Exam 18: Portfolio Performance Evaluation

Exam 1: Investments: Background and Issues75 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets90 Questions

Exam 4: Mutual Funds and Other Investment Companies85 Questions

Exam 5: Risk and Return: Past and Prologue83 Questions

Exam 6: Efficient Diversification84 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory85 Questions

Exam 8: The Efficient Market Hypothesis86 Questions

Exam 9: Behavioral Finance and Technical Analysis87 Questions

Exam 10: Bond Prices and Yields93 Questions

Exam 11: Managing Bond Portfolios85 Questions

Exam 12: Macroeconomic and Industry Analysis89 Questions

Exam 13: Equity Valuation88 Questions

Exam 14: Financial Statement Analysis84 Questions

Exam 15: Options Markets88 Questions

Exam 16: Option Valuation85 Questions

Exam 17: Futures Markets and Risk Management87 Questions

Exam 18: Portfolio Performance Evaluation87 Questions

Exam 19: Globalization and International Investing70 Questions

Exam 20: Hedge Funds60 Questions

Exam 21: Taxes,inflation,and Investment Strategy73 Questions

Exam 22: Investors and the Investment Process81 Questions

Select questions type

In performance measurement the bogey portfolio is designed to _________.

(Multiple Choice)

4.8/5  (33)

(33)

The Treynor-Black Model assumes security markets are _________.

(Multiple Choice)

4.9/5 (37)

A mutual fund with a beta of 1.1 has outperformed the S&P500 over the last 20 years.We know that this mutual fund manager _______________________.

(Multiple Choice)

4.9/5 (39)

__________ portfolio manager(s)experience streaks of abnormal returns which are hard to label as lucky outcomes,and ____ anomalies in realized returns have been sufficiently persistent such that portfolio managers could use them to beat a passive strategy over prolonged periods.

(Multiple Choice)

4.8/5 (34)

Consider the theory of active portfolio management.Stocks A and B have the same beta and the same positive alpha.Stock A has higher nonsystematic risk than stock B. You should want __________ in your active portfolio.

(Multiple Choice)

4.8/5 (39)

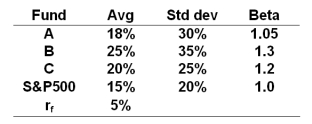

The risk free rate, average returns, standard deviations and betas for three funds and the S&P500 are given below.  -Based on the M2 measure,portfolio C has a superior return of _____ as compared to the S&P500.

-Based on the M2 measure,portfolio C has a superior return of _____ as compared to the S&P500.

(Multiple Choice)

5.0/5 (36)

Active portfolio managers try to construct a risky portfolio with _______.

(Multiple Choice)

4.8/5 (33)

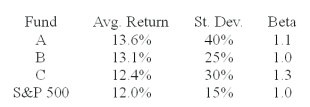

The average returns, standard deviations and betas for three funds are given below along with data for the S&P 500 index. The risk free return during the sample period is 6%.  -You wish to evaluate the three mutual funds using the Treynor measure for performance evaluation.The fund with the highest Treynor measure of performance is __________.

-You wish to evaluate the three mutual funds using the Treynor measure for performance evaluation.The fund with the highest Treynor measure of performance is __________.

(Multiple Choice)

4.8/5 (41)

The critical variable in the determination of the success of the active portfolio is the stock's __________.

(Multiple Choice)

4.9/5 (32)

A portfolio generates an annual return of 16%,a beta of 1.2 and a standard deviation of 19%.The market index return is 12% and has a standard deviation of 16%.What is the Sharpe measure of the portfolio if the risk free rate is 6%?

(Multiple Choice)

4.9/5 (33)

The risk free rate, average returns, standard deviations and betas for three funds and the S&P500 are given below.

-Which one of the following is largely based on forecasts of macroeconomic factors?

(Multiple Choice)

4.7/5 (35)

In the Treynor-Black model,the active portfolio will contain stocks with __________.

(Multiple Choice)

4.9/5 (37)

Assume you purchased a rental property for $100,000 and sold it one year later for $115,000 (there was no mortgage on the property).At the time of the sale,you paid $3,000 in commissions and $1,000 in taxes.If you received $10,000 in rental income (all received at the end of the year),what annual rate of return did you earn?

(Multiple Choice)

4.9/5 (42)

A portfolio generates an annual return of 16%,a beta of 1.2 and a standard deviation of 19%.The market index return is 12% and has a standard deviation of 16%.What is the Treynor measure of the portfolio if the risk free rate is 6%?

(Multiple Choice)

4.9/5 (40)

A managed portfolio has a standard deviation equal to 22% and a beta of 0.9 when the market portfolio's standard deviation is 26%.The adjusted portfolio P* needed to calculate the M2 measure will have ________ invested in the managed portfolio and the rest in T-bills.

(Multiple Choice)

4.8/5 (37)

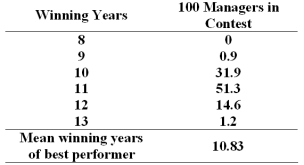

One hundred fund managers enter a contest to see how many times in thirteen years they can earn a higher return than their competitors.The probability distribution of the number of successful years out of thirteen for the best performing money managers is  Out of this sample,chance alone would indicate that there is a ______ probability that someone would beat the market at least 11 times out of 13 years.

Out of this sample,chance alone would indicate that there is a ______ probability that someone would beat the market at least 11 times out of 13 years.

(Multiple Choice)

4.8/5 (38)

Portfolio performance is often decomposed into various subcomponents such as the return due to ___________.

I.broad asset allocation across security classes

II.sector weightings within equity markets

III.security selection with a given sector

The one decision that contributes most to the fund performance is

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)