Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis

Exam 1: What Is Economics232 Questions

Exam 2: The Economy: Myth and Reality155 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice255 Questions

Exam 4: Supply and Demand: an Initial Look313 Questions

Exam 5: Consumer Choice: Individual and Market Demand206 Questions

Exam 6: Demand and Elasticity214 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis221 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis194 Questions

Exam 9: Securities: Business Finance and the Economy: the Tail That Wags the Dog203 Questions

Exam 10: The Firm and the Industry Under Perfect Competition212 Questions

Exam 11: Monopoly208 Questions

Exam 12: Between Competition and Monopoly230 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust155 Questions

Exam 14: The Case for Free Markets: the Price System225 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination172 Questions

Exam 21: Is Useconomic Leadership Threatened75 Questions

Exam 22: An Introduction to Macroeconomics216 Questions

Exam 23: The Goals of Macroeconomic Policy212 Questions

Exam 24: Economic Growth: Theory and Policy228 Questions

Exam 25: Aggregate Demand and the Powerful Consumer219 Questions

Exam 26: Demand-Side Equilibrium: Unemployment or Inflation216 Questions

Exam 27: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 28: Managing Aggregate Demand: Fiscal Policy210 Questions

Exam 29: Money and the Banking System224 Questions

Exam 30: Monetary Policy: Conventional and Unconventional210 Questions

Exam 31: He Financial Crisis and the Great Recession66 Questions

Exam 32: The Debate Over Monetary and Fiscal Policy219 Questions

Exam 33: Budget Deficits in the Short and Long Run215 Questions

Exam 34: The Trade-Off Between Inflation and Unemployment219 Questions

Exam 35: International Trade and Comparative Advantage223 Questions

Exam 36: The International Monetary System: Order or Disorder218 Questions

Exam 37: Exchange Rates and the Macroeconomy219 Questions

Select questions type

If the MPP of labor is 60 and the price of labor per period is $20, the MPP of machinery is 75 and the price of the machinery per period is $25, in order to achieve optimal input proportions the firm should use

(Multiple Choice)

4.9/5  (32)

(32)

Input choices in the present are often affected by past decisions.

(True/False)

4.8/5 (36)

A budget line is the locus of all points representing every input combination of inputs that the producer can afford to buy with a given amount of money and given input prices.

(True/False)

4.9/5 (39)

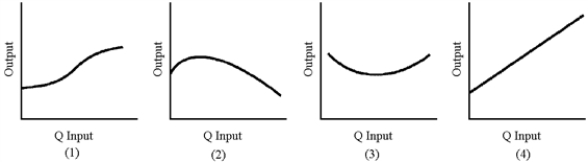

Figure 7-1

-In Figure 7-1, which graph best represents total physical product with diminishing returns?

-In Figure 7-1, which graph best represents total physical product with diminishing returns?

(Multiple Choice)

4.9/5 (32)

The United Auto Workers union is largely responsible for the historically high pay of American auto workers by negotiating pay raises above those obtained by workers in other industries.In addition to increasing the pay of auto workers, what other long-run effect would this high pay have on the use of auto workers?

(Essay)

4.7/5 (38)

Which of the following experiments will yield observations that would allow one to calculate the marginal physical product of labor?

(Multiple Choice)

4.9/5 (27)

Marginal revenue product equals the marginal physical product multiplied by the quantity demanded.

(True/False)

4.8/5 (37)

The short-run average cost curve shows the lowest possible average cost corresponding to each output level, assuming that all inputs are variable.

(True/False)

4.9/5 (36)

If in some range of production average cost is falling, the firm is experiencing

(Multiple Choice)

4.8/5 (33)

Figure 7-1

-Of the graphs in Figure 7-1, which best represents marginal physical product?

(Multiple Choice)

4.9/5 (34)

Draw a graph using production indifference curves and budget lines showing a firm initially minimizing cost with its inputs of A and B.Then illustrate a new optimal combination of inputs when the prices of the inputs change.

(Essay)

4.8/5 (28)

Cost curves in the long run differ from cost curves in the short run.

(True/False)

4.7/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)