Exam 15: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Enterprise31 Questions

Exam 2: Financial Goals and Corporate Governance51 Questions

Exam 3: The International Monetary System60 Questions

Exam 4: The Balance of Payments63 Questions

Exam 5: The Foreign Exchange Market60 Questions

Exam 6: International Parity Conditions67 Questions

Exam 7: Foreign Exchange Rate Determination and Forecasting51 Questions

Exam 8: Foreign Currency Derivatives57 Questions

Exam 9: Transaction Exposure56 Questions

Exam 10: Operating Exposure62 Questions

Exam 11: Translation Exposure59 Questions

Exam 12: Global Cost and Availability of Capital62 Questions

Exam 13: Sourcing Equity Capital Globally66 Questions

Exam 14: Financial Structure and International Debt58 Questions

Exam 15: Interest Rate and Currency Swaps63 Questions

Exam 16: International Portfolio Theory and Diversification58 Questions

Exam 17: Foreign Direct Investment Theory and Strategy47 Questions

Exam 18: Political Risk Assessment and Management56 Questions

Exam 19: Multinational Capital Budgeting60 Questions

Exam 20: International Trade Finance55 Questions

Exam 21: Multinational Tax Management52 Questions

Exam 22: Working Capital Management59 Questions

Select questions type

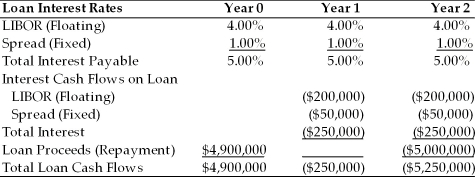

TABLE 15.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer Table 15.1. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return) for Polaris for the entire loan?

-Refer Table 15.1. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return) for Polaris for the entire loan?

(Multiple Choice)

4.8/5  (39)

(39)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. Choosing strategy #2 will

(Multiple Choice)

4.9/5 (38)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. If your firm felt very confident that interest rates would fall or, at worst, remain at current levels, and were very confident about the firm's credit rating for the next 10 years, which strategy would you likely choose? (Assume your firm is borrowing money.)

(Multiple Choice)

4.8/5 (28)

As a management tool, a ________ is a rule, but a ________ is an objective.

(Multiple Choice)

4.7/5 (30)

The potential exposure that any individual firm bears that the second party to any financial contract will be unable to fulfill its obligations under the contract is called ________.

(Multiple Choice)

4.7/5 (30)

Unlike the situation with exchange rate risk, there is no uncertainty on the part of management for shareholder preferences regarding interest rate risk. Shareholders prefer that managers hedge interest rate risk rather than having shareholders diversify away such risk through portfolio diversification.

(True/False)

4.8/5 (35)

A preferred interest rate swap strategy for a firm with variable-rate debt and that expects rates to go up is to

(Multiple Choice)

4.8/5 (42)

TABLE 15.2

Use the information to answer following question(s).

-Refer to Table 15.2. Which of the following are viable rates for the swap agreements with Barclay's Bank by Shell and Merck?

-Refer to Table 15.2. Which of the following are viable rates for the swap agreements with Barclay's Bank by Shell and Merck?

(Multiple Choice)

4.8/5 (40)

A U.S.-based firm with dollar denominated debt, but continuing sales denominated in Japanese yen, could

(Multiple Choice)

4.9/5 (36)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #2 is (Assume your firm is borrowing money.)

(Multiple Choice)

4.8/5 (40)

Over the last decade floating-rate notes have decreased in both total volume and percentage of total dollar-denominated bond issuances.

(True/False)

4.8/5 (37)

A firm entering into a currency or interest rate swap agreement is relieved of the ultimate responsibility for the timely servicing of its own debt obligations.

(True/False)

4.9/5 (41)

An agreement to swap the currencies of a debt service obligation would be termed a/an ________.

(Multiple Choice)

4.8/5 (43)

The single largest interest rate risk of a firm is ________.

(Multiple Choice)

4.8/5 (31)

A firm with fixed-rate debt that expects interest rates to fall may engage in a swap agreement to

(Multiple Choice)

4.8/5 (36)

Instruction 15.1:

For following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%,

to be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the

credit annually. The current one-year rate is 5%.

-Refer to Instruction 15.1. After the fact, under which set of circumstances would you prefer strategy #3? (Assume your firm is borrowing money.)

(Multiple Choice)

4.8/5 (35)

OTC interest rate derivative daily turnover has declined over the last decade in part due to the threat of terrorism and high energy prices.

(True/False)

4.9/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)