Exam 5: Interest Rate Risk Measurement: The Repricing Model

Exam 1: Why Are Financial Institutions Special66 Questions

Exam 2: The Financial Services Industry: Depository Institutions66 Questions

Exam 3: The Financial Services Industry: Other Financial Institutions56 Questions

Exam 4: Risk of Financial Institutions67 Questions

Exam 5: Interest Rate Risk Measurement: The Repricing Model69 Questions

Exam 6: Interest Rate Risk Measurement: The Duration Model64 Questions

Exam 7: Managing Interest Rate Risk Using Off Balance Sheet Instruments63 Questions

Exam 8: Credit Risk I: Individual Loan Risk65 Questions

Exam 9: Market Risk55 Questions

Exam 10: Credit Risk I: Individual Loan Risk66 Questions

Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk63 Questions

Exam 12: Sovereign Risk65 Questions

Exam 13: Foreign Exchange Risk63 Questions

Exam 14: Liquidity Risk65 Questions

Exam 15: Liability and Liquidity Management66 Questions

Exam 16: Off-Balance-Sheet Activities65 Questions

Exam 17: Technology and Other Operational Risk67 Questions

Exam 18: Capital Management and Adequacy66 Questions

Select questions type

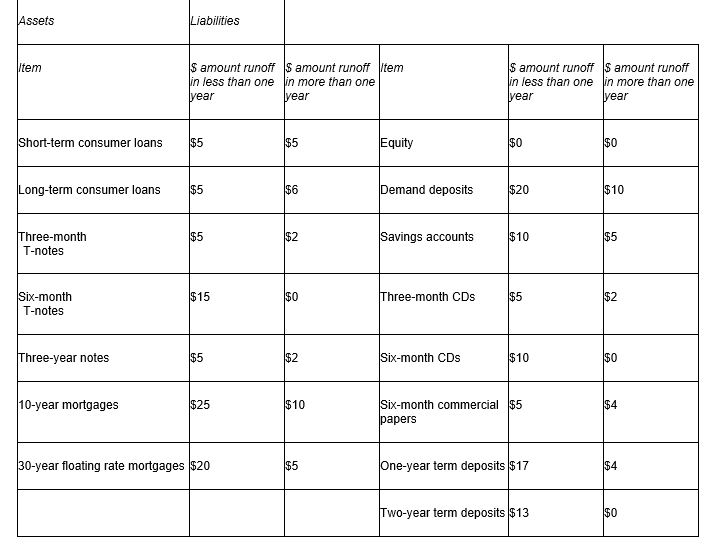

Consider the following table:  What is the one-year gap adjusted for runoffs?

What is the one-year gap adjusted for runoffs?

(Multiple Choice)

4.7/5  (35)

(35)

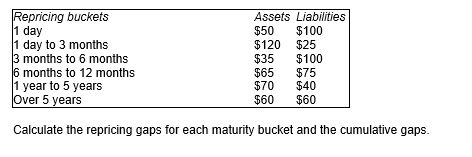

In the last quarter ABC Bank reported the following repricing buckets:

(Essay)

4.9/5 (42)

An FI with a neutral repricing gap in its three to six month bucket is hedged against any interest rate changes at all points in time.

(True/False)

4.9/5 (30)

If the spread between rate sensitive assets and rate sensitive liabilities increases for a bank, future changes in interest rates will lead to an increase in net interest income.

(True/False)

4.8/5 (32)

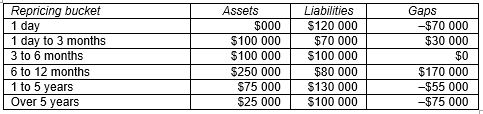

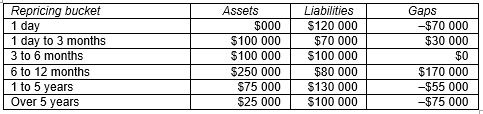

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

A)-$700

B)$700

C)-$7000

D)$700

What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

A)-$700

B)$700

C)-$7000

D)$700

(Essay)

4.8/5 (33)

An FI with a positive gap of $30 million suffers a $0.15 million decrease in its net interest income if interest rates increase by 0.5 per cent.

(True/False)

4.8/5 (39)

The Reserve Bank of Australia's (RBA) undertook actions in regards to their open market operation in the post global financial crisis environment to move financial markets towards greater stability.This was achieved by:

A)increasing the maturity of repos to reduce money pressure in the money market over the longer term.

B)increasing RBA holdings of non-government securities for use with repos due to the shortage of government securities

C)increasing the supply of deposits held by banks and other authorised deposit-taking institutions in their exchange settlement accounts held with the RBA.

D)All of the listed options are correct.

(Essay)

4.8/5 (32)

Convexity is the major problem associated with the repricing gap.

(True/False)

4.8/5 (34)

The unbiased expectations theory of the term structure of interest rates:

(Multiple Choice)

4.7/5 (45)

The cumulative gap over the whole balance sheet by definition:

(Multiple Choice)

4.7/5 (32)

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

(Multiple Choice)

4.9/5 (41)

The cumulative repricing gap position of an FI for a given extended time period is the sum of the repricing gap values for the individual time periods that make up the extended time period.

(True/False)

4.8/5 (38)

When repricing all interest sensitive assets and all interest sensitive liabilities in a balance sheet, the cumulative gap will be:

(Multiple Choice)

4.8/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)