Exam 18: Portfolio Performance Evaluation

Exam 1: Investments: Background and Issues75 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets90 Questions

Exam 4: Mutual Funds and Other Investment Companies85 Questions

Exam 5: Risk and Return: Past and Prologue83 Questions

Exam 6: Efficient Diversification84 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory85 Questions

Exam 8: The Efficient Market Hypothesis86 Questions

Exam 9: Behavioral Finance and Technical Analysis87 Questions

Exam 10: Bond Prices and Yields93 Questions

Exam 11: Managing Bond Portfolios85 Questions

Exam 12: Macroeconomic and Industry Analysis89 Questions

Exam 13: Equity Valuation88 Questions

Exam 14: Financial Statement Analysis84 Questions

Exam 15: Options Markets88 Questions

Exam 16: Option Valuation85 Questions

Exam 17: Futures Markets and Risk Management87 Questions

Exam 18: Portfolio Performance Evaluation87 Questions

Exam 19: Globalization and International Investing70 Questions

Exam 20: Hedge Funds60 Questions

Exam 21: Taxes,inflation,and Investment Strategy73 Questions

Exam 22: Investors and the Investment Process81 Questions

Select questions type

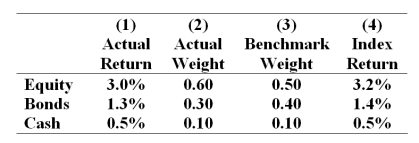

The table presents the actual return of each sector of the manager's portfolio in column (1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral sector allocations in column (3), and the returns of sector indexes in column 4.  -What is the contribution of asset allocation to relative performance?

-What is the contribution of asset allocation to relative performance?

(Multiple Choice)

4.8/5  (42)

(42)

A portfolio generates an annual return of 16%,a beta of 1.2 and a standard deviation of 19%.The market index return is 12% and has a standard deviation of 16%.What is Jensen's alpha of the portfolio if the risk free rate is 6%?

(Multiple Choice)

4.8/5 (46)

A portfolio generates an annual return of 13%,a beta of 0.7 and a standard deviation of 17%.The market index return is 14% and has a standard deviation of 21%.What is the Sharpe measure of the portfolio if the risk free rate is 5%?

(Multiple Choice)

4.8/5 (38)

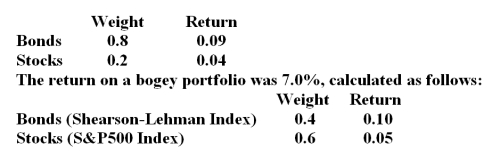

In a particular year, Lost Hope Mutual Fund made the following investments in asset classes:  -The contribution of asset allocation across markets to the total extra return was __________.

-The contribution of asset allocation across markets to the total extra return was __________.

(Multiple Choice)

4.9/5 (42)

What phrase might be used as a substitute for the Treynor-Black model developed in 1973?

(Multiple Choice)

4.9/5 (38)

In creating the T2 measure one mixes P* and T-bills to match the _____ of the market and in creating the M2 measure one mixes P* and T-bills to match the _____ of the market.

(Multiple Choice)

4.7/5 (41)

The table presents the actual return of each sector of the manager's portfolio in column (1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral sector allocations in column (3), and the returns of sector indexes in column 4.

-What was the manager's over or under performance for the month?

(Multiple Choice)

4.8/5 (43)

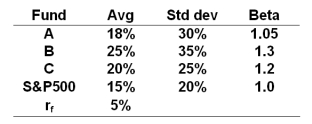

The risk free rate, average returns, standard deviations and betas for three funds and the S&P500 are given below.  -If these portfolios are subcomponents which make up part of a well diversified portfolio then portfolio ______ is preferred.

-If these portfolios are subcomponents which make up part of a well diversified portfolio then portfolio ______ is preferred.

(Multiple Choice)

4.8/5 (41)

The __________ calculates the reward to risk trade-off by dividing the average portfolio excess return by the portfolio beta.

(Multiple Choice)

4.9/5 (41)

The M2 measure of portfolio performance was developed by ______________.

(Multiple Choice)

4.9/5 (42)

In the Treynor-Black model,the weight of each analyzed security in the portfolio should be proportional to its __________.

(Multiple Choice)

4.7/5 (32)

The risk free rate, average returns, standard deviations and betas for three funds and the S&P500 are given below.

-Based on the example used in the book,a perfect market timer would have made _______ of dollars on a $1 investment between 1926 and 2008.

(Multiple Choice)

4.9/5 (37)

The appraisal ratio is equal to the stock's ____ divided by its ______.

(Multiple Choice)

4.9/5 (37)

The risk free rate, average returns, standard deviations and betas for three funds and the S&P500 are given below.

-What is the T2 measure for portfolio A?

(Multiple Choice)

4.8/5 (38)

Which of the following investment strategies would have produced the highest returns in the time period since 1926?

(Multiple Choice)

4.7/5 (40)

In the Treynor-Black model,the contribution of individual security to the active portfolio should be based primarily on the stock's _________.

(Multiple Choice)

4.9/5 (35)

If an investor is a successful market timer,his distribution of monthly portfolio returns will __________.

(Multiple Choice)

4.8/5 (45)

The Treynor-Black model is a model that shows how an investment manager can use security analysis and statistics to construct __________.

(Multiple Choice)

4.9/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)