Exam 25: Portfolio Theory and Asset Pricing Models

Exam 1: An Overview of Financial Management and the Financial Environment46 Questions

Exam 2: Financial Statements, cash Flow, and Taxes77 Questions

Exam 3: Analysis of Financial Statements104 Questions

Exam 4: Time Value of Money168 Questions

Exam 5: Bonds, bond Valuation, and Interest Rates100 Questions

Exam 6: Risk and Return146 Questions

Exam 7: Valuation of Stocks and Corporations80 Questions

Exam 8: Financial Options and Applications in Corporate Finance28 Questions

Exam 9: The Cost of Capital92 Questions

Exam 10: The Basics of Capital Budgeting: Evaluating Cash Flows108 Questions

Exam 11: Cash Flow Estimation and Risk Analysis78 Questions

Exam 12: Corporate Valuation and Financial Planning41 Questions

Exam 13: Agency Conflicts and Corporate Governance6 Questions

Exam 14: Distributions to Shareholders: Dividends and Repurchases58 Questions

Exam 15: Capital Structure Decisions59 Questions

Exam 16: Supply Chains and Working Capital Management135 Questions

Exam 17: Multinational Financial Management49 Questions

Exam 18: Public and Private Financing: Initial Offerings, seasoned Offerings, and Investment Banks22 Questions

Exam 18: Extension 18 A: Rights Offerings4 Questions

Exam 19: Lease Financing23 Questions

Exam 20: Hybrid Financing: Preferred Stock, warrants, and Convertibles26 Questions

Exam 21: Dynamic Capital Structures22 Questions

Exam 22: Mergers and Corporate Control46 Questions

Exam 23: Enterprise Risk Management14 Questions

Exam 24: Bankruptcy, reorganization, and Liquidation12 Questions

Exam 25: Portfolio Theory and Asset Pricing Models35 Questions

Exam 26: Real Options11 Questions

Exam 27: Providing and Obtaining Credit29 Questions

Exam 28: Advanced Issues in Cash Management and Inventory Control17 Questions

Exam 29: Pension Plan Management10 Questions

Exam 30: Financial Management in Not For Profit Businesses10 Questions

Select questions type

Stock A's beta is 1.5 and Stock B's beta is 0.5.Which of the following statements must be true about these securities? (Assume market equilibrium.)

Free

(Multiple Choice)

4.8/5  (35)

(35)

Correct Answer: Verified

Verified

C

Which of the following is NOT a potential problem with beta and its estimation?

Free

(Multiple Choice)

4.8/5 (40)

Correct Answer:Verified

B

Assume that the market is in equilibrium and that stock betas can be estimated with historical data.The returns on the market,the returns on United Fund (UF),the risk-free rate,and the required return on the United Fund are shown below.Based on this information,what is the required return on the market,rM? Year Market UF 2008 -9\% -14\% 2009 11\% 16\% 2010 15\% 22\% 2011 5\% 7\% 2012 -1\% -2\%

Free

(Multiple Choice)

4.8/5 (35)

Correct Answer:Verified

D

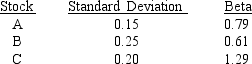

You have the following data on three stocks:  As a risk minimizer,you would choose Stock ____ if it is to be held in isolation and Stock ____ if it is to be held as part of a well-diversified portfolio.

As a risk minimizer,you would choose Stock ____ if it is to be held in isolation and Stock ____ if it is to be held as part of a well-diversified portfolio.

(Multiple Choice)

4.9/5 (27)

Suppose that (1)investors expect a 4.0% rate of inflation in the future, (2)the real risk-free rate is 3.0%, (3)the market risk premium is 5.0%, (4)Talcott Inc.'s beta is 1.00,and (5)its realized rate of return has averaged 15.0% over the last 5 years.Calculate the required rate of return for Talcot Inc.

(Multiple Choice)

4.9/5 (29)

The Y-axis intercept of the SML indicates the return on an individual asset when the realized return on an average (b = 1)stock is zero.

(True/False)

4.8/5 (36)

In a portfolio of three different stocks,which of the following could NOT be true?

(Multiple Choice)

4.7/5 (39)

If you plotted the returns of Selleck & Company against those of the market and found that the slope of your line was negative,the CAPM would indicate that the required rate of return on Selleck's stock should be less than the risk-free rate for a well-diversified investor,assuming that the observed relationship is expected to continue in the future.

(True/False)

4.7/5 (36)

Stock A has an expected return rA = 10% and A = 10%.Stock B has rB = 14% and B = 15%.rAB = 0.The rate of return on riskless assets is 6%.

a.

Construct a graph that shows the feasible and efficient sets, giving consideration to the existence of the riskless asset.

b.

Explain what would happen to the CML if the two stocks had (a) a positive correlation coefficient or (b) a negative correlation coefficient.

c.

Suppose these were the only three securities (A, B, and riskless) in the economy, and everyone's indifference curves were such that they were tangent to the CML to the right of the point where the CML was tangent to the efficient set of risky assets. Would this represent a stable equilibrium? If not, how would an equilibrium be produced?

(Essay)

4.9/5 (31)

Security A has an expected return of 12.4% with a standard deviation of 15%,and a correlation with the market of 0.85.Security B has an expected return of -0.73% with a standard deviation of 20%,and a correlation with the market of -0.67.The standard deviation of rM is 12%.

A) To someone who acts in accordance with the CAPM, which security is more risky, A or B? Why? (Hint: No calculations are necessary to answer this question; it is easy.)

B) What are the beta coefficients of A and B? Calculations are necessary.

C) If the risk-free rate is 6%, what is the value of rM?

(Essay)

4.9/5 (36)

If the returns of two firms are negatively correlated,then one of them must have a negative beta.

(True/False)

4.8/5 (30)

A stock with a beta equal to -1.0 has zero systematic (or market)risk.

(True/False)

4.8/5 (38)

You have the following data on (1)the average annual returns of the market for the past 5 years and (2)similar information on Stocks A and B.Which of the possible answers best describes the historical betas for A and B?

Years Market 1 0.03 2 -0.05 3 0.01 4 -0.10 5 006 Stock A 0.16 0.20 0.18 0.25 014 Stock B 0.05 0.05 0.05 0.05 005

(Multiple Choice)

4.7/5 (32)

Calculate the required rate of return for the Wagner Assets Management Group,which holds 4 stocks.The market's required rate of return is 15.0%,the risk-free rate is 7.0%,and the Fund's assets are as follows: Stack Investment Beta A \ 1.50 200,000 B -0.50 300,000 C 1.25 500,000 D 1,000,000 0.75

(Multiple Choice)

4.8/5 (39)

We will almost always find that the beta of a diversified portfolio is less stable over time than the beta of a single security.

(True/False)

4.8/5 (28)

Which is the best measure of risk for an asset held in isolation,and which is the best measure for an asset held in a diversified portfolio?

(Multiple Choice)

4.8/5 (38)

Assume an economy in which there are three securities: Stock A with rA = 10% and A = 10%; Stock B with rB = 15% and B = 20%; and a riskless asset with rRF = 7%.Stocks A and B are uncorrelated (rAB = 0).Which of the following statements is most CORRECT?

(Multiple Choice)

4.9/5 (33)

Consider the information below for Postman Builders Inc.Suppose that the expected inflation rate and thus the inflation premium increase by 2.0 percentage points,and Postman acquires risky assets that increase its beta by the indicated percentage.What is the firm's new required rate of return? Beta:

Reqquired return

percentage increase in beta:

(Multiple Choice)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)