Exam 10: The Firm and the Industry Under Perfect Competition

Exam 1: What Is Economics227 Questions

Exam 2: The Economy: Myth and Reality150 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice250 Questions

Exam 4: Supply and Demand: An Initial Look308 Questions

Exam 5: Consumer Choice: Individual and Market Demand202 Questions

Exam 6: Demand and Elasticity207 Questions

Exam 7: Production,Inputs,and Cost: Building Blocks for Supply Analysis215 Questions

Exam 8: Output,Price,and Profit: The Importance of Marginal Analysis189 Questions

Exam 9: Securities: Business Finance,and the Economy: The Tail That Wags the Dog198 Questions

Exam 10: The Firm and the Industry Under Perfect Competition206 Questions

Exam 11: Monopoly204 Questions

Exam 12: Between Competition and Monopoly225 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust152 Questions

Exam 14: The Case for Free Markets I: the Price System219 Questions

Exam 15: The Shortcomings of Free Markets214 Questions

Exam 16: The Markets Prime Achievement: Innovation and Growth110 Questions

Exam 17: Externalities, the Environment, and Natural Resources217 Questions

Exam 18: Taxation and Resource Allocation219 Questions

Exam 19: Pricing the Factors of Production228 Questions

Exam 20: Labor and Entrepreneurship: The Human Inputs222 Questions

Exam 21: Poverty, Inequality, and Discrimination167 Questions

Exam 22: International Trade and Comparative Advantage226 Questions

Select questions type

Which of the following decisions cannot be taken by a firm in a perfectly competitive market?

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

B

The opportunity cost of a given investment is the potential earnings forfeited by tying up money in the investment.

Free

(True/False)

4.8/5 (37)

Correct Answer:Verified

True

Perfectly competitive markets feature relatively high barriers to entry.

Free

(True/False)

4.7/5 (37)

Correct Answer:Verified

False

Firms entering a perfectly competitive industry will cause the price of the product to

(Multiple Choice)

4.9/5 (35)

In a perfectly competitive industry,influence over price is exerted by

(Multiple Choice)

4.8/5 (33)

In the long run,any firm may enter or leave a perfectly competitive market.

(True/False)

4.9/5 (38)

The short-run supply curve of the perfectly competitive industry is found by summing the

(Multiple Choice)

4.8/5 (28)

The short-run supply curve for the perfectly competitive firm is that part of the marginal cost curve that lies above the average fixed cost curve.

(True/False)

4.9/5 (41)

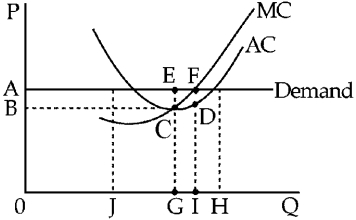

Figure 10-3

-In Figure 10-3,the perfectly competitive firm is realizing a

-In Figure 10-3,the perfectly competitive firm is realizing a

(Multiple Choice)

4.9/5 (33)

How does a firm that is losing money in the short run decide whether to shut down or continue to produce to minimize its losses?

(Essay)

4.7/5 (33)

What is the difference between the accountant's concept of profit and the economist's view of profit?

(Essay)

4.7/5 (32)

For a perfectly competitive firm,marginal revenue equals average revenue because the

(Multiple Choice)

4.8/5 (33)

Which of the following is a characteristic of perfect competition?

(Multiple Choice)

4.9/5 (37)

A firm can stay in business while taking a loss in the short run as long as it covers its

(Multiple Choice)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)