Exam 8: Risk and Return

Exam 1: The Role of Managerial Finance133 Questions

Exam 2: The Financial Market Environment91 Questions

Exam 3: Financial Statements and Ratio Analysis209 Questions

Exam 4: Cash Flow and Financial Planning183 Questions

Exam 5: Time Value of Money173 Questions

Exam 6: Interest Rates and Bond Valuation224 Questions

Exam 7: Stock Valuation188 Questions

Exam 8: Risk and Return190 Questions

Exam 9: The Cost of Capital137 Questions

Exam 10: Capital Budgeting Techniques167 Questions

Exam 11: Capital Budgeting Cash Flows117 Questions

Exam 12: Risk and Refinements in Capital Budgeting106 Questions

Exam 13: Leverage and Capital Structure217 Questions

Exam 14: Payout Policy130 Questions

Exam 15: Working Capital and Current Assets Management340 Questions

Exam 16: Current Liabilities Management171 Questions

Exam 17: Hybrid and Derivative Securities185 Questions

Exam 18: Mergers, Lbos, Divestitures, and Business Failure191 Questions

Exam 19: International Managerial Finance108 Questions

Select questions type

Asset Y has a beta of 1.2. The risk-free rate of return is 6 percent, while the return on the market portfolio of assets is 12 percent. The asset's market risk premium is

(Multiple Choice)

4.8/5  (38)

(38)

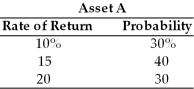

Assuming the following returns and corresponding probabilities for asset A, compute its standard deviation and coefficient of variation.

(Essay)

4.9/5 (28)

Interest rate risk is the chance that the value of an investment will decline because of market factors (such as economic, political, and social events) that are independent of the investment.

(True/False)

4.7/5 (35)

The security market line (SML) reflects the required return in the marketplace for each level of nondiversifiable risk (beta).

(True/False)

4.9/5 (29)

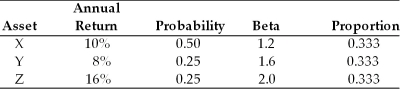

Table 8.2

You are going to invest $20,000 in a portfolio consisting of assets X, Y, and Z, as follows:  -Given the information in Table 8.2, what is the expected annual return of this portfolio?

-Given the information in Table 8.2, what is the expected annual return of this portfolio?

(Multiple Choice)

4.8/5 (51)

Even if assets are not negatively correlated, the lower the positive correlation between them, the lower the resulting risk.

(True/False)

4.8/5 (35)

A common approach of estimating the variability of returns involving forecasting the pessimistic, most likely, and optimistic returns associated with the asset is called

(Multiple Choice)

4.7/5 (39)

The ________ of an event occurring is the percentage chance of a given outcome.

(Multiple Choice)

4.9/5 (41)

Total security risk is the sum of a security's nondiversifiable and diversifiable risk.

(True/False)

4.8/5 (37)

The higher the coefficient of variation, the greater the risk and therefore the higher the expected return.

(True/False)

4.8/5 (38)

The financial manager's goal for the firm is to create a portfolio that maximizes return in order to maximize the value of the firm.

(True/False)

4.8/5 (35)

A portfolio combining two assets whose returns are less than perfectly positive correlated can increase total risk to a level above that of either of the components.

(True/False)

4.8/5 (36)

The required return on an asset is an increasing function of its nondiversifiable risk.

(True/False)

4.9/5 (35)

Assuming a risk-free rate of 8 percent and a market return of 12 percent, would a wise investor acquire a security with a Beta of 1.5 and a rate of return of 14 percent given the facts above?

(Essay)

4.9/5 (32)

What is the expected risk-free rate of return if asset X, with a beta of 1.5, has an expected return of 20 percent, and the expected market return is 15 percent?

(Multiple Choice)

5.0/5 (33)

Systematic risk is that portion of an asset's risk that is attributable to firm-specific, random causes.

(True/False)

4.7/5 (35)

In general, widely accepted expectations of hard times ahead tend to cause investors to become less risk-averse.

(True/False)

4.9/5 (30)

The coefficient of variation is a measure of relative dispersion that is useful in comparing the risks of assets with different expected returns.

(True/False)

4.8/5 (34)

The ________ measures the dispersion around the expected value.

(Multiple Choice)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)