Exam 8: Risk and Return

Exam 1: The Role of Managerial Finance133 Questions

Exam 2: The Financial Market Environment91 Questions

Exam 3: Financial Statements and Ratio Analysis209 Questions

Exam 4: Cash Flow and Financial Planning183 Questions

Exam 5: Time Value of Money173 Questions

Exam 6: Interest Rates and Bond Valuation224 Questions

Exam 7: Stock Valuation188 Questions

Exam 8: Risk and Return190 Questions

Exam 9: The Cost of Capital137 Questions

Exam 10: Capital Budgeting Techniques167 Questions

Exam 11: Capital Budgeting Cash Flows117 Questions

Exam 12: Risk and Refinements in Capital Budgeting106 Questions

Exam 13: Leverage and Capital Structure217 Questions

Exam 14: Payout Policy130 Questions

Exam 15: Working Capital and Current Assets Management340 Questions

Exam 16: Current Liabilities Management171 Questions

Exam 17: Hybrid and Derivative Securities185 Questions

Exam 18: Mergers, Lbos, Divestitures, and Business Failure191 Questions

Exam 19: International Managerial Finance108 Questions

Select questions type

The portion of an asset's risk that is attributable to firm-specific, random causes is called

(Multiple Choice)

4.9/5  (38)

(38)

Market risk is the chance that the value of an investment will decline because of market factors (such as economic, political, and social events) that are independent of the investment.

(True/False)

4.7/5 (36)

The empirical measurement of beta can be approached by using least-squares regression analysis to find the regression coefficient (bj) in the equation for the slope of the "characteristic line."

(True/False)

4.7/5 (38)

An abnormal probability distribution is a symmetrical distribution whose shape resembles a bell-shaped curve.

(True/False)

4.9/5 (36)

The risk of a portfolio containing international stocks generally does not contain less nondiversifiable risk than one that contains only American stocks.

(True/False)

4.8/5 (39)

Financial risk is the chance that the firm will be unable to cover its operating costs and is affected by a firm's revenue stability and the structure of its operating costs (fixed vs. variable).

(True/False)

5.0/5 (33)

Nico bought 100 shares of Cisco Systems stock for $24.00 per share on January 1, 2002. He received a dividend of $2.00 per share at the end of 2002 and $3.00 per share at the end of 2003. At the end of 2004, Nico collected a dividend of $4.00 per share and sold his stock for $18.00 per share. What was Nico's realized holding period return?

(Multiple Choice)

4.7/5 (30)

Because any investor can create a portfolio of assets that will eliminate all, or virtually all, nondiversifiable risk, the only relevant risk is diversifiable risk.

(True/False)

4.8/5 (31)

The capital asset pricing model (CAPM) links together unsystematic risk and return for all assets.

(True/False)

4.7/5 (29)

An increase in the Treasury Bill rate ________ the required rate of return of a common stock.

(Multiple Choice)

4.9/5 (35)

The standard deviation of a portfolio is a function only of the standard deviations of the individual securities in the portfolio and the proportion of the portfolio invested in those securities.

(True/False)

4.8/5 (34)

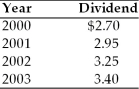

Tangshan Antiques has a beta of 1.40, the annual risk-free rate of interest is currently 10 percent, and the required return on the market portfolio is 16 percent. The firm estimates that its future dividends will continue to increase at an annual compound rate consistent with that experienced over the 2000-2003 period.  (a) Estimate the value of Tangshan Antiques stock.

(b) A lawsuit has been filed against the company by a competitor, and the potential loss has increased risk, which is reflected in the company's beta, increasing it to 1.6. What is the estimated price of the stock following the filing of the lawsuit.

(a) Estimate the value of Tangshan Antiques stock.

(b) A lawsuit has been filed against the company by a competitor, and the potential loss has increased risk, which is reflected in the company's beta, increasing it to 1.6. What is the estimated price of the stock following the filing of the lawsuit.

(Essay)

4.8/5 (28)

Two assets whose returns move in the same direction and have a correlation coefficient of +1 are each very risky assets.

(True/False)

4.9/5 (33)

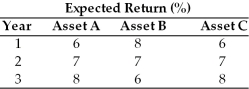

Table 8.1  -The correlation of returns between Asset A and Asset B can be characterized as ________. (See Table 8.1)

-The correlation of returns between Asset A and Asset B can be characterized as ________. (See Table 8.1)

(Multiple Choice)

4.8/5 (35)

Table 8.1

-If you were to create a portfolio designed to reduce risk by investing equal proportions in each of two different assets, which portfolio would you recommend? (See Table 8.1)

(Multiple Choice)

4.8/5 (33)

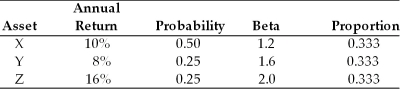

Table 8.2

You are going to invest $20,000 in a portfolio consisting of assets X, Y, and Z, as follows:  -The beta of the portfolio in Table 8.2 indicates this portfolio

-The beta of the portfolio in Table 8.2 indicates this portfolio

(Multiple Choice)

4.9/5 (36)

A portfolio of two negatively correlated assets has less risk than either of the individual assets.

(True/False)

4.9/5 (41)

For the risk-averse manager, the required return decreases for an increase in risk.

(True/False)

4.7/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)