Exam 6: Risk and Return

Exam 1: An Overview of Financial Management and the Financial Environment46 Questions

Exam 2: Financial Statements, cash Flow, and Taxes77 Questions

Exam 3: Analysis of Financial Statements104 Questions

Exam 4: Time Value of Money168 Questions

Exam 5: Bonds, bond Valuation, and Interest Rates100 Questions

Exam 6: Risk and Return146 Questions

Exam 7: Valuation of Stocks and Corporations80 Questions

Exam 8: Financial Options and Applications in Corporate Finance28 Questions

Exam 9: The Cost of Capital92 Questions

Exam 10: The Basics of Capital Budgeting: Evaluating Cash Flows108 Questions

Exam 11: Cash Flow Estimation and Risk Analysis78 Questions

Exam 12: Corporate Valuation and Financial Planning41 Questions

Exam 13: Agency Conflicts and Corporate Governance6 Questions

Exam 14: Distributions to Shareholders: Dividends and Repurchases58 Questions

Exam 15: Capital Structure Decisions59 Questions

Exam 16: Supply Chains and Working Capital Management135 Questions

Exam 17: Multinational Financial Management49 Questions

Exam 18: Public and Private Financing: Initial Offerings, seasoned Offerings, and Investment Banks22 Questions

Exam 18: Extension 18 A: Rights Offerings4 Questions

Exam 19: Lease Financing23 Questions

Exam 20: Hybrid Financing: Preferred Stock, warrants, and Convertibles26 Questions

Exam 21: Dynamic Capital Structures22 Questions

Exam 22: Mergers and Corporate Control46 Questions

Exam 23: Enterprise Risk Management14 Questions

Exam 24: Bankruptcy, reorganization, and Liquidation12 Questions

Exam 25: Portfolio Theory and Asset Pricing Models35 Questions

Exam 26: Real Options11 Questions

Exam 27: Providing and Obtaining Credit29 Questions

Exam 28: Advanced Issues in Cash Management and Inventory Control17 Questions

Exam 29: Pension Plan Management10 Questions

Exam 30: Financial Management in Not For Profit Businesses10 Questions

Select questions type

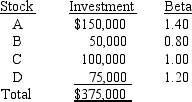

Paul McLaren holds the following portfolio:  Paul plans to sell Stock A and replace it with Stock E,which has a beta of 0.75.By how much will the portfolio beta change?

Paul plans to sell Stock A and replace it with Stock E,which has a beta of 0.75.By how much will the portfolio beta change?

Free

(Multiple Choice)

4.9/5  (38)

(38)

Correct Answer: Verified

Verified

D

The risk-free rate is 6%; Stock A has a beta of 1.0; Stock B has a beta of 2.0; and the market risk premium,rM - rRF,is positive.Which of the following statements is CORRECT?

Free

(Multiple Choice)

4.8/5 (22)

Correct Answer:Verified

B

Bloome Co.'s stock has a 25% chance of producing a 30% return,a 50% chance of producing a 12% return,and a 25% chance of producing a -18% return.What is the firm's expected rate of return?

Free

(Multiple Choice)

4.8/5 (43)

Correct Answer:Verified

D

Which of the following is NOT a potential problem when estimating and using betas,i.e.,which statement is FALSE?

(Multiple Choice)

4.8/5 (30)

Recession,inflation,and high interest rates are economic events that are best characterized as being

(Multiple Choice)

4.9/5 (31)

Gretta's portfolio consists of $700,000 invested in a stock that has a beta of 1.2 and $300,000 invested in a stock that has a beta of 0.8.The risk-free rate is 6% and the market risk premium is 5%.Which of the following statements is CORRECT?

(Multiple Choice)

5.0/5 (37)

Assume that two investors each hold a portfolio,and that portfolio is their only asset.Investor A's portfolio has a beta of minus 2.0,while Investor B's portfolio has a beta of plus 2.0.Assuming that the unsystematic risks of the stocks in the two portfolios are the same,then the two investors face the same amount of risk.However,the holders of either portfolio could lower their risks,and by exactly the same amount,by adding some "normal" stocks with beta = 1.0.

(True/False)

4.8/5 (39)

Variance is a measure of the variability of returns,and since it involves squaring the deviation of each actual return from the expected return,it is always larger than its square root,its standard deviation.

(True/False)

4.8/5 (33)

Gardner Electric has a beta of 0.88 and an expected dividend growth rate of 4.00% per year.The T-bill rate is 4.00%,and the T-bond rate is 5.25%.The annual return on the stock market during the past 4 years was 10.25%.Investors expect the average annual future return on the market to be 12.50%.Using the SML,what is the firm's required rate of return?

(Multiple Choice)

5.0/5 (27)

The SML relates required returns to firms' systematic (or market)risk.The slope and intercept of this line can be influenced by a manager's actions.

(True/False)

4.9/5 (29)

The CAPM is a multi-period model that takes account of differences in securities' maturities,and it can be used to determine the required rate of return for any given level of systematic risk.

(True/False)

4.7/5 (38)

Joel Foster is the portfolio manager of the SF Fund,a $3 million hedge fund that contains the following stocks.The required rate of return on the market is 11.00% and the risk-free rate is 5.00%.What rate of return should investors expect (and require)on this fund? Stack Amaunt A \ 1,075,000 1.20 B 675,000 0.50 C 750,000 1.40 D 500,000 0.75

(Multiple Choice)

4.8/5 (37)

Stock A has a beta of 0.8,Stock B has a beta of 1.0,and Stock C has a beta of 1.2.Portfolio P has 1/3 of its value invested in each stock.Each stock has a standard deviation of 25%,and their returns are independent of one another,i.e.,the correlation coefficients between each pair of stocks is zero.Assuming the market is in equilibrium,which of the following statements is CORRECT?

(Multiple Choice)

4.8/5 (30)

Managers should under no conditions take actions that increase their firm's risk relative to the market,regardless of how much those actions would increase the firm's expected rate of return.

(True/False)

4.7/5 (33)

The slope of the SML is determined by investors' aversion to risk.The greater the average investor's risk aversion,the steeper the SML.

(True/False)

4.9/5 (30)

Porter Plumbing's stock had a required return of 11.75% last year,when the risk-free rate was 5.50% and the market risk premium was 4.75%.Then an increase in investor risk aversion caused the market risk premium to rise by 2%.The risk-free rate and the firm's beta remain unchanged.What is the company's new required rate of return? (Hint: First calculate the beta,then find the required return.)

(Multiple Choice)

4.8/5 (30)

Risk-averse investors require higher rates of return on investments whose returns are highly uncertain,and most investors are risk averse.

(True/False)

4.9/5 (32)

Stock LB has a beta of 0.5 and Stock HB has a beta of 1.5.The market is in equilibrium,with required returns equaling expected returns.Which of the following statements is CORRECT?

(Multiple Choice)

4.8/5 (47)

Which of the following is most likely to be true for a portfolio of 40 randomly selected stocks?

(Multiple Choice)

5.0/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)