Exam 14: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Firm100 Questions

Exam 2: International Monetary System100 Questions

Exam 3: Balance of Payments100 Questions

Exam 4: Corporate Governance Around the World100 Questions

Exam 5: The Market for Foreign Exchange98 Questions

Exam 6: International Parity Relationships and Forecasting Foreign Exchange Rates100 Questions

Exam 7: Futures and Options on Foreign Exchange100 Questions

Exam 8: Management of Transaction Exposure98 Questions

Exam 9: Management of Economic Exposure100 Questions

Exam 10: Management of Translation Exposure81 Questions

Exam 11: International Banking and Money Market103 Questions

Exam 12: International Bond Market100 Questions

Exam 13: International Equity Markets100 Questions

Exam 14: Interest Rate and Currency Swaps100 Questions

Exam 15: International Portfolio Investment101 Questions

Exam 16: Foreign Direct Investment and Cross-Border Acquisitions100 Questions

Exam 17: International Capital Structure and the Cost of Capital100 Questions

Exam 18: International Capital Budgeting102 Questions

Exam 19: Multinational Cash Management100 Questions

Exam 20: International Trade Finance100 Questions

Exam 21: International Tax Environment and Transfer Pricing99 Questions

Select questions type

Explain how this opportunity affects which swap firm A will be willing to participate in.

(Essay)

5.0/5  (43)

(43)

When an interest-only swap is established on an amortizing basis

(Multiple Choice)

4.9/5 (36)

Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4% pound sterling loan into a 2-year USD-denominated loan.

(Essay)

4.9/5 (44)

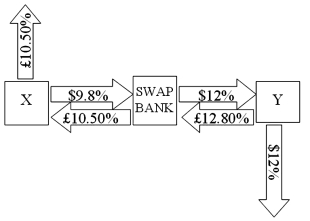

Company X wants to borrow $10,000,000 for 5 years; company Y wants to borrow £5,000,000 for 5 years. The exchange rate is $2 = £1 and is not expected to change over the next 5 years. Their external borrowing opportunities are shown below:  A swap bank proposes the following interest only swap: X will pay the swap bank annual payments on $10,000,000 with the coupon rate of 9.80%; in exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5%. Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12%.

A swap bank proposes the following interest only swap: X will pay the swap bank annual payments on $10,000,000 with the coupon rate of 9.80%; in exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5%. Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12%.  What is the value of this swap to the swap bank?

What is the value of this swap to the swap bank?

(Multiple Choice)

4.7/5 (34)

Suppose the quote for a five-year swap with semiannual payments is 8.50-8.60 percent. The means

(Multiple Choice)

4.8/5 (34)

Consider a plain vanilla interest rate swap. Firm A can borrow at 8% fixed or can borrow floating at LIBOR. Firm B is somewhat less creditworthy and can borrow at 10% fixed or can borrow floating at LIBOR + 1%. Eun wants to borrow floating and Resnick prefers to borrow fixed. Both corporations wish to borrow $10 million for 5 years. Which of the following swaps is mutually beneficial to each party and meets their financing needs?

(Multiple Choice)

4.8/5 (42)

Suppose that the swap that you proposed in question 2 is now 4 years old (i.e. there is exactly one year to go on the swap). The fourth payment has already been made. If the spot exchange rate prevailing in year 4 is $1.8778 = €1 and the 1-year forward exchange rate prevailing in year 4 is $1.95 = €1, what is the value of the swap to the party paying dollars? If the swap were initiated today the correct rates would be as shown:

(Essay)

4.8/5 (39)

Explain how this opportunity affects which swap firm B will be willing to participate in.

(Essay)

4.9/5 (40)

Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 6% USD loan into a 2-year pound denominated loan.

(Essay)

4.8/5 (37)

Consider the dollar- and euro-based borrowing opportunities of companies A and

(Multiple Choice)

4.9/5 (36)

Compute the payments due in the FIRST year on a three-year AMORTIZING swap from company B to company

A)B pays £402,114.80 to A

(Multiple Choice)

5.0/5 (37)

XYZ Corporation enters into a 6-year interest rate swap with a swap bank in which it agrees to pay the swap bank a fixed-rate of 9 percent annually on a notional amount of SFr10,000,000 and receive LIBOR - ½ percent. As of the third reset date (i.e. mid-way through the 6 year agreement), calculate the price of the swap, assuming that the fixed-rate at which XYZ can borrow has increased to 10%.

(Multiple Choice)

4.9/5 (39)

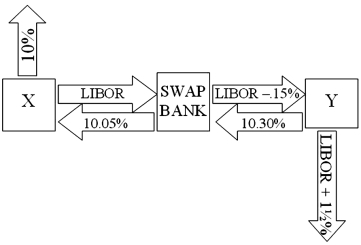

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown below:  A swap bank proposes the following interest only swap: X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of 10.05%. Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of LIBOR - 0.15%.

A swap bank proposes the following interest only swap: X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of 10.05%. Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of LIBOR - 0.15%.  What is the value of this swap to the swap bank?

What is the value of this swap to the swap bank?

(Multiple Choice)

4.8/5 (31)

Consider a fixed for fixed currency swap. The Dow Corporation is a U.S.-based multinational. The Jones Corporation is a U.K.-based multinational. Dow wants to finance a £2 million expansion in Great Britain. Jones wants to finance a $4 million expansion in the U.S. The spot exchange rate is £1.00 = $2.00. Dow can borrow dollars at $10% and pounds sterling at 12%. Jones can borrow dollars at 9% and pounds sterling at 10%. Assuming that the swap bank is willing to take on exchange rate risk, but the other counterparties are not, which of the following swaps is mutually beneficial to each party and meets their financing needs?

(Multiple Choice)

4.9/5 (34)

Consider bank that has entered into a five-year swap on a notational balance of $10,000,000 with a corporate customer who has agreed to pay a fixed payment of 10 percent in exchange for LIBOR. As of the fourth reset date, determine the price of the swap from the bank's point of view assuming that the fixed-rate side of the swap has increased to 11 percent. LIBOR is at 5 percent.

(Multiple Choice)

4.7/5 (37)

A swap bank makes the following quotes for 5-year swaps and AAA-rated firms:

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)