Exam 1: Introduction to Federal Taxation in Canada

Exam 1: Introduction to Federal Taxation in Canada144 Questions

Exam 2: Procedures and Administration92 Questions

Exam 3: Income or Loss From an Office or Employment108 Questions

Exam 4: Taxable Income and Tax Payable for Individuals105 Questions

Exam 5: Capital Cost Allowance95 Questions

Exam 6: Income or Loss From a Business103 Questions

Exam 7: Income From Property89 Questions

Exam 8: Capital Gains and Capital Losses104 Questions

Exam 9: Other Income, Other Deductions, and Other Issues130 Questions

Exam 10: Retirement Savings and Other Special Income Arrangements95 Questions

Exam 11: Taxable Income and Tax Payable for Individuals Revisited106 Questions

Exam 12: Taxable Income and Tax Payable for Corporations89 Questions

Exam 13: Taxation of Corporate Investment Income79 Questions

Exam 14: Other Issues in Corporate Taxation96 Questions

Exam 15: Corporate Taxation and Management Decisions93 Questions

Exam 16: Rollovers Under Section 8585 Questions

Exam 17: Other Rollovers and Sale of an Incorporated Business92 Questions

Exam 18: Partnerships96 Questions

Exam 19: Trusts and Estate Planning92 Questions

Exam 20: International Issues in Taxation66 Questions

Exam 21: Gst-Hst82 Questions

Select questions type

Canadian citizens are required to file a Canadian income tax return, without regard to where they currently live.

(True/False)

4.9/5  (41)

(41)

List three factors that would be considered in the determination of whether or not an individual is a resident of Canada.

(Short Answer)

4.9/5 (37)

Which of the following statements with respect to Canadian tax policy is NOT correct?

(Multiple Choice)

4.8/5 (40)

A part year resident for the current year is an individual who either establishes residency in Canada during the current year or, alternatively, terminates residency in Canada during the current year.

(True/False)

4.7/5 (35)

With respect to provincial income taxes, other than those assessed in Quebec, which of the following statements is NOT correct?

(Multiple Choice)

4.9/5 (36)

While the Sections of the Income Tax Act are numbered 1 through 260, there are actually more than 260 Sections. Explain why this is the case.

(Essay)

4.9/5 (37)

What is the meaning of "taxation year" as the phrase is used in the Income Tax Act?

(Essay)

4.9/5 (34)

What are some of the factors that have led to the entrenched use of tax expenditures as opposed to program spending?

(Essay)

4.8/5 (29)

Concerned with her inability to control the deficit, the Minister of Finance has indicated that she is considering the introduction of a head tax. This would be a tax of $200 per year, assessed on every living Canadian resident who, on December 31 of each year, has a head. In order to enforce the tax, all Canadian residents would be required to have a Head Administration Tax identification number (HAT, for short)tattooed in an inconspicuous location on their scalp. A newly formed special division of the RCMP, the Head Enforcement Administration Division (HEAD, for short), would run spot checks throughout the country in order to ensure that everyone has registered and received their HAT.

The Minister is very enthusiastic about the plan, anticipating that it will produce additional revenues of $5 billion per year. It is also expected to spur economic growth through increased sales of Canadian made toques.

As the Minister's senior policy advisor, you have been asked to prepare a memorandum evaluating this proposed new head tax.

Required: Prepare the memorandum.

(Essay)

4.8/5 (39)

Which of the following would be considered a desirable characteristic of an effective tax system?

(Multiple Choice)

4.9/5 (35)

Mr. Desmond Morris has spent his entire working life with his current employer, the Alcorn Manufacturing Company. In his first years with the Company, he was located in Winnipeg, Manitoba as a production supervisor. More recently, he was transferred to the Company's Calgary based subsidiary, where he has served as a manufacturing vice president until the current year.

Early in the current year, Mr. Morris was asked to move to the United States by April 1 to oversee the construction of a new manufacturing operation in Sarasota, Florida. It is expected that when the facility is completed, Mr. Morris will remain as the senior vice president in charge of all of the Florida operations. He does not have any intention of returning to live in Canada during the foreseeable future.

On April 1, Mr. Morris left Canada. In preparation for his departure, he had taken care to sell his residence, dispose of most of his personal property, and resign from all memberships in social and professional clubs. However, because Mr. Morris and his wife had three school age dependent children, it was decided that they would remain in Canada until the end of the current school year. As a consequence, Mrs. Morris and the children did not leave Canada until June 30. Until their departure, they resided in a small furnished apartment, rented on a month to month basis.

Required: For purposes of assessing Canadian income taxes, determine when Mr. Morris ceased to be a Canadian resident and the portion of his annual income which would be assessed for Canadian taxes. Explain your conclusions.

(Essay)

4.9/5 (29)

Karla Gomez is a Canadian resident who lives in Toronto. In the following two Cases, different assumptions are made with respect to the amounts and types of income she will include in her tax return for the current year. Information is also provided on the deductions that will be available to her for the year.

Case One - Karla had net employment income of $62,350. Unfortunately, her unincorporated flower shop suffered a net business loss of $115,600. In contrast, she had a very good year in the stock market, realizing the following gains and losses:  Also during the current year, Karla made deductible contributions of $4,560 to her RRSP.

Case Two - Karla had net employment income during the year of $45,600, as well as net business income of $27,310 and a net rental loss of $4,600. As part of a divorce agreement from a previous year, Karla paid spousal support of $600 per month to her former common-law partner, Lucretia Smart for the entire year. She realized the following results in the stock market during the year:

Also during the current year, Karla made deductible contributions of $4,560 to her RRSP.

Case Two - Karla had net employment income during the year of $45,600, as well as net business income of $27,310 and a net rental loss of $4,600. As part of a divorce agreement from a previous year, Karla paid spousal support of $600 per month to her former common-law partner, Lucretia Smart for the entire year. She realized the following results in the stock market during the year:  While Karla does not gamble on a regular basis, she enjoys the ambiance of the local casino. Given this, two or three times a year, she spends an evening dining and gambling with friends there. In March of this year, she got very lucky, winning $46,000 by hitting a slot machine jackpot.

Required: For each Case, calculate Karla's Net Income For Tax Purposes (Division B income)for the current year. Indicate the amount and type of any loss carry overs that would be available at the end of the year.

While Karla does not gamble on a regular basis, she enjoys the ambiance of the local casino. Given this, two or three times a year, she spends an evening dining and gambling with friends there. In March of this year, she got very lucky, winning $46,000 by hitting a slot machine jackpot.

Required: For each Case, calculate Karla's Net Income For Tax Purposes (Division B income)for the current year. Indicate the amount and type of any loss carry overs that would be available at the end of the year.

(Essay)

4.7/5 (27)

Tax expenditures are less costly to administer than direct funding programs.

(True/False)

4.9/5 (34)

The federal government does not collect personal or corporate taxes for Ontario or Quebec.

(True/False)

4.8/5 (42)

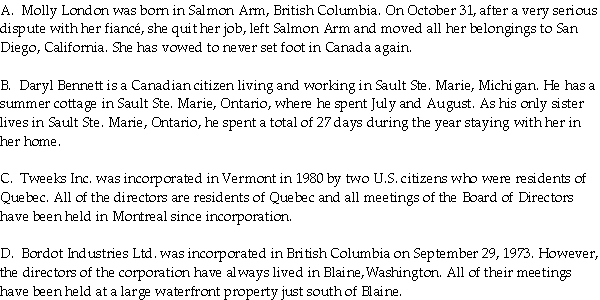

For each of the following persons, indicate how they would be taxed in Canada for the current year. Your answer should explain whether the person is a Canadian resident, what parts of their income would be subject to Canadian taxation, and the basis for your conclusions.

(Essay)

4.9/5 (37)

Mrs. Janice Theil gives $50,000 in Canada Savings Bonds to her 27 year old, unemployed daughter. What type of tax planning is involved in this transaction? Explain your conclusion.

(Essay)

4.7/5 (32)

Which of the following statements accurately describes a regressive tax?

(Multiple Choice)

4.8/5 (27)

A regressive tax is one that taxes high income individuals at lower effective rates. Explain why a sales tax levied at a flat rate of 8 percent can be regressive.

(Essay)

4.9/5 (36)

A value added tax is a tax levied on the increase in value of a commodity or service that has been created by the taxpayer's stage of the production or distribution cycle.

(True/False)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)