Exam 14: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Firm98 Questions

Exam 2: International Monetary System100 Questions

Exam 3: Balance of Payments100 Questions

Exam 4: Corporate Governance Around the World100 Questions

Exam 5: The Market for Foreign Exchange100 Questions

Exam 6: International Parity Relationships and Forecasting Foreign Exchange Rates100 Questions

Exam 7: Futures and Options on Foreign Exchange100 Questions

Exam 8: Management of Transaction Exposure100 Questions

Exam 9: Management of Economic Exposure100 Questions

Exam 10: Management of Translation Exposure81 Questions

Exam 11: International Banking and Money Market101 Questions

Exam 12: International Bond Market100 Questions

Exam 13: International Equity Markets99 Questions

Exam 14: Interest Rate and Currency Swaps100 Questions

Exam 15: International Portfolio Investment101 Questions

Exam 16: Foreign Direct Investment and Cross-Border Acquisitions100 Questions

Exam 17: International Capital Structure and the Cost of Capital99 Questions

Exam 18: International Capital Budgeting101 Questions

Exam 19: Multinational Cash Management100 Questions

Exam 20: International Trade Finance100 Questions

Exam 21: International Tax Environment and Transfer Pricing100 Questions

Select questions type

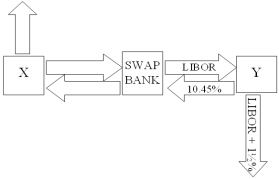

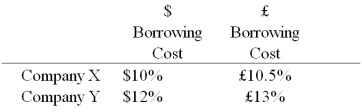

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are shown below:  A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05%-10.45% against LIBOR flat. Assume company Y has agreed,but company X will only agree to the swap if the bank offers better terms.

What are the absolute best terms the bank can offer X,given that it already booked Y?

A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05%-10.45% against LIBOR flat. Assume company Y has agreed,but company X will only agree to the swap if the bank offers better terms.

What are the absolute best terms the bank can offer X,given that it already booked Y?

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

A

A swap bank has identified two companies with mirror-image financing needs (they both want to borrow equivalent amounts for the same amount of time.Company X has agreed to one leg of the swap but company Y is "playing hard to get".

Free

(Multiple Choice)

4.9/5 (30)

Correct Answer:Verified

D

A major that can be eliminated through a swap is exchange rate risk.

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

A

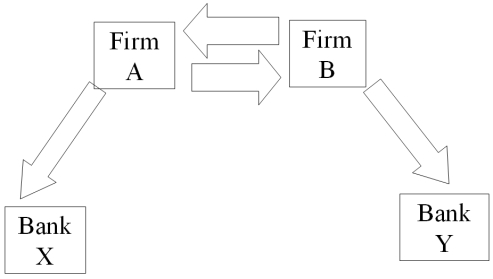

Explain how firm B could use the forward exchange markets to redenominate a 2-year €40m 5% euro loan into a 2-year USD-denominated loan.

(Essay)

4.9/5 (40)

Show how your proposed swap would work for firm A.(e.g.if you were acting as an agent for the swap bank,try to "sell" firm A on your swap)

I would point out that his contracting costs would be less with just having 1 swap instead of 2 forward contracts.Also,he might be able to get a better rate through the swap if he can't find forward contracts at his desired maturity and amounts.

(Essay)

4.9/5 (33)

When an interest-only swap is established on an amortizing basis

(Multiple Choice)

4.8/5 (36)

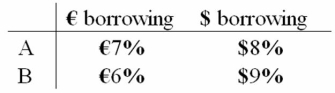

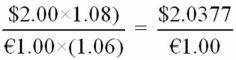

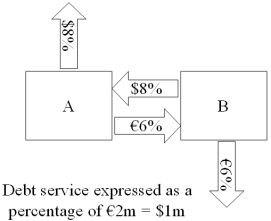

Consider the dollar- and euro-based borrowing opportunities of companies A and B .  A is a U.S.-based MNC with AAA credit; B is an Italian firm with AAA credit.Firm A wants to borrow €1,000,000 for one year and B wants to borrow $2,000,000 for one year.The spot exchange rate is $2.00 = €1.00 and the one-year forward rate is given by IRP as:

A is a U.S.-based MNC with AAA credit; B is an Italian firm with AAA credit.Firm A wants to borrow €1,000,000 for one year and B wants to borrow $2,000,000 for one year.The spot exchange rate is $2.00 = €1.00 and the one-year forward rate is given by IRP as:  .Suppose they agree to the swap shown at right.Is this mutually beneficial swap equally fair to both parties?

.Suppose they agree to the swap shown at right.Is this mutually beneficial swap equally fair to both parties?

(Multiple Choice)

4.9/5 (42)

Explain how firm B could use two of the swaps offered above to hedge its exchange rate risk.

(Essay)

4.9/5 (34)

Devise a direct swap for A and B that has no swap bank.Show their external borrowing.Answer the problem in the template provided.

(Essay)

4.8/5 (43)

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow £5,000,000 fixed for 5 years.The exchange rate is $2 = £1 and is not expected to change over the next 5 years.Their external borrowing opportunities are:  A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap.In order for X and Y to be interested,they can face no exchange rate risk

A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap.In order for X and Y to be interested,they can face no exchange rate risk  What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

(Multiple Choice)

4.8/5 (41)

Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 7% USD loan into a 2-year euro denominated loan.

(Essay)

4.8/5 (45)

Company X and company Y have mirror-image financing needs (they both want to borrow equivalent amounts for the same amount of time.Company X has a AAA credit rating,but company Y's credit standing is considerably lower.

(Multiple Choice)

4.8/5 (26)

Act as a swap bank and quote bid and ask prices to A and B that are attractive to A and B and promise to make at least 20bp for your firm.

(Essay)

4.8/5 (24)

In an efficient market without barriers to capital flows,the cost-savings argument of the QSD is difficult to accept,because

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)