Exam 15: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Enterprise31 Questions

Exam 2: Financial Goals and Corporate Governance51 Questions

Exam 3: The International Monetary System60 Questions

Exam 4: The Balance of Payments63 Questions

Exam 5: The Foreign Exchange Market60 Questions

Exam 6: International Parity Conditions67 Questions

Exam 7: Foreign Exchange Rate Determination and Forecasting51 Questions

Exam 8: Foreign Currency Derivatives57 Questions

Exam 9: Transaction Exposure56 Questions

Exam 10: Operating Exposure62 Questions

Exam 11: Translation Exposure59 Questions

Exam 12: Global Cost and Availability of Capital62 Questions

Exam 13: Sourcing Equity Capital Globally66 Questions

Exam 14: Financial Structure and International Debt58 Questions

Exam 15: Interest Rate and Currency Swaps63 Questions

Exam 16: International Portfolio Theory and Diversification58 Questions

Exam 17: Foreign Direct Investment Theory and Strategy47 Questions

Exam 18: Political Risk Assessment and Management56 Questions

Exam 19: Multinational Capital Budgeting60 Questions

Exam 20: International Trade Finance55 Questions

Exam 21: Multinational Tax Management52 Questions

Exam 22: Working Capital Management59 Questions

Select questions type

Some of the world's largest and most financially sound firms may borrow at variable rates less than LIBOR.

(True/False)

4.8/5  (36)

(36)

TABLE 15.2

Use the information to answer following question(s).

-Refer to Table 15.2. For a swap agreement structured by Barclay's to benefit both Shell and Merck, which of the following must be true?

-Refer to Table 15.2. For a swap agreement structured by Barclay's to benefit both Shell and Merck, which of the following must be true?

(Multiple Choice)

4.8/5 (30)

A swap agreement may involve currencies or interest rates, but never both.

(True/False)

4.8/5 (45)

Graham Investments must pay floating rate interest 6 months from now. The firm can lock in the rate by buying an interest rate futures contract. Interest rate futures for 6 months from today are currently settled at 95.03 for a yield of 4.97% per annum. If the floating interest rate 6 months from now is 6%, how much did Graham gain or lose?

(Multiple Choice)

5.0/5 (42)

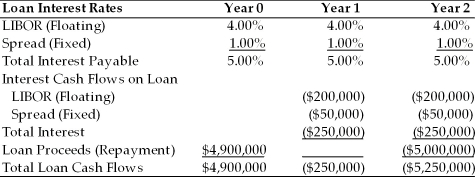

TABLE 15.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer Table 15.1. If the LIBOR rate falls to 3.00% after the first year what will be the all-in-cost (i.e. the internal rate of return) for Polaris for the entire loan?

-Refer Table 15.1. If the LIBOR rate falls to 3.00% after the first year what will be the all-in-cost (i.e. the internal rate of return) for Polaris for the entire loan?

(Multiple Choice)

4.8/5 (31)

Which of the following would be considered an example of a currency swap?

(Multiple Choice)

5.0/5 (31)

The interest rate swap strategy of a firm with fixed rate debt and that expects rates to go up is to

(Multiple Choice)

4.9/5 (37)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #3 is (Assume your firm is borrowing money.)

(Multiple Choice)

4.7/5 (54)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. After the fact, under which set of circumstances would you prefer strategy #1? (Assume your firm is borrowing money.)

(Multiple Choice)

4.9/5 (35)

The financial manager of a firm has a variable rate loan outstanding. If she wishes to protect the firm against an unfavorable increase in interest rates she could

(Multiple Choice)

4.9/5 (39)

The largest amount of daily trading in the foreign exchange derivatives market occurs in which of the following types of securities?

(Multiple Choice)

4.7/5 (42)

How does counterparty risk influence a firm's decision to trade exchange-traded derivatives rather than over-the-counter derivatives?

(Essay)

5.0/5 (33)

Historically, interest rate movements have shown less variability and greater stability than exchange rate movements.

(True/False)

4.8/5 (40)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. After the fact, under which set of circumstances would you prefer strategy #2? (Assume your firm is borrowing money.)

(Multiple Choice)

4.9/5 (42)

A combined position of selling one currency forward at one maturity while buying the same currency forward at a different maturity to lock in a future interest rate in the foreign currency is a/an

(Multiple Choice)

5.0/5 (28)

An agreement to swap a fixed interest payment for a floating interest payment would be considered a/an ________.

(Multiple Choice)

4.9/5 (32)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. Which strategy (strategies) will eliminate credit risk?

(Multiple Choice)

4.8/5 (36)

Molson Brewery, a Canadian company wishes to borrow $1,000,000 for 12 weeks. A rate of 6.00% per annum is quoted by lenders in both New York and London using, respectively, international and British definitions of interest. From which source should Molson borrow other things equal? What is Molson's total interest charge from the selected source?

(Multiple Choice)

4.7/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)