Exam 14: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Firm98 Questions

Exam 2: International Monetary System100 Questions

Exam 3: Balance of Payments100 Questions

Exam 4: Corporate Governance Around the World100 Questions

Exam 5: The Market for Foreign Exchange100 Questions

Exam 6: International Parity Relationships and Forecasting Foreign Exchange Rates100 Questions

Exam 7: Futures and Options on Foreign Exchange100 Questions

Exam 8: Management of Transaction Exposure100 Questions

Exam 9: Management of Economic Exposure100 Questions

Exam 10: Management of Translation Exposure81 Questions

Exam 11: International Banking and Money Market101 Questions

Exam 12: International Bond Market100 Questions

Exam 13: International Equity Markets99 Questions

Exam 14: Interest Rate and Currency Swaps100 Questions

Exam 15: International Portfolio Investment101 Questions

Exam 16: Foreign Direct Investment and Cross-Border Acquisitions100 Questions

Exam 17: International Capital Structure and the Cost of Capital99 Questions

Exam 18: International Capital Budgeting101 Questions

Exam 19: Multinational Cash Management100 Questions

Exam 20: International Trade Finance100 Questions

Exam 21: International Tax Environment and Transfer Pricing100 Questions

Select questions type

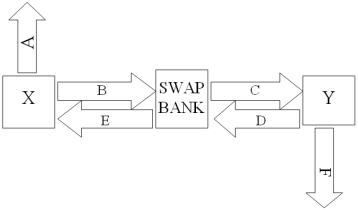

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are shown below:  A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05%-10.45% against LIBOR flat. Assume both X and Y agree to the swap bank's terms.

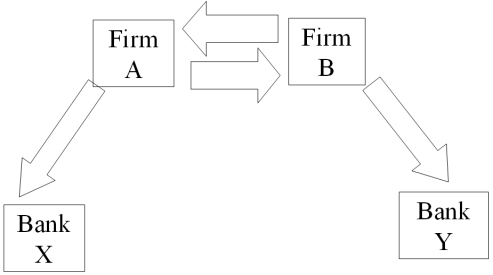

Fill in the values for A,B,C,D,E,& F on the diagram.

A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05%-10.45% against LIBOR flat. Assume both X and Y agree to the swap bank's terms.

Fill in the values for A,B,C,D,E,& F on the diagram.

(Multiple Choice)

4.7/5  (34)

(34)

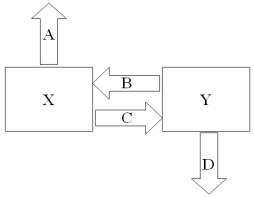

Company X wants to borrow $10,000,000 floating for 5 years.Company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are:  Design a mutually beneficial interest only swap for X and Y with a notational principal of $10 million by having appropriate values for A = Company X's external borrowing rate

B = Company Y's payment to X (rate)

C = Company X's payment to Y (rate)

D = Company Y's external borrowing rate

Design a mutually beneficial interest only swap for X and Y with a notational principal of $10 million by having appropriate values for A = Company X's external borrowing rate

B = Company Y's payment to X (rate)

C = Company X's payment to Y (rate)

D = Company Y's external borrowing rate

(Multiple Choice)

4.9/5 (40)

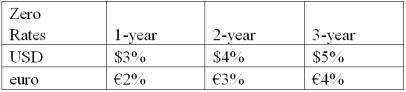

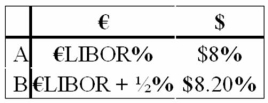

Suppose that you are a swap bank and you notice that interest rates on zero coupon bonds are as shown.Develop the 3-year bid price of a euro swap quoted against flat USD LIBOR.  In other words,what will you be willing to pay in euro against receiving USD LIBOR?

In other words,what will you be willing to pay in euro against receiving USD LIBOR?

(Multiple Choice)

4.8/5 (32)

A major risk faced by a swap dealer is mismatch risk.This is

(Multiple Choice)

4.8/5 (35)

Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4% pound sterling loan into a 2-year USD-denominated loan.

(Essay)

4.8/5 (36)

Come up with a swap (exchange of interest and principal)for parties A and B who have the following borrowing opportunities.  The current exchange rate is $1.60 = €1.00.Company "A" is in Milan,Italy and wishes to borrow $1,000,000 at a floating rate for 5 years and company "B" is a U.S.firm that wants to borrow €625,000 for 5 years at a fixed rate of interest.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.

The current exchange rate is $1.60 = €1.00.Company "A" is in Milan,Italy and wishes to borrow $1,000,000 at a floating rate for 5 years and company "B" is a U.S.firm that wants to borrow €625,000 for 5 years at a fixed rate of interest.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.

(Essay)

4.9/5 (30)

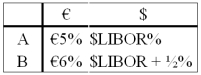

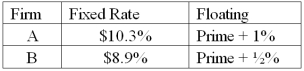

Consider a plain vanilla interest rate swap.Firm A can borrow at 8% fixed or can borrow floating at LIBOR.Firm B is somewhat less creditworthy and can borrow at 10% fixed or can borrow floating at LIBOR + 1%.Eun wants to borrow floating and Resnick prefers to borrow fixed.Both corporations wish to borrow $10 million for 5 years.Which of the following swaps is mutually beneficial to each party and meets their financing needs?

(Multiple Choice)

4.9/5 (34)

Devise a direct swap for A and B that has no swap bank.Show their external borrowing.Answer the problem in the template provided.

(Essay)

4.7/5 (30)

Explain how this opportunity affects which swap firm A will be willing to participate in.

(Essay)

4.8/5 (35)

Explain how this opportunity affects which swap firm A will be willing to participate in.

(Essay)

4.8/5 (37)

Suppose the quote for a five-year swap with semiannual payments is 8.50-8.60 percent in dollars and 6.60-6.80 percent in euro against six-month dollar LIBOR.This means

(Multiple Choice)

4.8/5 (37)

Come up with a swap (principal + interest)for two parties A and B who have the following borrowing opportunities.  The current exchange rate is $1.60 = €1.00.Company "A" wishes to borrow $1,000,000 for 5 years and "B" wants to borrow €625,000 for 5 years.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.Firms A and B are more concerned with what currency that they borrow in than whether the debt is fixed or floating.

The current exchange rate is $1.60 = €1.00.Company "A" wishes to borrow $1,000,000 for 5 years and "B" wants to borrow €625,000 for 5 years.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.Firms A and B are more concerned with what currency that they borrow in than whether the debt is fixed or floating.

(Essay)

4.9/5 (40)

Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4% pound sterling loan into a 2-year USD-denominated loan.

(Essay)

4.8/5 (42)

Consider the borrowing rates for Parties A and B.A wants to finance a $100,000,000 project at a FIXED rate.B wants to finance a $100,000,000 project at a FLOATING rate.Both firms want the same maturity,in 5 years.  Construct a mutually beneficial INTEREST ONLY swap that makes money for A,B,and the swap bank IN EQUAL MEASURE.

Construct a mutually beneficial INTEREST ONLY swap that makes money for A,B,and the swap bank IN EQUAL MEASURE.

(Essay)

4.8/5 (44)

Explain how this opportunity affects which swap firm B will be willing to participate in.

(Essay)

4.8/5 (36)

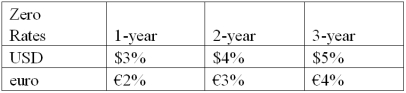

Suppose that you are a swap bank and you notice that interest rates on zero coupon bonds are as shown.Develop the 3-year bid price of a dollar swap quoted against flat USD LIBOR.  In other words,what will you be willing to pay in euro against receiving USD LIBOR?

In other words,what will you be willing to pay in euro against receiving USD LIBOR?

(Multiple Choice)

4.9/5 (47)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)