Exam 25: Oligopoly

Exam 1: Introduction12 Questions

Exam 2: A Consumers Economic Circumstances26 Questions

Exam 3: Economic Circumstances in Labor and Financial Markets15 Questions

Exam 4: Tastes and Indifference Curves17 Questions

Exam 5: Different Types of Tastes20 Questions

Exam 6: Doing the Best We Can20 Questions

Exam 7: Income and Substitution Effects in Consumer Goods Markets27 Questions

Exam 8: Wealth and Substitution Effects in Labor and Capital Markets19 Questions

Exam 9: Demand for Goods and Supply of Labor and Capital24 Questions

Exam 10: Consumer Surplus and Deadweight Loss28 Questions

Exam 11: One Input and One Output: a Short-Run Producer Model34 Questions

Exam 12: Production With Multiple Inputs34 Questions

Exam 13: Production Decisions in the Short and Long Run31 Questions

Exam 14: Competitive Market Equilibrium24 Questions

Exam 15: The Invisible Hand and the First Welfare Theorem24 Questions

Exam 16: General Equilibrium25 Questions

Exam 17: Choice and Markets in the Presence of Risk26 Questions

Exam 18: Elasticities, Price-Distorting Policies, and Non-Price Rationing28 Questions

Exam 19: Distortionary Taxes and Subsidies32 Questions

Exam 20: Prices and Distortions Across Markets22 Questions

Exam 21: Externalities in Competitive Markets25 Questions

Exam 22: Asymmetric Information in Competitive Markets24 Questions

Exam 23: Monopoly38 Questions

Exam 24: Strategic Thinking and Game Theory37 Questions

Exam 25: Oligopoly22 Questions

Exam 26: Product Differentiation and Innovation in Markets16 Questions

Exam 27: Public Goods21 Questions

Exam 28: Governments and Politics19 Questions

Exam 29: What Is Good Challenges From Psychology and Philosophy23 Questions

Select questions type

A firm that is the only firm in the industry may not behave like a monopolist in order to deter entry of other firms.

Free

(True/False)

4.8/5  (37)

(37)

Correct Answer: Verified

Verified

True

Just because a firm can deter entry by a competitor does not mean it will deter entry.

Free

(True/False)

4.9/5 (33)

Correct Answer:Verified

True

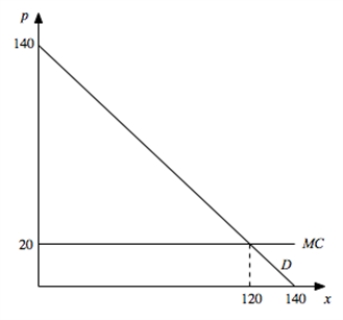

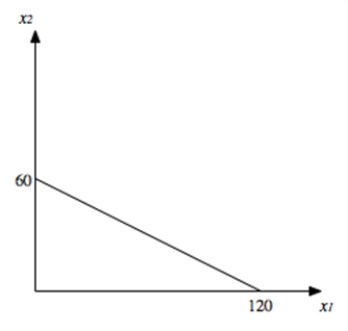

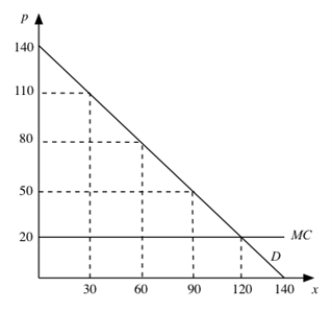

Suppose a single firm has constant marginal cost and faced the demand curve  a.Illustrate in this graph how a monopolist who cannot price discriminate would price this good.What is the monopoly price and quantity?

b.Suppose two firms with the same marginal cost as the monopolist operated in this market instead.Suppose quantity is the strategic variable and the two firms simultaneously choose quantity.On a graph with firm 1's output on the horizontal and firm 2's output on the vertical, illustrate firm 2's best response function with numerical labels for each intercept.

c.Add firm 1's best response function and determine the Nash equilibrium quantities.

d.What's the equilibrium price resulting from the quantities you determined in (c)?

e.What would be the equilibrium price if the strategic variable for the firms were price instead?

a.Illustrate in this graph how a monopolist who cannot price discriminate would price this good.What is the monopoly price and quantity?

b.Suppose two firms with the same marginal cost as the monopolist operated in this market instead.Suppose quantity is the strategic variable and the two firms simultaneously choose quantity.On a graph with firm 1's output on the horizontal and firm 2's output on the vertical, illustrate firm 2's best response function with numerical labels for each intercept.

c.Add firm 1's best response function and determine the Nash equilibrium quantities.

d.What's the equilibrium price resulting from the quantities you determined in (c)?

e.What would be the equilibrium price if the strategic variable for the firms were price instead?

Free

(Essay)

4.7/5 (40)

Correct Answer:Verified

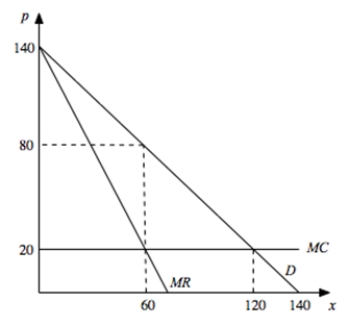

a. Price=80; Quantity = 60.  b.

b.  c.

c.  d. The equilibrium price is 60. (This is just read off the demand curve for output of 80.)

d. The equilibrium price is 60. (This is just read off the demand curve for output of 80.)

e. This would be Bertrand competition under which price is equal to MC -- i.e. p=20 and total output is 120.

Suppose that a market is currently served by a single firm protected by high entry costs from any potential competition.Then imagine fixed entry costs gradually falling in a model where any competition will be with quantity as the strategic variable.Describe how you would expect output price to evolve as entry costs fall.

(Essay)

5.0/5 (32)

If two simultaneous move Bertrand price competitors have different constant marginal costs, then any price between their marginal costs could be a Nash equilibrium price.

(True/False)

4.9/5 (38)

We showed that, when demand is linear and marginal cost is constant, the Stackelberg leader produces the monopoly output while the Stackelberg follower produces half the monopoly output.If the leader and follower now enter a simultaneous quantity setting game, why can't the leader maintain the same equilibrium?

(Essay)

4.9/5 (39)

Explain how two Bertrand price competitors can price above marginal cost in an infinitely repeated game setting.

(Essay)

4.7/5 (42)

Suppose a market is currently served by an incumbent firm.If a potential entrant can enter prior to the incumbent firm announcing its output (or price), the incumbent cannot deter entry through its actions.

(True/False)

4.9/5 (41)

Two firms in an oligopoly can always do better if one firm buys the other.

(True/False)

4.9/5 (36)

Suppose a market is currently served by an incumbent firm.If a potential entrant can enter prior to the incumbent firm announcing its output (or price), the entrant will enter the market and force the incumbent to compete.

(True/False)

4.9/5 (30)

If Bertrand price competitors incur recurring fixed costs, it will still be a Nash equilibrium for price to equal marginal cost.

(True/False)

4.8/5 (31)

If two firms in an oligopoly produce undifferentiated products and face identical constant marginal costs, then, absent any implicit or explicit collusion, they will price at marginal cost regardless of whether they move sequentially or simultaneously -- assuming price is the strategic variable.

(True/False)

4.8/5 (38)

The more firms there are in an oligopoly in which the strategic firm variable is quantity, the more price converges to marginal cost.

(True/False)

4.9/5 (32)

Suppose two Bertrand price competitors have different constant marginal costs.In any simultaneous move Nash equilibrium, only the lower cost firm will produce.

(True/False)

4.8/5 (33)

Suppose the market demand curve is as depicted in the graph, and all firms have constant

1

1

24

////AA==

marginal costs of 20.Assume that consumer tastes in x are quasilinear.  a.If a single monopolist who does not price discriminate serves this market, what is the value of consumer surplus and monopoly profit?

b.Suppose the government imposes a price ceiling of 40 on the monopolist from part (a).How does this change the value of consumer surplus and monopoly profit?

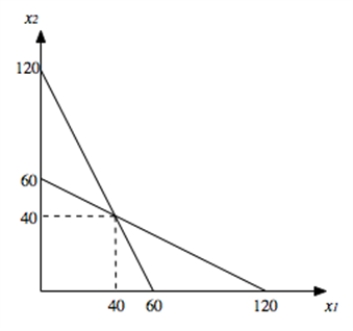

c.Suppose instead that this market has two Cournot competitors.Illustrate their best-response functions (labeling intercepts and slopes) as well as the Nash equilibrium.What is the value of consumer surplus and profit in the market now?

d.If the same price ceiling of 40 is imposed on the Cournot oligopoly, how will the best response functions change? (Assume that, if there is a good that is produced but does not get bought, it is equally likely that firm 1 gets stuck with the good as it is that firm 2 gets stuck with it, and it costs at least a penny to dispose of a good you are stuck with.) Is there more than one possible Nash equilibrium?

e.Will overall surplus increase?

f.Does your answer to (e) change if the price ceiling is imposed on Bertrand price competitors?

g.True or False: Whenever price ceilings impact the price at which goods are traded, they disturb the price signal and therefore result in deadweight losses.

a.If a single monopolist who does not price discriminate serves this market, what is the value of consumer surplus and monopoly profit?

b.Suppose the government imposes a price ceiling of 40 on the monopolist from part (a).How does this change the value of consumer surplus and monopoly profit?

c.Suppose instead that this market has two Cournot competitors.Illustrate their best-response functions (labeling intercepts and slopes) as well as the Nash equilibrium.What is the value of consumer surplus and profit in the market now?

d.If the same price ceiling of 40 is imposed on the Cournot oligopoly, how will the best response functions change? (Assume that, if there is a good that is produced but does not get bought, it is equally likely that firm 1 gets stuck with the good as it is that firm 2 gets stuck with it, and it costs at least a penny to dispose of a good you are stuck with.) Is there more than one possible Nash equilibrium?

e.Will overall surplus increase?

f.Does your answer to (e) change if the price ceiling is imposed on Bertrand price competitors?

g.True or False: Whenever price ceilings impact the price at which goods are traded, they disturb the price signal and therefore result in deadweight losses.

(Essay)

4.8/5 (36)

In a 2-firm oligopoly, if you can choose to either be a simultaneous move Cournot competitor or a Stackelberg leader, you will always choose to be a Stackelberg leader.

(True/False)

4.9/5 (39)

Cartels tend not to be long-lived because of the Prisoner's Dilemma.

(True/False)

4.7/5 (39)

Recurring fixed costs may lead to only one firm producing in a Cournot oligopoly model.

(True/False)

4.9/5 (43)

Firms in a cartel have an incentive to cheat on the cartel agreement because they suspect the other firms are cheating as well.

(True/False)

4.8/5 (20)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)