Exam 2: Product Costing Systems: Concepts and Design Issues

Exam 1: Cost Management and Strategic Decision Making Evaluating Opportunities and Leading Change75 Questions

Exam 2: Product Costing Systems: Concepts and Design Issues117 Questions

Exam 3: Cost Accumulation for Job-Shop and Batch Production Operations90 Questions

Exam 4: Activity-Based Costing Systems102 Questions

Exam 5: Activity-Based Management89 Questions

Exam 6: Managing Customer Profitability73 Questions

Exam 7: Managing Quality and Time to Create Value114 Questions

Exam 8: Process-Costing Systems110 Questions

Exam 9: Joint-Process Costing90 Questions

Exam 10: Managing and Allocating Support-Service Costs80 Questions

Exam 11: Cost Estimation90 Questions

Exam 12: Financial and Cost-Volume-Profit Models69 Questions

Exam 13: Cost Management and Decision Making70 Questions

Exam 14: Strategic Issues in Making Long-Term Capital Investment Decisions97 Questions

Exam 15: Budgeting and Financial Planning81 Questions

Exam 16: Standard Costing, Variance Analysis, and Kaizen Costing80 Questions

Exam 17: Flexible Budgets, Overhead Cost Management, and Activity-Based Budgeting97 Questions

Exam 18: Organizational Design, Responsibility Accounting, and Evaluation of Divisional Performance80 Questions

Exam 19: Transfer Pricing76 Questions

Exam 20: Performance Measurement Systems Glossary Photo Credits81 Questions

Select questions type

The product cost of merchandise inventory acquired by a retailer consists of the purchase cost of the inventory plus any shipping charges.

(True/False)

4.8/5  (45)

(45)

Unit-level costs are incurred for every unit of product manufactured or service performed.

(True/False)

4.9/5 (35)

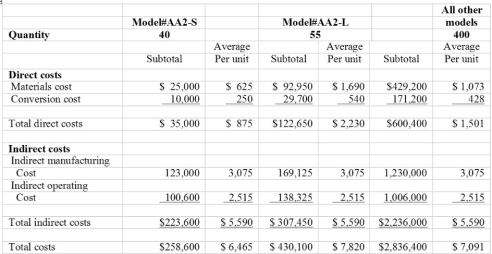

Additional information:

● Sales prices:

$8,900 per unit of Model AA2-S

16,700 per unit of Model AA2-L

10,000 per unit of all other models

● The only spending increase was for material cost because this increased production. All other spending as shown above was unchanged.

● Sales were as follows:

32 units of part Model AA2-S

55 units of Model AA2-L

350 units of all other models

Case

Sabrina Wood has recently inherited a medium-sized machine shop. Upon taking over, she finds that the business is not doing as well as her Dad had made it out to be. The list of dissatisfied customers has been steadily growing; she has had to do a lot of explaining to customers and promised to improve the situation. She called her Dad's loyal production manager, James Hurley, to her office in order to have a chat with him.

Wood: Good morning Mr. Hurley. How are you?

Hurley: Good morning. I'm doing fine. What can I do for you?

Wood: I'll be honest with you. I need your help and advice. You always were my Dad's most trusted employee.

Hurley: Any time, Ms. Wood. What seems to be the problem?

Wood: I have recently received calls from some long-time customers who are frustrated with our cost, quality and on-time delivery performance. They said they would soon take their business elsewhere if we do not improve. These people were good friends of my Dad and gave him their business only because of this friendship.

Hurley: To be honest, our production processes need improvement. The whole shop floor has become a bit chaotic during the last five years when more orders started coming in. We are just unable to cope. It is not that we do not have the capacity or the capabilities. Our problem is more because of the lack of discipline. I could not do a whole lot because your Dad was determined to continue in this manner. Wood: My father was stubborn. I do not want to be like him. Please tell me if there are other problems that we need to deal with.

Hurley: The other problem is the lack of a cost management system. Your Dad ran the show by just recording all the costs and computing an average. We have no idea which products are making money and which are not. Do you mind if I call Lindsay Sawin, our new accountant, and ask her to join us? She can explain you what is going on, and can also make some suggestions to improve.

Wood: Please do. (She waits for Sawin to join the meeting.) Good morning, Lindsay. Mr. Hurley tells me that our costing system is in disarray.

Sawin: Yes. Currently, there is no order in the way that we measure costs. In fact, in the last three months since I joined this company, I have just been trying to understand the processes, the types of resources that are used, where they are used in the company's value-chain, and their traceability to decisions.

Wood: Thank you for doing this. What can we do? In fact, is there any hope for us? It is important that we understand costs and are able to compute the cost and profitability information for each of our products or at least product lines. Do you have any ideas?

Sawin: Yes, we can certainly do that. However, I must inform you that there are three alternative costing methods and each of these has its merits and limitations.

Wood: I did not realize that we have to make decisions about the type of the costing system we would like to use. We need to know a little more about each system. Can you show us what would happen under each costing system? In particular, I would like you to present a scenario where you use cost data to show us the product costs and operating incomes from using the three different costing methods. This might open the eyes of many of us around here. Together, we can work hard to keep my Dad's company alive. Sawin: Please give me a month's time. I will put together something to present to you and several others. It would be nice if we can spend an entire afternoon on this so that I can get into some detail. Required:

Assume the role of Lindsay Sawin. Identify all the issues raised and address them. For the computational requirement, consider the following information.

(Essay)

4.8/5 (32)

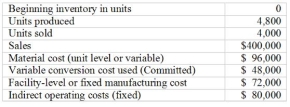

Use the following to answer questions:

-The throughput operating income is:

-The throughput operating income is:

(Multiple Choice)

4.7/5 (39)

Variable costs change in total direct proportion to a change in the activity of a cost driver.

(True/False)

4.9/5 (34)

Factory heating and air conditioning should be considered a product cost in a manufacturing operation.

(True/False)

4.9/5 (37)

In a manufacturing company, cost of goods manufactured consists of direct materials put into production, direct labor and manufacturing overhead incurred plus the beginning inventory of finished goods less the ending inventory of finished goods

(True/False)

4.9/5 (39)

Sunk costs are past resource payments that cannot be changed by any current or future decision.

(True/False)

4.7/5 (40)

Absorption costing measures use gross margin as the contribution to profit.

(True/False)

4.8/5 (35)

The cost of renting a car for the sales force should be accounted for as:

(Multiple Choice)

4.8/5 (45)

Use the following to answer questions:

-The variable cost of goods sold is:

(Multiple Choice)

4.7/5 (29)

Use the following to answer questions:

-The absorption operating income is:

(Multiple Choice)

4.9/5 (40)

A cost driver is a characteristic of an activity or event that causes that activity or event to incur cost.

(True/False)

4.8/5 (28)

Which of the following is an example of a facility-level cost?

(Multiple Choice)

4.7/5 (38)

Throughput costing inventory contains no conversion and indirect costs.

(True/False)

4.8/5 (32)

Overtime premium costs should theoretically be considered part of direct labor cost.

(True/False)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)