Exam 6: Sellers and Incentives

Exam 1: The Principles and Practice of Economics103 Questions

Exam 2: Economic Methods and Economic Questions94 Questions

Exam 3: Optimization: Doing the Best You Can94 Questions

Exam 4: Demand, supply, and Equilibrium185 Questions

Exam 5: Consumers and Incentives187 Questions

Exam 6: Sellers and Incentives261 Questions

Exam 7: Perfect Competition and the Invisible Hand251 Questions

Exam 8: Trade264 Questions

Exam 9: Externalities and Public Goods223 Questions

Exam 10: The Government in the Economy: Taxation and Regulation244 Questions

Exam 11: Markets for Factors of Production237 Questions

Exam 12: Monopoly295 Questions

Exam 13: Game Theory and Strategic Play199 Questions

Exam 14: Oligopoly and Monopolistic Competition264 Questions

Exam 15: Trade-Offs Involving Time and Risk147 Questions

Exam 16: The Economics of Information119 Questions

Exam 17: Auctions and Bargaining123 Questions

Exam 18: Social Economics111 Questions

Select questions type

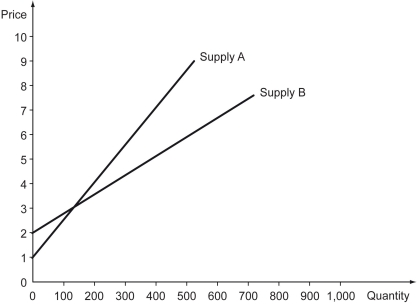

The supply curve of good A,and the supply curve if good B are both depicted in the following graph.Which statement is true?

Free

(Multiple Choice)

4.8/5  (45)

(45)

Correct Answer: Verified

Verified

B

Which of the costs below is an example of a fixed cost in the short run?

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

D

When price is less than the firms' minimum average total cost in a perfectly competitive market in the long run,________.

Free

(Multiple Choice)

4.9/5 (27)

Correct Answer:Verified

B

Suppose ethanol is produced in a perfectly competitive market.If a subsidy is paid to ethanol producers,the ethanol producers' profit will ________.

(Multiple Choice)

4.8/5 (30)

The entry and exit of firms in a perfectly competitive market is mostly dependent on ________.

(Multiple Choice)

4.8/5 (34)

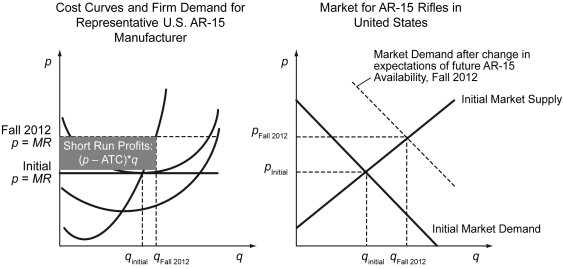

Suppose the market for AR-15 style rifles in the United States was in an initial long-run equilibrium.In the fall of 2012,the demand for these rifles increased substantially due to concerns that President Obama would either ban or restrict the sale of these semi-automatic rifles.As a result,the market price of these rifles increased,and gun manufacturers earned positive economic profits (shown in the figure below).

The presence of economic profits in the short-run will lead to the ________.

The presence of economic profits in the short-run will lead to the ________.

(Multiple Choice)

4.8/5 (31)

Scenario: In 2012, the company behind the EpiPen settled a lawsuit by agreeing to allow a generic competitor into the market in 2015, potentially cutting into a big part of its business. The company, Mylan, had already been steadily increasing the price of EpiPen, an injector containing a drug that can save people from life-threatening allergy attacks. After the settlement, it started to raise the price even faster. Now, as Mylan faces growing public furor over its pricing of EpiPen, the company's history of pricing the product highlights a common tactic in the drug industry: sharply raising prices in the years just before a generic competitor reaches the market, as a sort of final attempt to milk big profits from the brand-name drug. Whether the looming generic competition was a motive for the price increases is not entirely clear, because Mylan has declined to answer questions about its thinking. But while the company was once taking two 10 percent price increases a year, it has made two 15 percent increases annually starting in 2014, when the generic competition seemed imminent. Over all, the list price for a pack of two EpiPens is now over $600, up from a little more than $100 in 2007, the year Mylan acquired the product. Most of that increase-a rise to $609 from $265-has come in the last three years. (Source: "Mylan Raised EpiPen's Price Before the Expected Arrival of a Generic," New York Times, August 24, 2016.)

-Refer to the scenario above.Which condition of a perfectly competitive market could most directly be hampered in the market for epinephrine autoinjectors?

(Multiple Choice)

4.9/5 (36)

Gary produces handmade baseball gloves.On any given working day,it costs Gary $50 to make the first glove,$60 to make the second,$80 to make the third,and $110 to make the fourth glove.What should Gary do?

(Multiple Choice)

4.8/5 (44)

Which of the following statements is true in the short run?

(Multiple Choice)

4.8/5 (28)

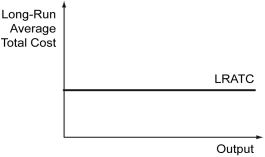

The long-run average total cost (LRATC)shown below exhibits ________.

(Multiple Choice)

4.8/5 (30)

Given the following price,quantity,and cost numbers,estimate the profit-maximizing output,assuming that the firm is operating in a perfectly competitive market.What is the fixed cost that the firm faces? What is the profit at the profit-maximizing output?

(Essay)

4.9/5 (32)

In a perfectly competitive market,a marginal entrant ________.

(Multiple Choice)

4.9/5 (31)

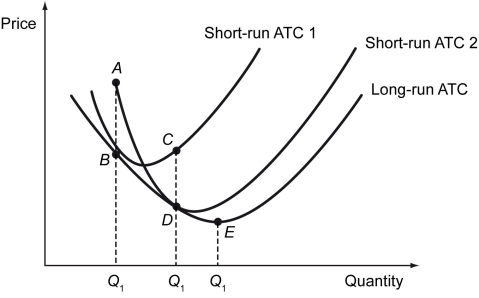

The following figure depicts a firm's long-run average total cost and selected short-run average total cost curves.

-Refer to the figure above.The firm is currently producing at point D.What prevents the firm from producing at E?

-Refer to the figure above.The firm is currently producing at point D.What prevents the firm from producing at E?

(Multiple Choice)

4.8/5 (37)

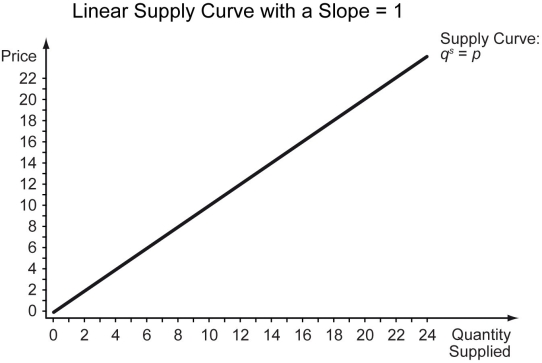

If a firm's supply curve is linear qˢ = p with a slope of 1 (see the graph below),

Then the firm's price elasticity of supply is ________.

Then the firm's price elasticity of supply is ________.

(Multiple Choice)

4.8/5 (28)

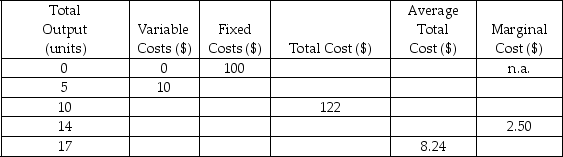

The following table shows the total output, variable costs, fixed costs, total costs, average total costs, and marginal costs of a firm, with some cells in the table intentionally left blank.

-Refer to the table above.What is the total cost of producing 5 units of output?

-Refer to the table above.What is the total cost of producing 5 units of output?

(Multiple Choice)

4.9/5 (32)

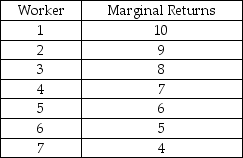

Scenario: A car repair shop hires workers and pays them the federal minimum wage of $7.25. The following table shows the marginal returns to each worker in terms of number of cars repaired.

-Refer to the scenario above.Which statement is true?

-Refer to the scenario above.Which statement is true?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)