Exam 11: Decision Making With a Strategic Emphasis

Exam 1: Cost Management and Strategy79 Questions

Exam 2: Implementing Strategy: the Value Chain, the Balanced Scorecard, and the Strategy Map70 Questions

Exam 3: Basic Cost Management Concepts98 Questions

Exam 4: Job Costing118 Questions

Exam 5: Activity-Based Costing and Customer Profitability Analysis149 Questions

Exam 6: Process Costing106 Questions

Exam 7: Cost Allocation: Departments, Joint Products, and By-Products96 Questions

Exam 8: Cost Estimation120 Questions

Exam 9: Short-Term Profit Planning: Cost-Volume-Profit Cvp Analysis105 Questions

Exam 10: Strategy and the Master Budget146 Questions

Exam 11: Decision Making With a Strategic Emphasis137 Questions

Exam 12: Strategy and the Analysis of Capital Investments167 Questions

Exam 13: Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing94 Questions

Exam 14: Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures178 Questions

Exam 15: Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management167 Questions

Exam 16: Operational Performance Measurement: Further Analysis of Productivity and Sales134 Questions

Exam 17: The Management and Control of Quality147 Questions

Exam 18: Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard133 Questions

Exam 19: Strategic Performance Measurement: Investment Centers and Transfer Pricing151 Questions

Exam 20: Management Compensation, Business Analysis, and Business Valuation108 Questions

Select questions type

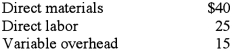

Motor Corp. manufactures machine parts for boat engines. The CEO, James Hamilton, was considering an offer from a subcontractor who would provide 3,000 units of product AB100 for Hamilton for a price of $230,000. If Motor Corp. does not purchase these parts from the subcontractor it must produce them in-house with the following per-unit costs:  In addition to the above costs, if Hamilton produces part AB100, he would also have a retooling and design cost of $10,000. Should Motor Corp. accept the offer from the subcontractor?

In addition to the above costs, if Hamilton produces part AB100, he would also have a retooling and design cost of $10,000. Should Motor Corp. accept the offer from the subcontractor?

(Essay)

4.8/5  (44)

(44)

Quinta Inc. manufactures machine parts for aircraft engines. The CEO is considering an offer from a subcontractor who would provide 2,800 units of product QR128 for a price of $190,000. If Quinta does not purchase these parts from the subcontractor it must produce them in-house with the following costs:  In addition to the above costs, if Quinta produces part QR128, there would also be a retooling and design cost of $13,000. Should Quinta Inc. accept the offer from the subcontractor?

In addition to the above costs, if Quinta produces part QR128, there would also be a retooling and design cost of $13,000. Should Quinta Inc. accept the offer from the subcontractor?

(Essay)

4.8/5 (41)

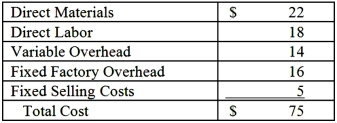

Plainfield Company manufactures part G for use in its production cycle. The costs per unit for 10,000 units of part G are as follows:  Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit. If Plainfield accepts Verona's offer, the released facilities could be used to save $45,000 in relevant costs in the manufacture of part H. In addition, $5 per unit of the fixed overhead applied to part G would be totally eliminated. What alternative is more desirable and by what amount?

Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit. If Plainfield accepts Verona's offer, the released facilities could be used to save $45,000 in relevant costs in the manufacture of part H. In addition, $5 per unit of the fixed overhead applied to part G would be totally eliminated. What alternative is more desirable and by what amount?

(Multiple Choice)

4.7/5 (39)

The make-or-buy decision can apply to decisions about all of the following except:

(Multiple Choice)

5.0/5 (31)

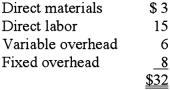

Quirch Inc. manufactures machine parts for aircraft engines. The CEO, Chucky Valters, was considering an offer from a subcontractor who would provide 2,400 units of product PQ107 for Valters for a price of $150,000. If Quirch does not purchase these parts from the subcontractor it must produce them in-house with the following costs:  In addition to the above costs, if Quirch produces part PQ107, it would also have a retooling and design cost of $9,800. The relevant costs of producing 2,400 units of product PQ107 are:

In addition to the above costs, if Quirch produces part PQ107, it would also have a retooling and design cost of $9,800. The relevant costs of producing 2,400 units of product PQ107 are:

(Multiple Choice)

4.9/5 (34)

Relevant costs in a make-vs.-buy decision of a part include:

(Multiple Choice)

4.8/5 (36)

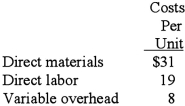

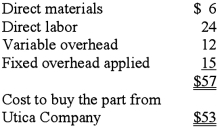

Kingston Company, which needs 10,000 units of a certain part to be used in its production cycle, can make or buy the part. If Kingston buys the part from Utica Company, Kingston could not use the released facilities in another manufacturing activity within the coming year. 60% of the fixed overhead applied will continue regardless of which decision is made. The following information is available: Cost to Kingston to make the part:  In deciding whether to make or buy the part, Kingston's total relevant costs to make the part are:

In deciding whether to make or buy the part, Kingston's total relevant costs to make the part are:

(Multiple Choice)

4.8/5 (39)

In a sell-or-process-further decision, joint production costs:

(Multiple Choice)

4.9/5 (40)

Which of the following items does NOT have to be considered when evaluating a make-or-buy decision?

(Multiple Choice)

4.8/5 (38)

If the plugs are purchased and the facility rented, Regis Company wishes to realize $100,000 in net savings annually. To achieve this goal, the minimum annual rent on the facility must be:

(Multiple Choice)

4.9/5 (42)

Feel the Difference, Inc. manufactures bath and beauty products such as soaps, skin creams, lotions, and other products primarily for people with dry and sensitive skin. It has just introduced a new line of product that removes the spotting and wrinkling in skin associated with aging. It sells these products in pharmacies and department stores at prices slightly higher than those of other brands because of Feel the Difference's excellent reputation for quality and effectiveness.

Feel the Difference currently has very low utilization of plant capacity. Two years ago, in anticipation of rapid growth, the company opened a new large manufacturing plant, which has yet to be utilized more than 50 percent. Partly for this reason, Feel the Difference has sought new partners and was able, with the help of financial analysts, to locate suitable business partners. The first potential partner identified in this search was a large supermarket chain, All-Mart, which is interested in the partnership because it wants Feel the Difference to manufacture an age cream to sell in its stores. The product would be essentially the same as the Feel the Difference product but would be packaged in the All-Mart brand name. The agreement would pay Feel the Difference $2.00 per unit and would allow All-Mart a limited right to advertise the product as manufactured for All-Mart by Feel the Difference. Feel the Difference's CFO has made some calculations and has determined that the direct materials, direct labor and other variable costs needed for the All-Mart order would be about $1.00 per unit as compared to the full cost of $2.50 (materials, labor, and overhead) for the equivalent Feel the Difference product.

Required:

Should Feel the Difference accept the proposal from All-Mart? Why or why not? (Include strategic considerations)

(Essay)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)