Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk

Exam 1: Why Are Financial Institutions Special66 Questions

Exam 2: The Financial Services Industry: Depository Institutions66 Questions

Exam 3: The Financial Services Industry: Other Financial Institutions56 Questions

Exam 4: Risk of Financial Institutions67 Questions

Exam 5: Interest Rate Risk Measurement: The Repricing Model69 Questions

Exam 6: Interest Rate Risk Measurement: The Duration Model64 Questions

Exam 7: Managing Interest Rate Risk Using Off Balance Sheet Instruments63 Questions

Exam 8: Credit Risk I: Individual Loan Risk65 Questions

Exam 9: Market Risk55 Questions

Exam 10: Credit Risk I: Individual Loan Risk66 Questions

Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk63 Questions

Exam 12: Sovereign Risk65 Questions

Exam 13: Foreign Exchange Risk63 Questions

Exam 14: Liquidity Risk65 Questions

Exam 15: Liability and Liquidity Management66 Questions

Exam 16: Off-Balance-Sheet Activities65 Questions

Exam 17: Technology and Other Operational Risk67 Questions

Exam 18: Capital Management and Adequacy66 Questions

Select questions type

Which of the following statements is true?

Free

(Multiple Choice)

4.8/5  (40)

(40)

Correct Answer: Verified

Verified

A

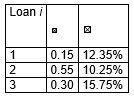

Consider the following table with information on the weightings and expected returns of three assets held by an FI.  What is the expected return on the portfolio (round to two decimals)?

What is the expected return on the portfolio (round to two decimals)?

Free

(Multiple Choice)

4.9/5 (36)

Correct Answer:Verified

C

The concentration limit for a loan portfolio is calculated as the expected default frequency of the borrower multiplied by (one divided by the loss rate).

Free

(True/False)

4.8/5 (32)

Correct Answer:Verified

True

Consider the following portfolio of assets:

What is the variance of the portfolio (round to two decimals)?

What is the variance of the portfolio (round to two decimals)?

(Multiple Choice)

4.8/5 (29)

Assume that an FI's concentration limit on a particular sector is 15 per cent and that the sector's loss rate is 25 per cent.What is the maximum loss as a percentage of the FI's capital (round to two decimals)?

(Multiple Choice)

4.8/5 (30)

Loan loss ratio based models estimate systematic loan losses by running a time-series regression of quarterly losses of the ith sector's loss rate on the quarterly loss rate of an FI's total loans.

(Essay)

4.7/5 (35)

Using the KMV Portfolio Manager Model, the return on a loan can be calculated as the annual all-in-spread minus the loss in the event of default.

(True/False)

4.9/5 (38)

Using the KMV Portfolio Manager Model, the risk on a loan can be calculated as the volatility of the loan's default rate times the loss in the event of default.

(True/False)

4.8/5 (35)

The most important swap contract in terms of quantity is the credit swap.

(True/False)

4.9/5 (31)

A transition matrix can be used to establish the probabilities that a currently rated borrower will be upgraded, downgraded or will default over time.

(True/False)

4.9/5 (32)

Loan sales and securitisation are increasingly seen as valuable tools in the management of credit risk.Which of the following are not advantageous to FIs?

(Multiple Choice)

4.8/5 (24)

Assume that the maximum loss as a percentage of capital is 12 per cent of an FI's capital to a particular sector.The FI's concentration limit on this sector 35 per cent.What is the sector's loss rate (round to two decimals)?

(Multiple Choice)

4.9/5 (33)

Financial institutions do not use options to hedge credit risk exposures as credit risk is a natural risk that comes with the core activities of the bank, namely lending.

(True/False)

4.8/5 (35)

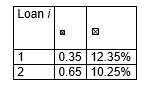

Consider the following table with information on the weightings and expected returns of two assets held by an FI.  What is the expected return on the portfolio (round to two decimals)?

What is the expected return on the portfolio (round to two decimals)?

(Multiple Choice)

5.0/5 (29)

Consider the following portfolio of assets:  What is the standard deviation of the portfolio (round to two decimals)?

A)(0.3)( 82.00) + (0.7)( 76.00) = 8.82%

B)( 82.00) + ( 76.00) = 17.77%

C) 15.75 = 3.97%

D) 48.93 = 6.99%

What is the standard deviation of the portfolio (round to two decimals)?

A)(0.3)( 82.00) + (0.7)( 76.00) = 8.82%

B)( 82.00) + ( 76.00) = 17.77%

C) 15.75 = 3.97%

D) 48.93 = 6.99%

(Essay)

4.8/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)