Exam 14: Firms in Competitive Markets

Exam 1: Ten Principles of Economics237 Questions

Exam 2: Thinking Like an Economist267 Questions

Exam 3: Interdependence and the Gains From Trade217 Questions

Exam 4: The Market Forces of Supply and Demand303 Questions

Exam 5: Elasticity and Its Applications282 Questions

Exam 6: Supply, demand, and Government Policies252 Questions

Exam 7: Consumers, producers, and the Efficiency of Markets248 Questions

Exam 8: Application: the Costs of Taxation245 Questions

Exam 9: Application: International Trade245 Questions

Exam 10: Externalities288 Questions

Exam 11: Public Goods and Common Resources258 Questions

Exam 12: The Design of the Tax System328 Questions

Exam 13: The Costs of Production303 Questions

Exam 14: Firms in Competitive Markets271 Questions

Exam 15: Monopoly306 Questions

Exam 16: Oligopoly291 Questions

Exam 17: Monopolistic Competition257 Questions

Exam 18: The Markets for the Factors of Production284 Questions

Exam 19: Earnings and Discrimination286 Questions

Exam 20: Income Inequality and Poverty247 Questions

Exam 21: The Theory of Consumer Choice238 Questions

Exam 22: Frontiers of Microeconomics199 Questions

Exam 23: Measuring a Nations Income215 Questions

Exam 24: Measuring the Cost of Living208 Questions

Exam 25: Production and Growth240 Questions

Exam 26: Saving, investment, and the Financial System282 Questions

Exam 27: The Basic Tools of Finance249 Questions

Exam 28: Unemployment242 Questions

Exam 29: The Monetary System277 Questions

Exam 30: Money Growth and Inflation224 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts256 Questions

Exam 32: A Macroeconomic Theory of the Open Economy217 Questions

Exam 33: Aggregate Demand and Aggregate Supply302 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand249 Questions

Exam 35: The Short Run Trade Off Between Inflation and Unemployment246 Questions

Exam 36: Five Debates Over Macroeconomic Policy140 Questions

Select questions type

In calculating accounting profit,accountants typically don't include

Free

(Multiple Choice)

4.9/5  (40)

(40)

Correct Answer: Verified

Verified

D

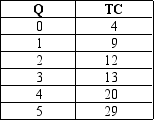

The following table presents the total cost of production for various levels of output for a competitive firm:  What is the lowest price at which this firm might choose to operate?

What is the lowest price at which this firm might choose to operate?

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

B

Suppose a firm in a competitive market received $1,000 in total revenue and had a marginal revenue of $10 for the last unit produced and sold.What is the average revenue per unit,and how many units were sold?

Free

(Multiple Choice)

4.7/5 (43)

Correct Answer:Verified

D

When price is greater than marginal cost for a firm in a competitive market,

(Multiple Choice)

4.9/5 (28)

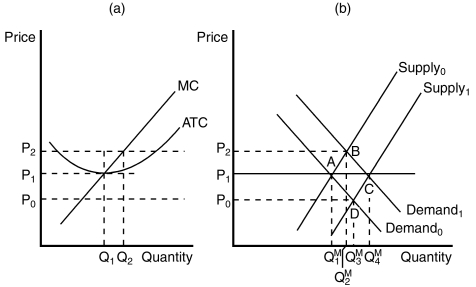

Figure 14-7

-Refer to Figure 14-7.When the market is in long-run equilibrium at point A in panel (b),the firm represented in panel (a)will

-Refer to Figure 14-7.When the market is in long-run equilibrium at point A in panel (b),the firm represented in panel (a)will

(Multiple Choice)

4.8/5 (34)

Regardless of the cost structure of firms in a competitive market,in the long run

(Multiple Choice)

4.9/5 (27)

If ABC Company sells its product in a competitive market,then

(Multiple Choice)

4.8/5 (39)

A market might have an upward-sloping long-run supply curve if

(Multiple Choice)

4.9/5 (36)

Suppose that in a competitive market the market price is $2.50.What is marginal revenue for the last unit sold by the typical firm in this market?

(Multiple Choice)

4.8/5 (38)

When a competitive market experiences an increase in demand that induces an increase in production costs,which of the following is most likely to arise?

(Multiple Choice)

4.8/5 (27)

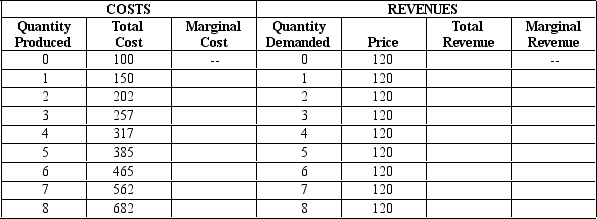

Table 14-2

The following table presents cost and revenue information for Soper's Port Vineyard.

-Refer to Table 14-2.Consumers are willing to pay $120 per unit of port wine.What is the total revenue from selling 7 units?

-Refer to Table 14-2.Consumers are willing to pay $120 per unit of port wine.What is the total revenue from selling 7 units?

(Multiple Choice)

4.8/5 (31)

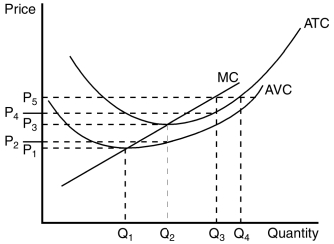

Figure 14-4

The figure below depicts the cost structure of a firm in a competitive market.

-Refer to Figure 14-4.When market price is P₂,a profit-maximizing firm's losses can be represented by the area

-Refer to Figure 14-4.When market price is P₂,a profit-maximizing firm's losses can be represented by the area

(Multiple Choice)

4.7/5 (38)

If a competitive firm is currently producing a level of output at which marginal revenue exceeds marginal cost,then

(Multiple Choice)

4.8/5 (36)

The short-run supply curve for a firm in a perfectly competitive market is

(Multiple Choice)

4.8/5 (32)

Which of the following statements regarding a competitive firm is true?

(Multiple Choice)

4.9/5 (31)

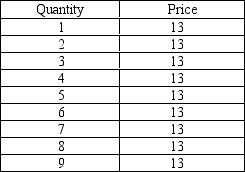

Table 14-1

-Refer to Table 14-1.Over what range of output is marginal revenue declining?

-Refer to Table 14-1.Over what range of output is marginal revenue declining?

(Multiple Choice)

4.8/5 (33)

Table 14-1

-Refer to Table 14-1.Over which range of output is average revenue equal to price?

(Multiple Choice)

4.9/5 (32)

A firm must be participating in a competitive market for average revenue to equal price.

(True/False)

4.7/5 (45)

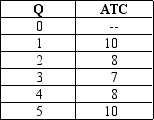

The following table gives the average total cost of production for various levels of output for a competitive firm:  If the firm's fixed cost of production is $3 and the market price is $10,how many units should the firm produce to maximize its profit?

If the firm's fixed cost of production is $3 and the market price is $10,how many units should the firm produce to maximize its profit?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)