaulay duration of 5.34 years, cash flow yield of 3.25%, portfolio convexity of 33.05, and basis point value (bPv) of $10,505. Soto suggested employing a duration-matching strategy using one of the three aaa rated bond portfolios presented in exhibit 2.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs), and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-Which of hudgens's reasons for choosing bond mutual funds as an investment vehicle is correct?

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-Which of Compton's statements about liability-driven investing is (are) correct?

The following information relates to Questions

Chaopraya av is an investment advisor for high-net-worth individuals. one of her clients,Schuylkill Cy, plans to fund her grandson's college education and considers two options:

option 1 Contribute a lump sum of $300,000 in 10 years.

option 2 Contribute four level annual payments of $76,500 starting in 10 years.The grandson will start college in 10 years. Cy seeks to immunize the contribution today.For option 1, av calculates the present value of the $300,000 as $234,535. to immunize the future single outflow, av considers three bond portfolios given that no zero-coupon govern- ment bonds are available. The three portfolios consist of non-callable, fixed-rate, coupon-bearing government bonds considered free of default risk. av prepares a comparative analysis of the three portfolios, presented in exhibit 1.

EXHIBIT 1 Results of Comparative Analysis of Potential Portfolios Portfolio A Portfolio B Portfolio C Market value \ 235,727 \ 233,428 \ 235,306 Cash flow yield 2.504\% 2.506\% 2.502\% Macaulay duration 9.998 10.002 9.503 Convexity 119.055 121.498 108.091

av evaluates the three bond portfolios and selects one to recommend to Cy.

-Discuss the effectiveness of av's immunization strategy in terms of duration gaps.

The following information relates to Questions

Serena Soto is a risk management specialist with Liability Protection advisors. trey hudgens, CFo of Kiest Manufacturing, enlists Soto's help with three projects. The first project is to defease some of Kiest's existing fixed-rate bonds that are maturing in each of the next three years. The bonds have no call or put provisions and pay interest annually. exhibit 1 presents the payment schedule for the bonds.

EXHIBIT 1 Kiest Manufacturing Bond Payment Schedule as of 1 October 2017

Maturity Date Payment Amount 1 October 2018 \ 9,572,000 1 October 2019 \ 8,392,000 1 October 2020 \ 8,200,000

The second project for Soto is to help hudgens immunize a $20 million portfolio of liabilities. The liabilities range from 3.00 years to 8.50 years with a Macaulay duration of 5.34 years, cash flow yield of 3.25%, portfolio convexity of 33.05, and basis point value (bPv) of $10,505. Soto suggested employing a duration-matching strategy using one of the three aaa rated bond portfolios presented in exhibit 2.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs), and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-based on exhibit 2, relative to Portfolio C, Portfolio b:

The following information relates to Questions

Doug Kepler, the newly hired chief financial officer for the City of radford, asks the dep-uty financial manager, hui ng, to prepare an analysis of the current investment portfolio and the city's current and future obligations. The city has multiple liabilities of different amounts and maturities relating to the pension fund, infrastructure repairs, and various other obligations. ng observes that the current fixed-income portfolio is structured to match the duration of each liability. Previously, this structure caused the city to access a line of credit for temporary mismatches resulting from changes in the term structure of interest rates.

Kepler asks ng for different strategies to manage the interest rate risk of the city's fixed-income investment portfolio against one-time shifts in the yield curve. ng considers two different strategies:

Strategy 1: immunization of the single liabilities using zero-coupon bonds held to maturity.

Strategy 2: immunization of the single liabilities using coupon-bearing bonds while continuously matching duration. The city also manages a separate, smaller bond portfolio for the radford School District. During the next five years, the school district has obligations for school expansions and ren- ovations. The funds needed for those obligations are invested in the loomberg barclays US aggregate index. Kepler asks ng which portfolio management strategy would be most efficient in mimicking this index.

a radford School board member has stated that she prefers a bond portfolio structure that provides diversification over time, as well as liquidity. in addressing the board member's

inquiry, ng examines a bullet portfolio, a barbell portfolio, and a laddered portfolio.

-The effects of a non-parallel shift in the yield curve on Strategy 2 can be reduced by:

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-based on exhibit 1, which of the portfolios will best immunize SD&r's single liability?

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-based on DFC's bond holdings and exhibit 2, Compton should recommend:

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-The two-bond hypothetical portfolio's immunization goal is to lock in a rate of return equal to:

The following information relates to Questions

Doug Kepler, the newly hired chief financial officer for the City of radford, asks the dep-uty financial manager, hui ng, to prepare an analysis of the current investment portfolio and the city's current and future obligations. The city has multiple liabilities of different amounts and maturities relating to the pension fund, infrastructure repairs, and various other obligations. ng observes that the current fixed-income portfolio is structured to match the duration of each liability. Previously, this structure caused the city to access a line of credit for temporary mismatches resulting from changes in the term structure of interest rates.

Kepler asks ng for different strategies to manage the interest rate risk of the city's fixed-income investment portfolio against one-time shifts in the yield curve. ng considers two different strategies:

Strategy 1: immunization of the single liabilities using zero-coupon bonds held to maturity.

Strategy 2: immunization of the single liabilities using coupon-bearing bonds while continuously matching duration. The city also manages a separate, smaller bond portfolio for the radford School District. During the next five years, the school district has obligations for school expansions and ren- ovations. The funds needed for those obligations are invested in the loomberg barclays US aggregate index. Kepler asks ng which portfolio management strategy would be most efficient in mimicking this index.

a radford School board member has stated that she prefers a bond portfolio structure that provides diversification over time, as well as liquidity. in addressing the board member's

inquiry, ng examines a bullet portfolio, a barbell portfolio, and a laddered portfolio.

-a disadvantage of Strategy 1 is that:

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-relative to approach 2 of gaining passive exposure, an advantage of approach 1 is that it:

The following information relates to Questions

Serena Soto is a risk management specialist with Liability Protection advisors. trey hudgens, CFo of Kiest Manufacturing, enlists Soto's help with three projects. The first project is to defease some of Kiest's existing fixed-rate bonds that are maturing in each of the next three years. The bonds have no call or put provisions and pay interest annually. exhibit 1 presents the payment schedule for the bonds.

EXHIBIT 1 Kiest Manufacturing Bond Payment Schedule as of 1 October 2017

Maturity Date Payment Amount 1 October 2018 \ 9,572,000 1 October 2019 \ 8,392,000 1 October 2020 \ 8,200,000

The second project for Soto is to help hudgens immunize a $20 million portfolio of liabilities. The liabilities range from 3.00 years to 8.50 years with a Macaulay duration of 5.34 years, cash flow yield of 3.25%, portfolio convexity of 33.05, and basis point value (bPv) of $10,505. Soto suggested employing a duration-matching strategy using one of the three aaa rated bond portfolios presented in exhibit 2.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs), and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-based on exhibit 1, Kiest's liabilities would be classified as:

The following information relates to Questions

SD&r Capital (SD&r), a global asset management company, specializes in fixed-income investments. Molly Compton, chief investment officer, is eeting with a prospective client,Leah Mowery of DePuy Financial Company (DFC).Mowery informs Compton that DFC's previous fixed income manager focused on theinterest rate sensitivities of assets and liabilities when making asset allocation decisions. Comp-ton explains that, in contrast, SD&r's investment process first analyzes the size and timingof client liabilities, then builds an asset portfolio based on the interest rate sensitivity of thoseliabilities.

Compton notes that SD&r generally uses actively managed portfolios designed to earna return in excess of the benchmark portfolio. For clients interested in passive exposure tofixed-income instruments, SD&r offers two additional approaches.approach 1 Seeks to fully replicate the bloomberg barclays US aggregate bond index.

approach 2 Follows a stratified sampling or cell approach to indexing for a subset of the

bonds included in the bloomberg barclays US aggregate bond index. approach2 may also be customized to reflect client preferences.to illustrate SD&r's immunization approach for controlling portfolio interest rate risk,Compton discusses a hypothetical portfolio composed of two non-callable, investment-gradebonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.Mowery informs Compton that DFC has a single $500 million liability due in nine years,and she wants SD&r to construct a bond portfolio that earns a rate of return sufficient to payoff the obligation. Mowery expresses concern about the risks associated with an immunization strategy for this obligation. in response, Compton makes the following statements about lia-bility-driven investing:

Statement 1 although the amount and date of SD&r's liability is known with certainty,measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

Statement 2 a cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.Compton provides the four US dollar-denominated bond portfolios in exhibit 1 for consid-eration. Compton explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable. EXHIBIT 1 Proposed Bond Portfolios to Immunize SD\&R Single Liability Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Cash flow yield 7.48\% 7.50\% 7.53\% 7.51\% Average time to maturity 11.2 years 9.8 years 9.0 years 10.1 years Macaulay duration 9.8 8.9 8.0 9.1 Market value weighted duration 9.1 8.5 7.8 8.6 Convexity 154.11 131.75 130.00 109.32

The discussion turns to benchmark selection. DFC's previous fixed-income manager used a custom benchmark with the following characteristics:

Characteristic 1 The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.Characteristic 2 valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

Characteristic 3 historical prices and portfolio turnover are available for review. Compton explains that, in order to evaluate the asset allocation process, fixed-income port-folios should have an appropriate benchmark. Mowery asks for benchmark advice regarding DFC's portfolio of short-term and intermediate-term bonds, all denominated in US dollars.

Compton presents three possible benchmarks in exhibit 2.

-relative to approach 1 of gaining passive exposure, an advantage of approach 2 is that it:

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)