Exam 15: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Enterprise31 Questions

Exam 2: Financial Goals and Corporate Governance51 Questions

Exam 3: The International Monetary System60 Questions

Exam 4: The Balance of Payments63 Questions

Exam 5: The Foreign Exchange Market60 Questions

Exam 6: International Parity Conditions67 Questions

Exam 7: Foreign Exchange Rate Determination and Forecasting51 Questions

Exam 8: Foreign Currency Derivatives57 Questions

Exam 9: Transaction Exposure56 Questions

Exam 10: Operating Exposure62 Questions

Exam 11: Translation Exposure59 Questions

Exam 12: Global Cost and Availability of Capital62 Questions

Exam 13: Sourcing Equity Capital Globally66 Questions

Exam 14: Financial Structure and International Debt58 Questions

Exam 15: Interest Rate and Currency Swaps63 Questions

Exam 16: International Portfolio Theory and Diversification58 Questions

Exam 17: Foreign Direct Investment Theory and Strategy47 Questions

Exam 18: Political Risk Assessment and Management56 Questions

Exam 19: Multinational Capital Budgeting60 Questions

Exam 20: International Trade Finance55 Questions

Exam 21: Multinational Tax Management52 Questions

Exam 22: Working Capital Management59 Questions

Select questions type

Outright techniques of interest rate risk management do not include which of the following?

Free

(Multiple Choice)

4.7/5  (40)

(40)

Correct Answer: Verified

Verified

D

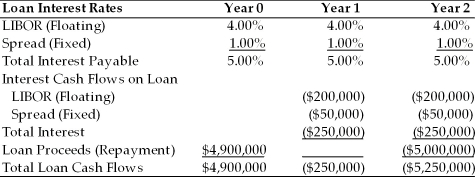

TABLE 15.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 15.1. What is the all-in-cost (i.e., the internal rate of return) of the Polaris loan including the LIBOR rate, fixed spread and upfront fee?

-Refer to Table 15.1. What is the all-in-cost (i.e., the internal rate of return) of the Polaris loan including the LIBOR rate, fixed spread and upfront fee?

Free

(Multiple Choice)

4.9/5 (28)

Correct Answer:Verified

D

Which of the following is NOT true?

Free

(Multiple Choice)

4.8/5 (40)

Correct Answer:Verified

D

An interbank-traded contract to buy or sell interest rate payments on a notional principal is called a/an ________.

(Multiple Choice)

4.8/5 (36)

TABLE 15.2

Use the information to answer following question(s).

-Refer to Table 15.2. Which of the following swap agreements could work for Shell and Merck with Barclay's as the facilitating bank?

-Refer to Table 15.2. Which of the following swap agreements could work for Shell and Merck with Barclay's as the facilitating bank?

(Multiple Choice)

4.8/5 (48)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. Choosing strategy #1 will

(Multiple Choice)

4.8/5 (31)

TABLE 15.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer Table 15.1. What portion of the cost of the loan is at risk of changing?

(Multiple Choice)

4.9/5 (31)

TABLE 15.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer Table 15.1. Polaris could have locked in the future interest rate payments by using

(Multiple Choice)

4.8/5 (42)

A firm with variable-rate debt that expects interest rates to rise may engage in a swap agreement to

(Multiple Choice)

4.8/5 (32)

Polaris Inc. has a significant amount of bonds outstanding denominated in yen because of the attractive variable rate available to the firm in yen when the loan was made. However, Polaris does not have significant receivables in yen. Options available to Polaris to consider the risk of such a loan include which one of the following?

(Multiple Choice)

4.7/5 (34)

An agreement to exchange interest payments based on a fixed payment for those based on a variable rate (or vice versa) is known as a/an ________.

(Multiple Choice)

4.8/5 (44)

Which of the following is NOT true regarding a corporate policy?

(Multiple Choice)

4.8/5 (42)

Counterparty risk is greater for exchange-traded derivatives than for over-the-counter derivatives.

(True/False)

4.9/5 (32)

Your firm is faced with paying a variable rate debt obligation with the expectation that interest rates are likely to go up. Identify two strategies using interest rate futures and interest rate swaps that could reduce the risk to the firm.

(Essay)

5.0/5 (34)

A/an ________ is a contract to lock in today interest rates over a given period of time.

(Multiple Choice)

4.9/5 (41)

Cross currency swaps typically have larger swings in total value than "plain vanilla" interest rate swaps because

(Multiple Choice)

4.9/5 (28)

________ is the possibility that the borrower's creditworthiness is reclassified by the lender at the time of renewing credit. ________ is the risk of changes in interest rates charged at the time a financial contract rate is set.

(Multiple Choice)

5.0/5 (31)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. Choosing strategy #3 will

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)